Gig workers can be considered independent contractors or employees, or sometimes the platform operator is classed as an employment agent. It depends on the business structure and the workers’ employment relationship. Click the arrow to read the new ‘Gig economy businesses’ page.

Payroll tax grouping for illegal phoenix operators

If a business intentionally liquidates to avoid payroll tax, a new business that emerges may be liable for the outstanding payroll tax of the former business. Promoters of illegal phoenix schemes and business directors may be penalised.

The NSW Government amended grouping provisions in the Payroll Tax Act 2007 in September 2023 to reduce lost revenue from illegal phoenix activity. The changes are outlined on this page.

On this page

It is estimated that the costs of illegal phoenix activity to the Australian economy exceed $2.85 billion annually.

Revenue NSW can now recover unpaid payroll tax from NSW employers who have engaged in illegal phoenix activity to avoid state tax responsibilities.

We can now also penalise those who promote illegal phoenix schemes, including directors and intermediaries.

For details on how to identify and report phoenix operators read the illegal phoenix activity page.

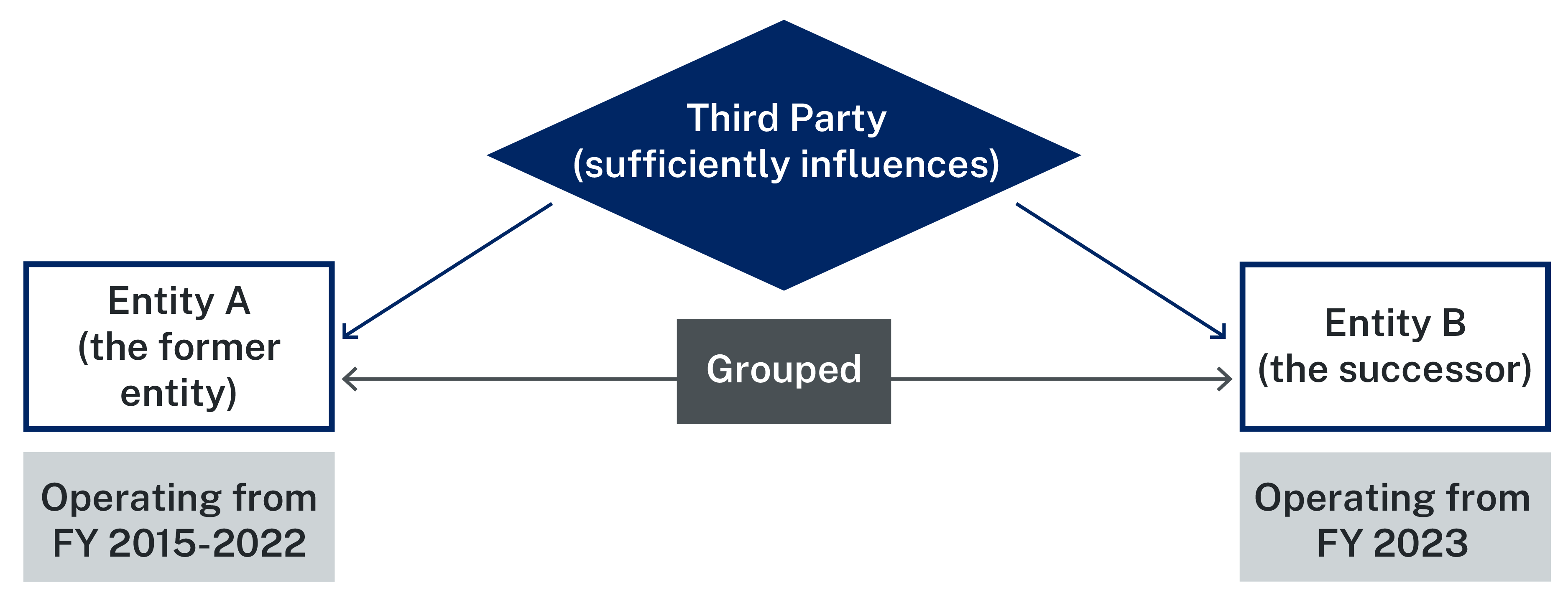

How phoenix operators are grouped

An entity (the successor) and a former entity constitute a group if the successor and the former entity are or were sufficiently influenced by the same third party.

A successor is often referred to as a phoenix operator.

Sufficiently influenced is when a former entity and the successor must act in accordance with the directions, instructions or wishes of a third party.

Sufficiently influenced by a third party may:

be formal or informal

be communicated directly or indirectly through another person, and/or

exist even in the absence of legal control of the former entity or the successor.

Examples of phoenix operator grouping

Former entity directly controlled by the same third party

Entity A was incorporated on 1 July 2015 and incurred a liability of $1 million in payroll tax for the 2017 to 2021 financial years, which they did not pay.

Entity A went into administration in December 2021 and was wound up in June 2022.

Both Entity A and B are fully owned by Mr and Mrs Appleby. As a result, Entity A and B are both sufficiently influenced by the same third party (Mr and Mrs Appleby).

If the Chief Commissioner is satisfied that the influence from the third party was intended to avoid tax or other commercial obligations, Entity A and B are grouped under section 74A of the PTA.

Under section 81 of the PTA, Entity B will be liable for any amount payable by Entity A, including the debts payable before 1 July 2022.

Therefore, Entity B will be liable for the $1 million of outstanding payroll tax payable by Entity A for the 2017 to 2022 financial years.

Former entity indirectly controlled by the same third party

Biscuit Pty Ltd conducts a labour-hire business.

Peter has a controlling interest in Biscuit Pty Ltd as the sole director and sole shareholder. As Peter has a majority voting interest in the company, it is considered that Biscuit Pty Ltd is sufficiently influenced by Peter.

On June 2021 Biscuit Pty Ltd went into administration with $2 million in payroll tax outstanding.

“Banana Pty Ltd as trustee for (ATF) Cake Trust” was formed in December 2021. All assets of Biscuit Pty Ltd were transferred to “Banana Pty Ltd ATF Cake Trust” with the intention to carry on the same labour hire business conducted by Biscuit Pty Ltd.

Peter has a controlling interest in Banana Pty Ltd as the sole shareholder and the director.

Peter’s daughter, Daniella, is the sole beneficiary of Cake Trust.

While Peter does not have direct controlling interest in Cake Trust, he has sufficient influence over the entity because:

he is the controlling person behind the trustee company of Cake Trust, and

the trust deed of Cake Trust confirms the trustee has absolute discretion over the trust business.

As a result, Biscuit Pty Ltd and Cake Trust are sufficiently influenced by Peter.

Biscuit Pty Ltd and Cake Trust are grouped under section 74A of the PTA as the Chief Commissioner is satisfied that the influence of Peter was intended to avoid tax or other commercial obligations.

Under section 81 of the PTA “Banana Pty Ltd ATF Cake Trust” will be liable for any amount payable by Biscuit Pty Ltd, even the debts payable before December 2021.

Therefore, “Banana Pty Ltd ATF Cake Trust” will be liable for the $2 million of outstanding payroll tax that was payable by Biscuit Pty Ltd.

This means that promoter penalties may be imposed along with a section 74A grouping under section 106F(3A) of the TAA.

A person or corporation will be considered a promoter of a tax avoidance scheme under section 106N of the TAA if they are seen to advertise the scheme, encourage its growth or interest in it.

A person or corporation is not considered a promoter of a tax avoidance scheme if they only provide advice or distribute details about the scheme that has been prepared by someone else.

The Chief Commissioner may apply to the Supreme Court of NSW to make an order requesting a person or corporation who breaches section 106N of the TAA pay a penalty that does not exceed:

Penalties maybe imposed under section 58A of the TAA if the director is deliberately seen to evade or attempt to evade paying tax.

The maximum penalty that can be applied in this instance is:

500 penalty units

2 years imprisonment, or

both above.

Penalties may not be imposed if the director can prove:

that they have taken reasonable care to comply, or

the circumstances involved are beyond their control.

Exclusion from a payroll tax grouping

The Chief Commissioner will not group the entity and a former entity where the influence of the third party was not intended to avoid tax or other commercial obligations.

Section 74A of the PTA is not intended to group businesses because of legitimate business failures or restructures.

Please note, an entity that is grouped under section 74A of the PTA cannot apply for an exclusion under section 79 of the PTA.