Gig workers can be considered independent contractors or employees, or sometimes the platform operator is classed as an employment agent. It depends on the business structure and the workers’ employment relationship. Click the arrow to read the new ‘Gig economy businesses’ page.

Businesses can be grouped for payroll tax in different ways. Grouping affects how businesses can claim the payroll tax threshold.

New payroll tax grouping for illegal phoenix operators

The NSW Government amended grouping provisions in the Payroll Tax Act 2007 in September 2023 to reduce lost revenue from illegal phoenix activity. For more details and examples read payroll tax grouping for illegal phoenix operators.

On this page

For payroll tax purposes, businesses can be grouped with other businesses if there is a link between the businesses.

Grouping can occur regardless of where a business operates.

Grouping has important implications for calculating threshold entitlements because where a group exists:

the gross wages of all group members must be added together and a single threshold deduction applies to the group.

the threshold entitlement is based on the proportion of NSW wages against total Australian wages.

every member of the group is liable for any unpaid payroll tax of any other group members.

Where a business is a member of more than one group, all businesses in each group are subsumed into a single payroll tax group.

If a person or set of persons together have a controlling interest in two or more businesses, those businesses are grouped for payroll tax purposes. A ‘person’ includes a natural person, set of persons, trustee or corporation.

There are different definitions of ‘controlling interest’ depending on the business type:

Sole owner: a person who is the sole business owner (whether or not as a trustee) has a controlling interest in that business.

Joint owners: a set of persons together (including as trustees) who are the sole business owners have a controlling interest in that business.

Company: a controlling interest is held by any person who is, or set of persons who together are, entitled to exercise more than 50 per cent of the voting power at director meetings; or any person who has, or set of persons who together have, more than 50 per cent of the voting rights attached to voting shares that the company has issued.

Body corporate or unincorporated: a controlling interest is held by any person who, or set of persons who together, controls more than 50 per cent of the board of management.

Partnership: a controlling interest is held by any person who owns, or set of persons who together own, more than 50 per cent of the partnership capital or are entitled to more than 50 per cent of the partnership profits.

Trust: a controlling interest is held by any person who is a beneficiary and is entitled to more than 50 per cent of the value of the interests in the trust that carries on the business. Note: if the trust is a discretionary trust then every beneficiary is deemed to have a controlling interest in the trust.

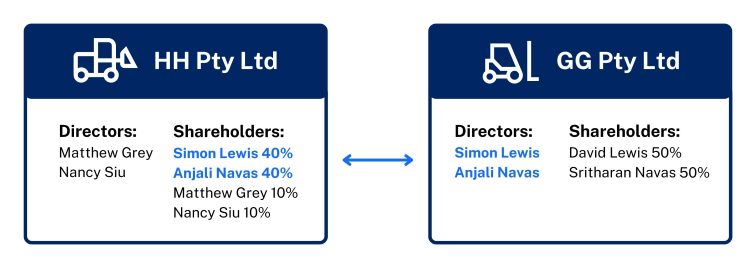

Example

Simon holds 40% of the shares in HH Pty Ltd and is one of two directors of GG Pty Ltd. Anjali holds 40% of the shares in HH Pty Ltd and is the other director of GG Pty Ltd. Together as a set of persons Simon and Anjali have a controlling interest in both HH Pty Ltd (controlling 80% of the voting power attached to the share capital) and GG Pty Ltd (controlling 100% of the voting power at directors’ meetings). The businesses are grouped for payroll tax purposes.

Example

Maria and Frank Grasso are the shareholders of ACE Pty Ltd. They are also both beneficiaries of the Grasso Family Trust (along with their two children). Frank and Maria together as a set of persons have a controlling interest in both the trust and ACE Pty Ltd. The two businesses form a group for payroll tax purposes.

NB: the carrying on of a trust is deemed to be a ‘business’ under the Payroll Tax Act 2007 and as the Grasso Family Trust is a discretionary trust then all beneficiaries are deemed to have a controlling interest in the business of the trust.

A larger group can be formed out of multiple smaller groups when a business is a member of two or more groups at the same time, or the members of a group share a controlling interest in another business.

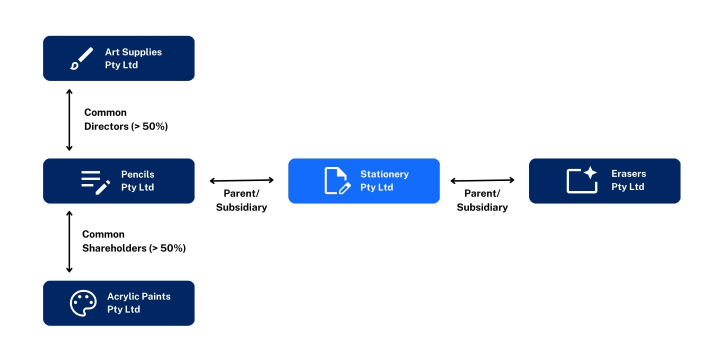

Example: Subsuming through common group members

Stationery Pty Ltd is the holding company of Pencils Pty Ltd (Group 1).

Stationery Pty Ltd is also the holding company of Erasers Pty Ltd (Group 2)

The directors of Art Supplies Pty Ltd are also the directors of Pencils Pty Ltd (Group 3).

The shareholders of Acrylic Paints Pty Ltd are also the shareholders of Pencils Pty Ltd (Group 4)

Stationery Pty Ltd is common to Groups 1 and 2; as such a payroll tax group is formed by Stationery Pty Ltd, Pencils Pty Ltd and Erasers Pty Ltd.

Pencils Pty Ltd is common to Groups 3 and 4; as such a payroll tax group is formed by Art Supplies Pty Ltd, Acrylic Paints Pty Ltd and Pencils Pty Ltd.

Pencils Pty Ltd is common to BOTH groups. Subsuming applies and so a group consisting of all 5 businesses is formed i.e. Stationery, Pencils, Erasers, Art Supplies and Acrylic Paints.

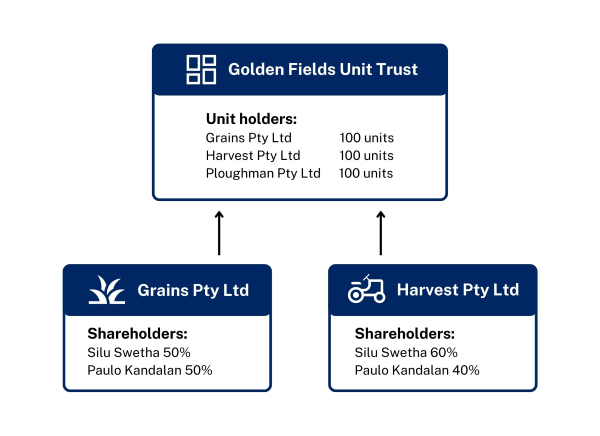

Example: Subsuming through combined interest

Grains Pty Ltd and Harvest Pty Ltd have common shareholders and so are grouped for payroll tax purposes. Each business also holds one-third of the units in the Golden Fields Unit Trust. As Grains Pty Ltd and Harvest Pty Ltd are grouped their interest in the trust is combined (together holding two-thirds of units in the trust) and subsuming means all 3 businesses form a single group for payroll tax purposes (Grains Pty Ltd, Harvest Pty Ltd and the Golden Fields Unit Trust).

Read the case studies page for more grouping examples.

If an entity has a direct, indirect or aggregate interest of more than 50 per cent in any corporation, that corporation is grouped with that entity.

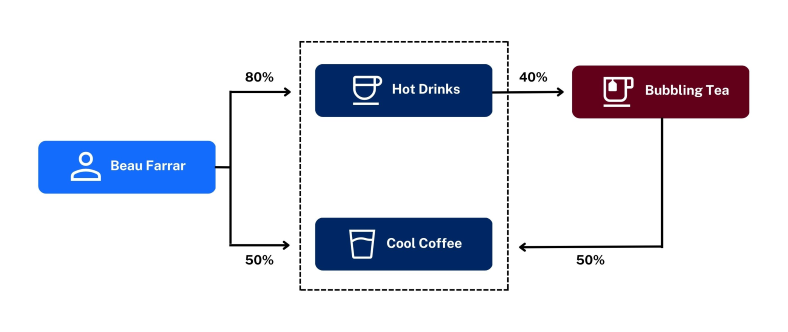

Example

Beau Farrar has a direct interest of 80 per cent in Hot Drinks, and 50 per cent in Cool Coffee. Hot Drinks owns 40 per cent of Bubbling Tea, and Bubbling Tea owns 50 per cent of Cool Coffee. Beau has an indirect interest in Cool Coffee of 16 per cent. This is calculated by multiplying:

Beau’s ownership of Hot Drinks (80 per cent)

Hot Drinks’ ownership of Bubbling Tea (40 per cent)

Bubbling Tea’s ownership of Cool Coffee (50 per cent)

80 per cent × 40 per cent × 50 per cent = 16 per cent

By adding Beau’s direct and indirect ownership in Cool Coffee, Beau has an aggregate interest in Cool Coffee of 66 per cent (50 per cent direct and 16 per cent indirect).

Hot Drinks and Cool Coffee are grouped because Beau has an interest of greater than 50 per cent in both businesses.

Bubbling Tea is not part of the group as the level of Beau’s interest is not more than 50 per cent (80 per cent × 40 per cent = 32 per cent).

Businesses are grouped if one or more employees of a business:

performs duties in connection with another business carried on by the employer and another person (including joint ventures), or

is employed solely or mainly to perform duties in connection with one or more businesses carried on by another person, or

performs duties in fulfillment of an employer’s obligation to provide services to another person under an arrangement or agreement between them.

An employee performs duties for another business if a person in that business can direct or control the manner in which the work is performed by the other person.

Consequently, businesses are not grouped if the employee undertaking work for or in connection with another business is not performing duties.

Example

Green Thumb Pty Ltd is a manufacturer of gardening and greenlife products. Big Box Pty Ltd was set up to provide warehouse and logistic services for Green Thumb Pty Ltd. In providing those services, employees of Big Box are under the direction of, and must adhere to, instructions from Green Thumb Pty Ltd management and staff. The two businesses form a group for payroll tax purposes.

An entity (the successor) and a former entity constitute a group if the successor and the former entity are or were sufficiently influenced by the same third party.

A successor is often referred to as a phoenix operator.

Only one member of a payroll tax group can claim the threshold. The threshold can be claimed either as the designated group employer or the single lodger.

In a designated group employer (DGE) group, one member of the group becomes the DGE and that member must pay wages on its own that exceed the threshold amount. The other group members become non-threshold claimers (NTC).

The DGE is the only member which can claim the threshold. The NTC members of the group pay the flat rate of payroll tax on their wages.