If you have been impacted by a natural disaster and require assistance with your fines or fees, call us on 1300 138 118 to discuss your options. Some online services will be unavailable on Sunday.

A new rebate has been made available from 4 September 2024. The rebate is available for medical centres who bulk bill a majority of their GP services. Click the arrow to find out more including detailed eligibility criteria.

Section 10AA of the Land Tax Management Act 1956 (LTMA) exempts land that is used for the dominant purpose of primary production. If primary production land (PPL) is not rural land, its use must also satisfy additional tests which determine whether the primary production undertaking has a significant and substantial commercial purpose or character and is carried out for the purpose of profit on a continuous or repetitive basis (together referred to as the “commercial tests”).

Meaning of “land used for primary production”

“Land used for primary production” means land whose dominant use is:

cultivation, for the purpose of selling the produce of the cultivation, or

the maintenance of animals (including birds), whether wild or domesticated, for the purpose of selling them or their natural increase or bodily produce, or

commercial fishing (including preparation for that fishing and the storage or preparation of fish or fishing gear) or the commercial farming of fish, molluscs, crustaceans or other aquatic animals, or

the keeping of bees, for the purpose of selling their honey, or

a commercial plant nursery, but not a nursery at which the principal cultivation is the maintenance of plants pending their sale to the general public, or

the propagation for sale of mushrooms, orchids or flowers.

The reference to “land” in section 10AA is a reference to a parcel of land which has been separately valued and recorded in the Register of Land Values kept by the Valuer General under s.14CC of the Valuation of Land Act 1916.

In the case of land that is not “rural land”, the primary production conducted on the land must have a significant and substantial commercial purpose or character, and must be engaged in for the purpose of profit on a continuous or repetitive basis, whether or not a profit is actually made (the commercial tests).

Lodgement of returns

If a person (including a corporation or trustee of a trust) acquires a parcel of land, that person is required to lodge a land tax return with the Chief Commission by a date specified in a notice published in the Government Gazette prior to the commencement of the next tax year. If the new owner considers the land qualifies for the exemption for primary production, the owner must include in the return an application for the exemption, including supporting information. A person who owns exempt land whose primary production use of the land ends or is reduced to the extent that it ceases to satisfy the “dominant use” test (see paragraphs 15-20) or the “commercial” tests (see paragraphs 49-64) , or whose land is rezoned (see paragraphs 65-67), must lodge a variation return with the Chief Commissioner.

Failure to lodge a return when required may be a tax default, and may result in multiple prior year assessments being issued by the Chief Commissioner, including assessment of penalty tax and interest.

Purpose of Ruling

The purpose of this ruling is to explain the Chief Commissioner’s interpretation of the exemption provisions in s.10AA applying to land used for primary production.

Ruling

Classification of land as “rural land”

An owner of “rural land” must demonstrate that the dominant use of the land is one of the types of primary production specified in s.10AA(3), or a combination of those primary production uses. The commercial tests specified in s.10AA(2) do not apply to “rural land”.

Land is “rural land” if it is zoned “rural”, “rural-residential”, “non-urban” or “large lot residential” under a planning instrument. If land is not zoned under a planning instrument, it may be regarded as “rural land” if the Chief Commissioner is satisfied the land is rural land.

A parcel of land that has a non-rural zoning applying to any part of the land is not “rural land”[1]. The entire parcel of land must have only rural zonings to be treated as rural land.

The zoning of a parcel of land may be found in a “planning instrument” as defined in section 3 of the LTMA. A planning instrument may be a state, regional or local environmental plan, (including a former planning instrument in force prior to 25 March 1988).

Land that is not rural land but which may be used for primary production under existing use rights is not “rural land” for the purposes of the PPL exemption.

Land with the following land use zones under a Local Environmental Plan made under the Standard Instrument (Local Environmental Plans) Order 2006 is “rural land”:

RU1 Primary Production;

RU2 Rural Landscape;

RU3 Forestry;

RU4 Primary Production Small Lots;

RU5 Village;

RU6 Transition.

The land use zone R5 (“Large Lot Residential”) is also treated as “rural land” for the purposes of the PPL exemption. Land in any other “Residential Zone”, or any other zone type specified in an environmental planning instrument is not “rural land” for the purposes of the PPL exemption.

A parcel of land that is not “rural land” must satisfy the additional commercial tests specified in s.10AA(2). The commercial tests require that the primary production use (or uses):

has a significant and substantial commercial purpose or character; and

is engaged in for the purpose of profit on a continuous or repetitive basis, whether or not a profit is actually made.

Determining the “dominant use” of land

The activity of primary production must be the dominant use of a parcel of land to qualify for the PPL exemption. If primary production is conducted on several parcels, the use of each parcel must be separately determined, and only those parcels that satisfy the test are entitled to exemption.

The decision as to whether primary production is the dominant use of a parcel requires consideration of the nature and intensity of the competing uses, the physical areas over which they are conducted, the time and labour spent in conducting the different uses, the money spent or assets deployed in each use and the value derived or to be derived from each use[2]. It is a question of fact and degree, viewing all of the relevant facts as a whole[3], to arrive at a decision an objective observer would reach from viewing the land as a whole[4].

The task of determining the dominant use requires a comparison of the uses of land for the primary production activities or purposes listed in paragraphs (a) to (f) of s.10AA(3) with uses of the land for all other activities or purpose that are not primary production uses. A relevant “use” of land is a use that requires something to be done with the land, whether by using it physically or refraining from using it so as to obtain an actual and present advantage”, such as

leaving land in fallow as part of a crop rotation, or

removing stock during a drought to prevent damage to the land or avoid stock losses.

Non-primary production “uses” of land have included:

use of a house as a residence by a tenant under a lease[5];

providing short term visitors with a farm experience associated with overnight accommodation;

using virgin land surrounding a hospital as a buffer to provide fresh air and peace and quiet for patients[6];

commercial development of land including preliminary earthworks[7];

surveying and carrying out tests in connection with an existing or proposed development[8].

An intended or planned future use of land is not a use for the purposes of determining the dominant use; eg merely owning land with the intention of future development (“land banking”), or classifying land as “trading stock” and taking advantage of income tax benefits[9].

The key facts and circumstances that are taken into account in determining whether primary production is the dominant use include[10]:

the area of land over which each use extends;

the scale and intensity of the primary production activities compared to the potential scale intensity of that use or carrying capacity of the land;

the relative economic and financial significance of competing uses, including the amount of capital expenditure, current expenditure, revenue and profit attributed to each use;

the scale, extent and intensity of non-primary production uses;

the length of time that each use has been conducted on the land; and

time and labour and resources spent in using the land for each purpose.

Partial PPL exemptions are not available

A partial PPL exemption cannot be applied to a part of a parcel of land which is used for primary production (see paragraph 3 regarding the definition of a “parcel”). The whole parcel is either exempt or not exempt depending on whether or not primary production is the dominant use[11].

Multiple types of primary production uses of a single parcel of land

There may be multiple types of primary production uses occurring on a parcel of land, by the same user or by different users. If the various primary production uses seen as a whole are the main or chief use of the land, outweighing the non-primary production uses, including non-use, the dominant use of the land is for primary production[12].

Non-use may dominate primary production use

If primary production is the only activity conducted on a parcel of land, but part of the land is unused, the primary production activity must be sufficiently substantial or intensive to prevail over the proposition that the land is predominantly unused[13]. If not sufficiently substantial or intensive, the land may be regarded as mainly unused, looking at the land and its use as a whole. The most important factors include:

the proportion of the land which is both usable and used for primary production, compared to the proportion that is not used for any purpose[14];

the time period during which the land is used; ;the periods of 6 months before and after the taxing date are most significant, but a longer time period may be relevant[15];

mere intention to use the land for primary production is not sufficient, but may be relevant[16]. For example, preparation of the land may have commenced, but implementation of that use may be in the early stages of implementation, such as being cleared and fenced in preparation for primary production use.

Capital intensive uses

Where land is used for primary production and is also used for other activities, the comparative level of capital investment, as well as the actual and expected level of income will largely determine whether the land is exempt. If the non-primary production uses require a higher level of capital investment and generate a higher level of income than the primary production uses, it is unlikely that the land will qualify for exemption. This will be particularly important where primary production land is also used for a purpose that requires a significantly higher capital investment, such as wind farming or mining operations.

The area of land committed to each use may be decisive if the amount of capital investment and revenue generated does not clearly suggest which is the dominant use. For example, providing a “farm experience” and/or short term accommodation to farm visitors as a means of supplementing primary production income would not be regarded as the dominant use of the land unless such use involved both substantial capital investment and profitability compared to the primary production use.

Preparatory work as a “use”

Preparation of land for a particular purpose is capable of constituting a use of the land for that purpose. For example, costs associated with construction work and land improvements in preparation for the subdivision and sale of residential lots or completed dwellings may constitute a use for residential development[17].

In the case of primary production activities, land may be classified as land used for primary production if significant preparatory work necessary to commence actual primary production has been undertaken but actual production has not commenced by the taxing date e.g. erecting fencing, weed control, clearing native vegetation, planting and tending of fruit or nut trees, or trees intended to produce timber may constitute primary production use of land even though primary products may not be produced or sold during the relevant tax year. In the case primary production such as fruit, nuts or timber, the products may not be sold for several years[18].

Secondary processing of primary production

Land that is used for processing of primary products, or distribution and sale of the product of primary production does not qualify for the PPL .For example, land used for the dominant purpose of slaughtering animals and/or processing and distributing primary products, such as animal carcasses, will not qualify for exemption, even if the animals were maintained prior to slaughter on other land which was entitled to the exemption[19].

Where secondary processing of primary production occurs on the same land as the primary production activity, e.g. slaughtering of animals on the same land on which the animals are maintained, the primary production use must dominate the secondary processing use for the PPL exemption to apply (see relevant factors in paragraphs 15-20 above).

Time of use

The use of each parcel of land is determined as at the taxing date, but uses of land for a reasonable period before and after the taxing date are relevant in determining the dominant use on the taxing date. The uses of the land during the 6 months immediately before and after the taxing date are generally most relevant[20]. However, longer periods may be relevant in some circumstances; e.g. see paragraphs 32-34.

Intention to use land for primary production

An intention to use land for primary production is not sufficient to qualify for the PPL exemption[21]. However, such an intention may be relevant in some cases if there are activities conducted on the land which result in future sales of produce. For example, in the case of fruit trees, planting and tending of the trees with the intention of producing fruit for sale may qualify as primary production use even if the production and sale of the fruit does not occur until the trees reach maturity several years after planting.

Temporary cessation of primary production

Land may temporarily cease to be used for primary production, for example due to drought, allowing the land to lie fallow or changing the method of production, including changing to organic farming methods. Where primary production use of land temporarily ceases, in a physical sense, for a period of time that includes the taxing date, the facts and circumstances before and after the taxing date, and especially during the 6 months before and after the taxing date are relevant to determining whether the land qualifies for the PPL exemption[22].

If there is a change in the method of primary production, the exemption may continue to apply even though no primary products may be produced for sale for a period of time while the changeover occurs[23]. The period during which the exemption continues will depend on the circumstances but may include a change from conventional farming to organic farming, requiring removal of stock or cessation of cultivation for an extended period to satisfy certification requirements.

The landowner must demonstrate that the primary production activity had previously been the dominant use of the land, and that the hiatus period during which there was no primary production was temporary or a typical part of the cycle of primary production, such that primary production remains the “purpose” attributable to, or the reason for occurrence of the hiatus period. Examples include a drought, biosecurity measures for the treatment of diseases, allowing the land to lie fallow, converting to organic farming methods which may result in the land being unproductive for a period of time, or during a transition from one form of primary production to another.

Primary production use by a person other than the owner

Land may qualify for the PPL exemption if the owner permits another person to conduct primary production activities under a lease or licence, including agistment agreements. It is the use of land and not the identity of the user which is significant[24]. ;However, occasional or intermittent primary production use of land under an agistment agreement may not qualify for exemption if the primary production use of the land is so small that the land is regarded as unused (see paragraph 23 above).

Multiple primary production activities

In relation to the dominant use test (s.10AA(3)), if a parcel of land is used for more than one form of primary production, the dominant use test is satisfied if, having regard to all of the primary production uses, the “dominant use” of the land is primary production. It is not necessary for one of the uses specified in s.10AA(3) to be the dominant use of the land[25].

Types of Primary Production

(a) Cultivation of land [s.10AA(3)(a)]

Cultivation of land for the purpose of selling the produce is not limited to annual crops, or crops with periodic production. The land may in the relevant sense be cultivated either by breaking it up, such as ploughing, or by activities that may not be associated with the breaking up of the soil. “Cultivation” occurs in respect of a particular tax year when the land is tended, or subject to a programme of tending, including improving the water supply, if the tending is conducted in accordance with the practices of husbandry applicable to the particular crop[26].

In the case of land used for timber production, “cultivation” may occur if work is carried out for the protection and improvement of the growing timber, including maintenance of firebreaks, removal of undergrowth or thinning of the trees to allow healthier growth of the remaining timber.

Hydroponic methods of crop production may also qualify as “cultivation” where the tending of the relevant crop is conducted in accordance with the usual husbandry practices applicable to the production of crops by such means.

(b) Maintenance of animals for the purpose of sale [s.10AA(3)(b)]

Maintenance of animals comprises keeping and maintaining animals, whether wild or domesticated, and including birds. The maintenance of animals must[27] occur on the land for which the PPL exemption is sought. The animals must be maintained for the purpose of selling them or their natural increase or bodily produce[28]. It does not matter whether the purpose is to sell live animals or animal products after slaughter and secondary preparation or processing, but the dominant use of the land must be for maintaining the live animals to qualify for the PPL exemption.[29].

The maintenance of the animals requires that the animals are owned or controlled (including leased) by the primary producer. A licence to take wild animals which are not owned by the licensee is not sufficient to satisfy the requirement that the wild animals are “maintained” on the land[30].

Land used for a stud business, including a horse or cattle stud, is eligible for the PPL exemption if the stud animals are maintained for the dominant purpose of selling the animals or their bodily produce, including their offspring or semen[31].

However, the exemption does not apply if the dominant use of the land is the maintenance of horses:

for horse-racing purposes; or

for recreational riding and/or riding sports, including polo; or

for a riding school.

(c) Commercial fishing [s.10AA(3)(c)]

The PPL exemption may apply to land if the dominant use of the land is commercial fishing or commercial farming of fish. For the purposes of the exemption, “fish” includes marine, estuarine or freshwater fish, oysters, molluscs, crustaceans or other aquatic animals. “Fishing” includes the catching of bait fish. Activities conducted on the land may include preparation or storage of nets, boats or other fishing equipment, preparation of bait, or preparation of the fish that have been caught (including the use of drying racks).

In the case of commercial fishing and commercial farming of fish, the dominant use of the land must be for a commercial business. A person who uses land in connection with a commercial enterprise would therefore be expected to hold a commercial licence, permit or other authority appropriate to the enterprise under the Fisheries Management Act 1994.

(d) Beekeeping [s.10AA(3)(d)]

Land used for primary production includes land used to keep bees for the purpose of selling their honey. ;Factors that are relevant in determining whether a beekeeping use of land satisfies the dominant purpose test include[32]:

the number of hives kept;

the length of time before and after the taxing date during which bees are continuously maintained on the land;

the area containing buildings and equipment used in the course of maintaining the bees or producing and selling honey;

the area containing flora and watering points from which foraging bees collect nectar and water so that the bees in the hives can make honey;

the availability of suitable flora on adjacent land from which foraging bees may collect nectar and water; and

whether unused land surrounding the hives provides a buffer between the hives and adjacent land, such as where adjacent land contains residences or businesses.

(e) Commercial plant nurseries [s.10AA(3)(e)]

Under s.10AA(3)(e) of the LTMA land may be eligible for the PPL exemption if it is used for a commercial plant nursery, which is a place, operated on a commercial basis, where plants or trees are propagated. If plants which are sold by the nursery are primarily propagated elsewhere, the land will not qualify for the exemption[33].

The propagation of plants primarily for use by the propagator, or to be hired, displayed or distributed other than by way of sale is not “primary production” for the purposes of the PPL exemption[34].

(f) Propagation of mushrooms, orchids and flowers [s.10AA(3)(f)]

Under 10AA(3)(f) of the LTMA land may be eligible for the PPL exemption if it is used for the propagation of mushrooms, orchids or flowers. This requires the growing of mushrooms, orchids or flowers via propagation methods such as spores, seeds or cuttings. They may be grown in the soil or in pots, but must be produced for the dominant purpose of selling the produce. The PPL exemption will not apply if the product of the propagation is consumed or displayed by the producer rather than being sold.

Commercial purposes and profits tests – s.10AA(2)

If land is used for primary production but is not “rural land” as defined in s.10AA(4), the use of the land must meet the tests set out in s.10AA(2), which are:

the primary production use must have a significant and substantial commercial purpose or character (s.10AA(2)(a)); and

the primary production use must be engaged in for the purpose of profit on a continuous or repetitive basis, whether or not a profit is actually made (s.10AA(2)(b)).

A parcel of land which satisfies the “dominant use” tests in s.10AA(3) is exempt if the owner can demonstrate on the balance of probability that the PPL use on the taxing date satisfies the “commercial purpose or character” and “profits” tests in s 10AA(2), either on its own or viewed together with other land if the relevant parcel and that other land is used together[35]. The tests in s 10AA(2) are considered solely by reference to the actual use of the land on the taxing date of the land tax years in question[36]. However, the facts and circumstances relating to that use applying for a reasonable period before and after the taxing date, especially for the 6 months before and after the taxing date, are relevant[37].

If there are multiple primary production users of land for which the PPL exemption is sought, the “commercial purpose or character” and “profits” tests are assessed as a whole, taking into account the primary production activities of each of the users. If any of those users conduct their primary production business on the land together with other land (see paragraph 56), the “commercial purpose or character” and “profits” tests are applied to that user’s primary production business as a whole[38].

(a) Significant and substantial commercial purpose or character – s.10AA(2)(a)

The “significant and substantial commercial purpose or character” test requires that use of the lands to have had a relatively high degree of importance. A business that is carried on in a small way or as a sideline does not satisfy the test. The enterprise must be conducted on a commercial basis with appropriate attention to the orthodoxies of income, expenditure and an intention to be profitable, while recognising the elements of unpredictability of any business operation, especially primary production[39]. An enterprise must have either a significant and substantial purpose (ie subjective intention), or a significant and substantial character ( viewed objectively). It may have both, but either a significant purpose or a significant and substantial character is sufficient.

Relevant factors in determining whether both the “purpose” and “character” tests are satisfied include[40]:

the physical size and scale of the primary production activity;

the repetition and regularity of that activity;

the actual primary production from the land compared to the expected production if fully utilised for that purpose;

the intensity of the primary production activities;

the history and future prospects in relation to income, costs and profit;

the characteristics of similar primary production enterprises;

the expected commercial viability of the business in the foreseeable future, including the potential to generate a reasonable profit, having regard to the level of investment in the business.

The “significant and substantial commercial purpose or character” tests may be satisfied by either:

the use of land on which primary production is conducted, or

the use of that land in conjunction with other lands on which a primary production business is conducted, if the land and “other” land is “used together”[41] (see paragraph 56).

The connections that are relevant in assessing whether multiple parcels of land are “used together” in a primary production business include[42]:

whether there is movement of animals, equipment, materials or primary production between the parcels of land and the reasons for such movements;

whether work relating to the enterprise is performed on or in relation to each parcel by the same person(s);

whether common accounting records, tax records, and bank accounts are kept or used;

whether the use of the multiple parcels benefits the enterprise by providing alternative sources of income or cash flow, or by permitting rotation of crops or animals;

whether different physical or climatic conditions applying to the parcels mitigates environmental risks to income or production, including risk of floods or drought;

whether the connections benefit the primary production enterprise.

(b) The purpose of profit test – s.10AA(2)(b)

Section 10AA(2)(b) requires that the use of the land for primary production must be engaged in for the purpose of profit on a continuous or repetitive basis, whether or not a profit is actually made (“purpose of profit test”). “Profit” is not defined in the LTMA, and should be given its ordinary meaning having regard to accounting principles[43].

The profit result in periods preceding the relevant taxing date and the expected profit result in subsequent years are taken into account in determining the primary producer’s intention. Prospective profit forecasts are considered, especially if the primary production use does not generate a profit in the tax years for which the PPL exemption is claimed.

The fact that land could be used more profitably, whether by the owner, the primary production enterprise or by someone else is not relevant[44].

If other land is used together in a primary production business[45] with the land for which exemption is sought, the “purpose of profit” test is applied to the entirety of primary production activities by the entity (or entities) conducting a business on the land. The test is not limited to the activities conducted on the land for which the PPL exemption is sought.

The absence of actual profit by a primary production business does not exclude eligibility for the PPL exemption if there is a genuine intention to achieve a profit, but a continuous pattern of a lack of profit may lead to a conclusion that the primary production use of the land was not engaged in for the purpose of profit[46].

(c) Measures of profit – ss.10AA(2)(a) and (b)[47]

Measures of profit that are commonly used by businesses are relevant to both the “significant and substantial purpose” and “intention to profit” tests. Non-cash costs incurred, such as depreciation are taken into account. Common costs, where there are competing non-primary production uses, such as council rates and utility charges are relevant and should be apportioned between the primary production and competing non-primary production uses of the land. Costs of labour and indirect costs actually incurred, such as fringe benefits or the cost of providing a farm hand with “free” board and lodgings should be taken into account.

Notional costs that are not actually incurred by the person who conducts the primary production do not have to be taken into account in considering whether a primary production enterprise realized profits[48]. For example, the cost of council rates which are not recovered by a landowner from the entity that conducts the primary production are not relevant in determining whether the primary production entity had a genuine intention to profit under s.10AA(2)(b). However, the fact that the landowner does not recover such costs from a primary production user may lead to a conclusion that the arrangements do not satisfy the “significant and substantial commercial purpose or character” and “purpose of profit” tests in s.10AA(2)(a)[49].

An intention to make a bare profit is not sufficient to satisfy either the “significant and substantial commercial purpose or character” test or the “purpose of profit” test in s.10AA(2)(a). The primary producer should have an intention to make a living or derive income or profit from the primary production use[50].

Rural land re-zoned for non-rural uses

Where rural land that has previously been exempt primary production land is rezoned for non-rural use, the exemption will continue if the continuing primary production activities satisfy both the dominant use and commercial tests.

However, the land may cease to be exempt if preparatory development of the land leading to subdivision has commenced, and the scale, extent, intensity and cost of the preparatory work or activity indicate that the main, chief or paramount use has changed from primary production to commercial land development. Preparatory work includes physical work or activities conducted on the land such as earthworks, but does not include seeking planning approval or development application unless associated physical activities such as surveying or testing of soil or water, or earthworks are conducted on the land.[51].

Landowners who own exempt rural land that is rezoned from rural to non-rural should lodge a return with the Chief Commissioner, including details of the rezoning and the primary production use of the land. This will ensure the Chief Commissioner reviews eligibility of the land for exemption and may avoid a tax default by the owner, which may result in multiple prior year assessments being issued, including assessment of penalty tax and interest.

Onus of proof and record-keeping requirements

The onus of proving that land qualifies for the primary production exemption rests with the owner of land, even if another person conducts the primary production activities on the land[52]. If another person uses the land, the owner is responsible for obtaining detailed information about that other person’s use of the land, including details of non-primary production uses.

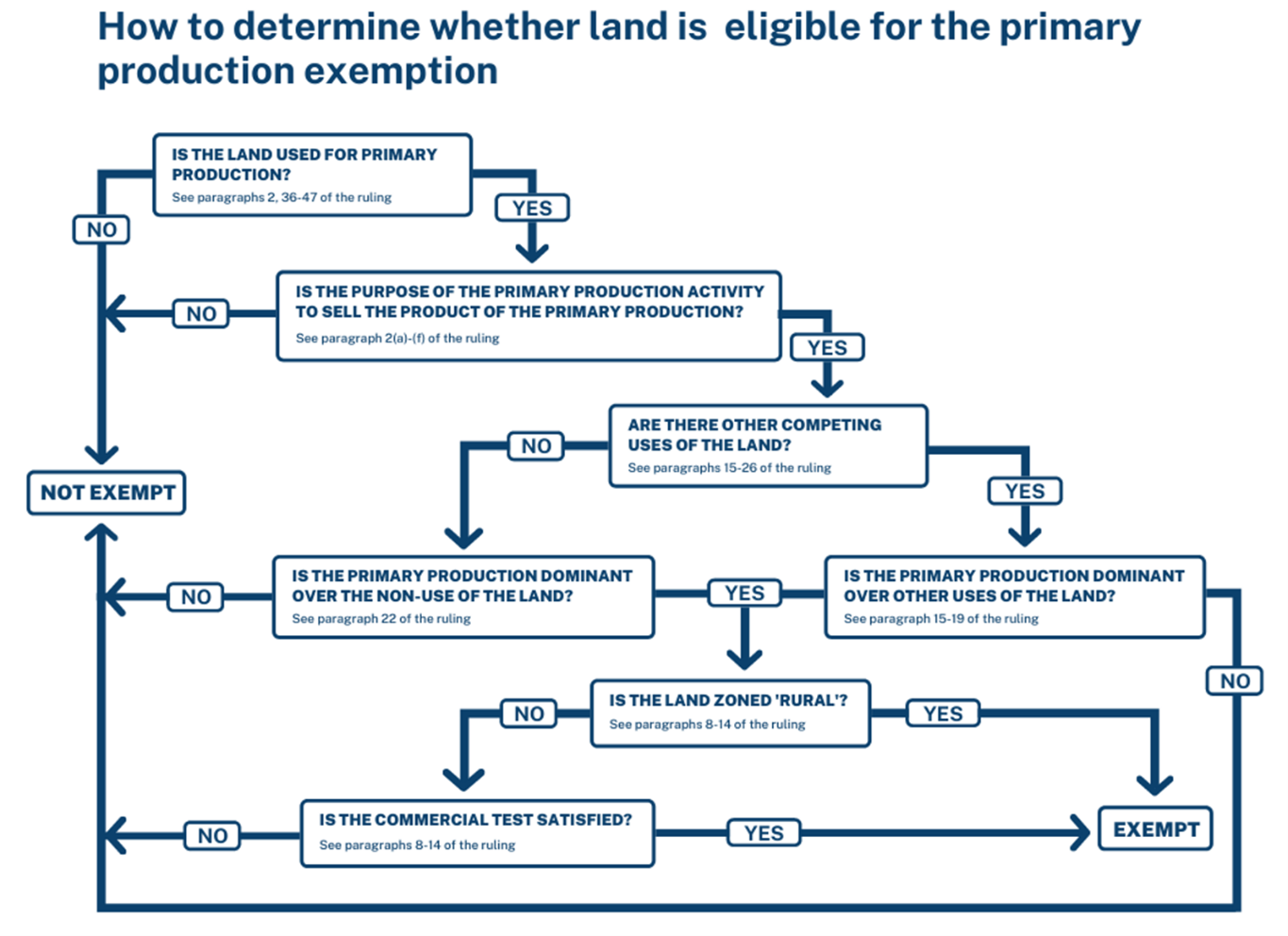

Flow Chart

Attached is a flow chart which demonstrates the decisions which have to be made in considering whether or not the use of land satisfies the requirements necessary to qualify for the PPL exemption under s.10AA.

Footnotes

^ Triston Pty Ltd atf The Ghantous Family Trust v Chief Commissioner of State Revenue [2017] NSWCATAD 100 at [44]; Triston Pty Limited v Chief Commissioner of State Revenue [2018] NSWCATAP 37 at [50].

^ See Thomason v Chief Executive, Department of Lands [1995] QLAC 4; (1995) 15 QLCR 286 at 303.

^ See Leda Manorstead v Chief Commissioner [2010] NSWSC 867 at 69 & 70

^ See Thomason v Chief Executive, Department of Lands (1994-1995) 15 QLCR 286 at 303.

^ See Chief Commissioner of State Revenue v Metricon Qld Pty Ltd [2017] NSWCA 11 at 63.

^ See Newcastle City Council v Royal Newcastle Hospital ([1959] AC 248 at 255.

^ See Leda Manorstead v Chief Commissioner [2010] NSWSC 867.

^ Leppington Pastoral Co Pty Ltd v Chief Commissioner of State Revenue [2017] NSWSC 9 at 178.

^ See Metricon Qld Pty Limited v Chief Commissioner of State Revenue (No. 2) [2016] NSWSC 332 at 71 and 82.

^ See Leda Manorstead v Chief Commissioner [2010] NSWSC 867 at 76, Hope v Bathurst City Council (No 2) (1983) 52 LGRA 79 at 84.

^ See Brown v Commissioner of Land Tax (1977) 7 ATR 642.

^ See McIntosh Bros Pty Ltd (In Liq) v Chief Commissioner of State Revenue [2019] NSWCATAD 124 at 148 and 171; Chief Commissioner of State Revenue v McIntosh Bros Pty Ltd (in liq) [2021] NSWCA 221 at 17-20.

^ Leda Manorstead v Chief Commissioner [2010] NSWSC 867 at 71.

^ See Greenville Pty Ltd v Commissioner of Land Tax (1977) 7 ATR 278.

^ Leda Manorstead v Chief Commissioner [2010] NSWSC 867 at 4.

^ Saville v Commissioner of Land Tax (1980) 12 ATR 7.

^ See Leda Manorstead v Chief Commissioner of State Revenue [2010] NSWSC 867 at 61

^ See Safety Beach Estate Pty Ltd v Commissioner of Land Tax 79 ATC 4032.

^ See Caruana v Chief Commissioner of State Revenue [2011] NSWADT 183 at 44.

^ See Leda Manorstead v Chief Commissioner [2010] NSWSC 867 at 4.

^ Greenville Pty Ltd v Commissioner of Land Tax (1977) 7 ATR 278.

^ See Longford Investments Pty Ltd v Commissioner of Land Tax 78 ATC 4264; Leda Manorstead v Chief Commissioner of State Revenue [2010] NSWSC 867 at 4.

^ See Quito Pty Ltd v Commissioner of State Revenue [2014] WASAT 8 at 109-115.

^ Thomason v Chief Executive, Department of Lands (1994-1995) 15 QLCR 286.

^ Vartuli & Anor v Chief Commissioner of State Revenue [2014] NSWSC 678 at 36; Chief Commissioner of State Revenue v McIntosh Bros Pty Ltd (in liq) [2021] NSWCA 221 at [22].

^ See Safety Beach Estate Pty Ltd v Commissioner of Land Tax (N.S.W.) 79 ATC 4032.

^ See Caruana v Chief Commissioner of State Revenue [2011] NSWADT 183, at 40-53.

^ Illawarra Meat Co Pty. Ltd. v Commissioner of Land Tax (1979) 1 NSWLR 188.

^ See Burnside and Marakai Ltd v Federal Commissioner of Taxation (1957) 11 ATD 181.

^ Godolphin Australia Pty Ltd v Chief Commissioner of State Revenue [2022] NSWSC 430 at 104.

^ see Reysson Pty Ltd v Chief Commissioner of State Revenue (RD) [2009] NSWADTAP 17.

^ See Lease A Leaf Property Pty Limited v Chief Commissioner of State Revenue (RD) [2011] NSWADTAP 41 at 36.

^ See Lease A Leaf Property Pty Limited v Chief Commissioner of State Revenue (RD) [2011] NSWADTAP 41 at 37-38.

^ See Maraya Holdings Pty Ltd v Chief Commissioner of State Revenue [2013] NSWSC 23 at 73; Thomason v Chief Executive, Department of Lands (1995) 15 QLCR 286 at 307.

^ Maraya Holdings Pty Ltd v Chief Commissioner of State Revenue [2013] NSWSC 23 at 76.

^ Leda Manorstead v Chief Commissioner [2010] NSWSC 867 at 4.

^ Chief Commissioner of State Revenue v McIntosh Bros Pty Ltd (in liq) [2021] NSWCA 221 at 21.

^ See Maraya Holdings Pty Ltd v Chief Commissioner of State Revenue [2013] NSWSC 23 at 86-90.

^ See Maraya Holdings Pty Ltd v Chief Commissioner of State Revenue [2013] NSWSC 23 at 99 to 101; Maraya Holdings Pty Ltd v Chief Commissioner of State Revenue [2013] NSWCA 408 at 66; McIntosh Bros Pty Ltd (In Liq) v Chief Commissioner of State Revenue at [2019] NSWCATAD 124 at 178.

^ See Maraya Holdings Pty Ltd v Chief Commissioner of State Revenue [2013] NSWSC 23 at 73; Vartuli v Chief Commissioner of State Revenue [2014] NSWSC 678 at 36; Leppington Pastoral Co Pty Ltd v Chief Commissioner of State Revenue [2017] NSWSC 9 at 48; Chief Commissioner of State Revenue v McIntosh Bros Pty Ltd (in liq) [2021] NSWCA 221 at 25; Fitzpatrick Investments Pty Ltd v Chief Commissioner of State Revenue [2021] NSWCATAD 315 at 126-127.

^ See Fitzpatrick Investments Pty Ltd v Chief Commissioner of State Revenue [2021] NSWCATAD 315 at 136-161; McIntosh Bros Pty Ltd (In Liq) v Chief Commissioner of State Revenue [2019] NSWCATAD 124 at 215-224.

^ McIntosh Bros Pty Ltd (In Liq) v Chief Commissioner of State Revenue [2019] NSWCATAD 124 at 241-242.

^ Maraya Holdings Pty Ltd v Chief Commissioner of State Revenue [2013] NSWSC 23 at 74.

^ See Maraya Holdings Pty Ltd v Chief Commissioner of State Revenue [2013] NSWSC 23 at 73; Chief Commissioner of State Revenue v McIntosh Bros Pty Ltd (in liq) [2021] NSWCA 221 at 25.

^ Maraya Holdings Pty Ltd v Chief Commissioner of State Revenue [2013] NSWSC 23 at 107-108.

^ See for example Maraya Holdings Pty Ltd v Chief Commissioner of State Revenue [2013] NSWSC 23 at 90-108.

^ Chief Commissioner of State Revenue v McIntosh Bros Pty Limited (in liq) [2020] NSWCATAP 124 at 112.

^ Chief Commissioner of State Revenue v McIntosh Bros Pty Limited (in liq) [2020] NSWCATAP 124 at 119.

^ Chief Commissioner of State Revenue v McIntosh Bros Pty Ltd (in liq) [2021] NSWCA 221 at 45.

^ See Explanatory Note to the Local Government (Rates and Charges) Amendment Bill 1988, which introduced similar provisions into the Local Government Act 1919.

^ See Leda Manorstead v Chief Commissioner [2010] NSWSC 867 at 61.

^ Sections 88, 100(3) and 100(4) of the Taxation Administration Act 1996.