Payroll tax grouping for related corporations

How related corporations are grouped for payroll tax, including examples.

What are related corporations?

All corporations that meet the definition of ‘related bodies corporate’ in section 50 of the Corporations Act 2001 are grouped for payroll tax.

Corporations are related if they are:

- a holding company and a subsidiary

- subsidiaries of the same holding company.

Any related corporations paying Australian wages are grouped, even if they have an overseas holding company.

Corporations grouped under this provision cannot apply for an exclusion from the group under section 79 of the Payroll Tax Act 2007 (PTA).

Note, trustee or nominee companies cannot be grouped under this provision.

Payroll tax tips for related corporations

- Related corporations must register for payroll tax as a member of a group.

- Grouped employers must nominate a designated group employer (DGE), or if you wish to lodge a joint return, a group single lodger for the group (SLG). Read more on the Grouping page.

- Only a DGE or SLG can claim the threshold entitlement. Read more about how to calculate thresholds on the rates and thresholds page.

How can corporations be grouped?

A corporation will be grouped with another corporation for the purposes of section 70 of the PTA if it:

- controls the composition of the board of directors of that other corporation, or

- can cast, or control the casting of, more than 50% of the votes which can be cast at a general meeting of that other corporation, or

- holds more than 50% of the issued share capital (excluding certain shares with limited rights).

Examples of related corporation grouping

Example 1

Controls the composition of the board of directors of that other corporation

Person A (natural person) holds 100% of issued capital of ABC Investments Pty Ltd (investments vehicle). ABC Investments Pty Ltd owns 40% of the issued capital in XYZ Pty Ltd. Persons B, C and D as trustees of ABC Nominees Trust own 20% of the issued capital of XYZ Pty Ltd. Remaining 40% of the issued capital of XYZ Pty Ltd is held by minority shareholders with less than 5%. The Constitution of XYZ Pty Ltd provides: - Board consists of one director and six independent directors (seven directors in total).

- Issued capital – 1,000,000 ordinary shares.

- Every 10% (100,000 ordinary shares) equity capital in the business can appoint one independent director.

Pursuant to the Constitution of XYZ Pty Ltd, ABC Investments Pty Ltd can appoint four independent directors. This means ABC Investments Pty Ltd can appoint 4 of the 7 directors, which is more than 50% of XYZ Pty Ltd director board based on XYZ Pty Ltd Article of Constitution. Therefore, ABC Investments Pty Ltd controls the composition of the board of XYZ Pty Ltd and as such, XYZ Pty Limited is considered a subsidiary of ABC Investments Pty Ltd. |

Diagram 1: Person A can control another entity with less than 50% ownership by controlling the composition of the board of directors of that other corporation.

Example 2

Can cast, or control the casting of, more than 50% of the votes which can be cast at a general meeting of that other corporation

Dotcom Pty Ltd issued capital includes both voting (Class A) and non-voting shares (Class B). TechHub Pty Ltd owns 51% of Class A shares of Dotcom Pty Ltd. TechHub Pty Ltd can cast more than 50% of the votes in general meetings of Dotcom Pty Ltd pursuant to 51% holding of Class A voting shares. Therefore, the two businesses form a group under related corporations. If TechHub held a mixture of voting shares and non-voting shares of Dotcom, and the number of voting shares held was not more than 50%, they would not be considered related corporations. |

Diagram 2: A corporation can control another entity with less than 50% ownership through casting or controlling the casting of more than 50% of the votes which can be cast at a general meeting of that other corporation.

Example 3

Holds more than 50% of the issued share capital

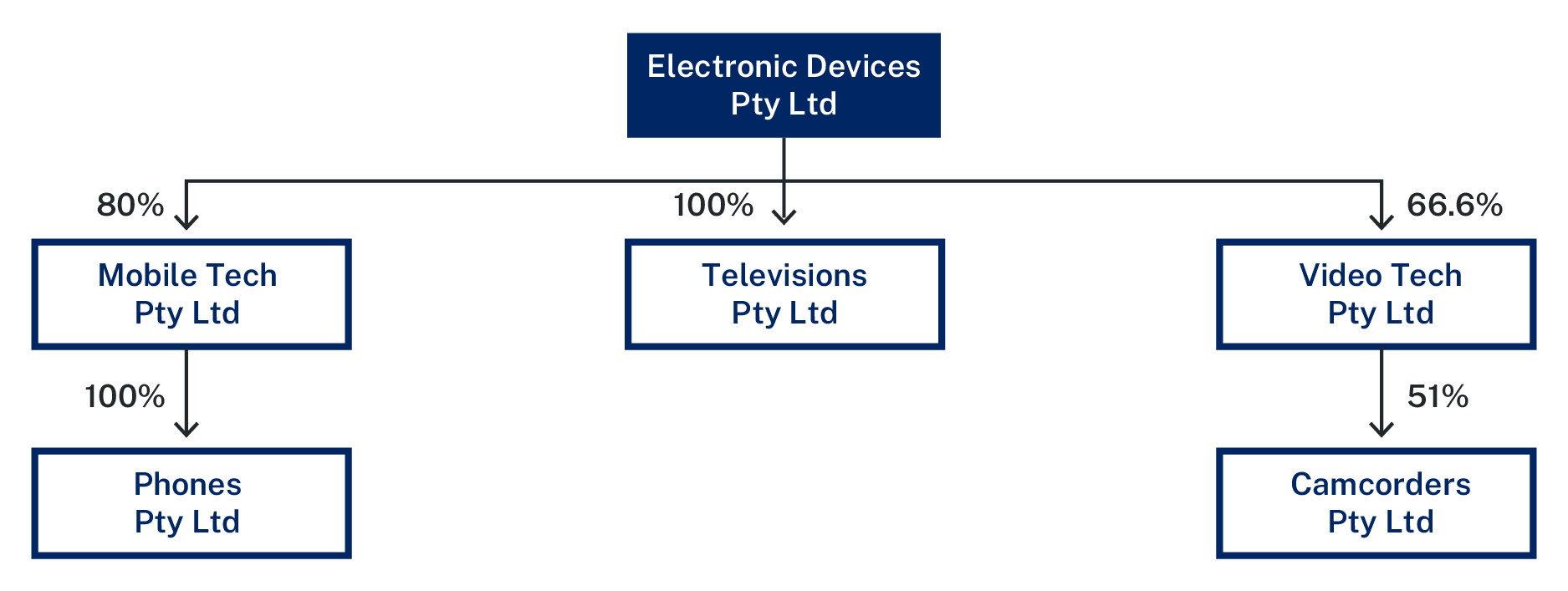

This is a common example of related corporation grouping.

Electronic Devices Pty Ltd owns Mobile Tech Pty Ltd, Video Tech Pty Ltd and Televisions Pty Ltd. Mobile Tech Pty Ltd owns Phones Pty Ltd. Video Tech Pty Ltd owns Camcorders Pty Ltd. Electronic Devices Pty Ltd is the ultimate holding company. All six companies are grouped because Electronic Devices Pty Ltd is the ultimate holding company of all five of the other corporations. |

Diagram 3: A related corporation grouping when a corporation holds more than 50% of the issued share capital.

Example 4

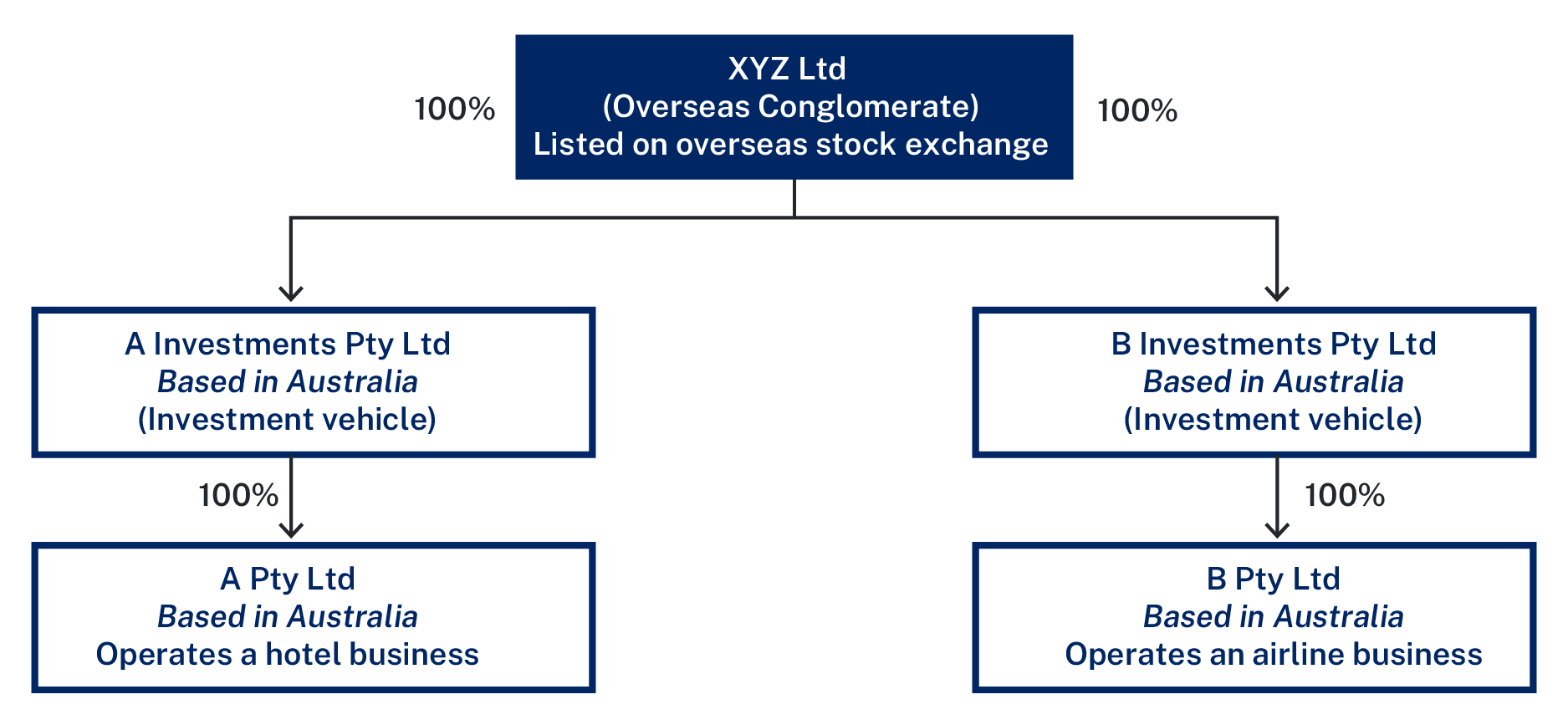

International conglomerates and ultimate holding companies

If all, or majority, shares in a company are held by another company, the second company is considered to be the holding company (HC) of the first mentioned company.

Ultimate parent company (UPC) generally refers to the highest company within the hierarchy of the entire organisation.

Revenue NSW has seen errors being made in relation to identifying the UPC, particularly when UPC is an overseas conglomerate and the entities do not have a direct relationship with that entity.

A Pty Ltd operates a hotel business and is a wholly owned subsidiary of investment vehicle A Investments Pty Ltd. A Investments Pty Ltd is wholly owned by multinational conglomerate XYZ Ltd (listed in an overseas stock exchange). B Pty Ltd operates an airline business and is a wholly owned subsidiary of investment vehicle B Investments Pty Ltd. B Investments Pty Ltd is wholly owned by XYZ limited. A Pty Ltd and B Pty Ltd have a separate management structure. They do not: - have any transactions together

- have any working business relationship together, or

- deal directly with XYZ Ltd.

However, since XYZ Ltd “holds more than 50% of the issued share capital” in both A Investments Pty Ltd and B Investments Pty Ltd, and A Investments Pty Ltd and B Investments Pty Ltd “holds more than 50% of the issued share capital” in A Pty Ltd and B Pty Ltd respectively, all business form a group under related corporation grouping pursuant to Section 70 of the PTA. |

Diagram 4: How an international conglomeration, with corporations based in Australia, can form a related corporation grouping.

Commissioner’s Practice Note

For more examples of payroll tax groupings read Commissioner's practice note 009: Payroll tax grouping.

Contact the payroll tax team

If you have questions about this topic call 1300 139 815 or +61 2 7808 6904 for international callers.

You can also email [email protected]