Transfers in relation to Managed Investment Schemes

Section 54A of the Duties Act 1997

|

Ruling number

|

DUT 049

|

|

Tax/benefit

|

Duties

|

|

Type

|

Duties

|

|

Date issued

|

June 2020

|

|

Issued by

| Scott Johnston

Chief Commissioner of State Revenue

|

|

Effective from

|

June 2020

|

|

Effective to

| 4 September 2023 |

|

Status

| Superseded by DUT 49 v2 |

Preamble/Background

- This ruling provides background and guidance on the application of section 54A of the Duties Act 1997 (“the Act”), ‘Transfers in relation to managed investment schemes’.

- Section 54A of the Act provides for concessional duty of $50 in respect of certain transfers of dutiable property (and in the case of section 54A(3) statutory vestings of land in NSW) in relation to the administration of a managed investment scheme (“MIS”).

- Each of the transfers of dutiable property to which the section applies involves an ‘internal’ transfer of the dutiable property - comprising all or part of the scheme property of the relevant MIS - between different entities involved in the administration of the scheme or the holding of the scheme property; these entities include:

- the responsible entity,

- any custodian appointed by the responsible entity and

- any sub-custodian appointed by the custodian.

- The section also extends to analogous transfers between the trustee and custodian of any wholly owned sub-trust of the MIS [1] in which the scheme property may (and will often) be held.

- In general, the purpose of these transfers is to increase the efficiency of the holding of assets within a registered MIS group. None of these transfers involve any change in the ultimate beneficial ownership of the scheme property, which at all times resides with the members of the scheme. Hence, the legislative purpose of the concession is to allow these internal restructurings of the holding of the scheme property to occur free of ad valorem duty.

Note: Section 54A only applies to registered managed investment schemes and wholly owned sub-trusts of such registered schemes. Thus, if the particular MIS has never been registered under section 601EB of the Corporations Act or has been de-registered under section 601PA or section 601PB of that Act (and not reinstated under section 601PC of that Act) at the time of the relevant transfer, section 54A cannot apply to any transfer of dutiable property relating to that scheme.

Ruling

What dutiable transactions the different parts of section 54A apply to

Section 54A(1)(b) [2]- Prescribed Interest Schemes

- Section 54A(1)(b) imposes nominal (fixed) duty of $50 on a transfer of dutiable property from a person who held the dutiable property as a trustee of a prescribed interest scheme within the meaning of the Corporations Law as in force immediately before 1 July 1998 when the scheme became a registered scheme within the meaning of Division 11 of Part 11.2 of the Corporations Law (as continued in effect by section 1408 of the Corporations Act) to a custodian or agent of the responsible entity as custodian or agent of the scheme in which the transferor held the dutiable property.

- This transitional provision is referring to older investment schemes which were established prior to 1 July 1998 as prescribed interest schemes under the Corporations Law which on that date became registered schemes under the Corporations Law and later registered managed investment schemes under Chapter 5C of the Corporations Act (when the Corporations Act replaced the Corporations Law).

- Under section 54A(1)(b) of the Act, any transfer of the relevant dutiable property from the trustee of the former prescribed interest scheme (in whose name the property is registered) to a custodian or agent of the responsible entity of the MIS (as the scheme has since become) is liable to nominal duty of $50.

Section 54A(1)(a) - Responsible Entity to Custodian

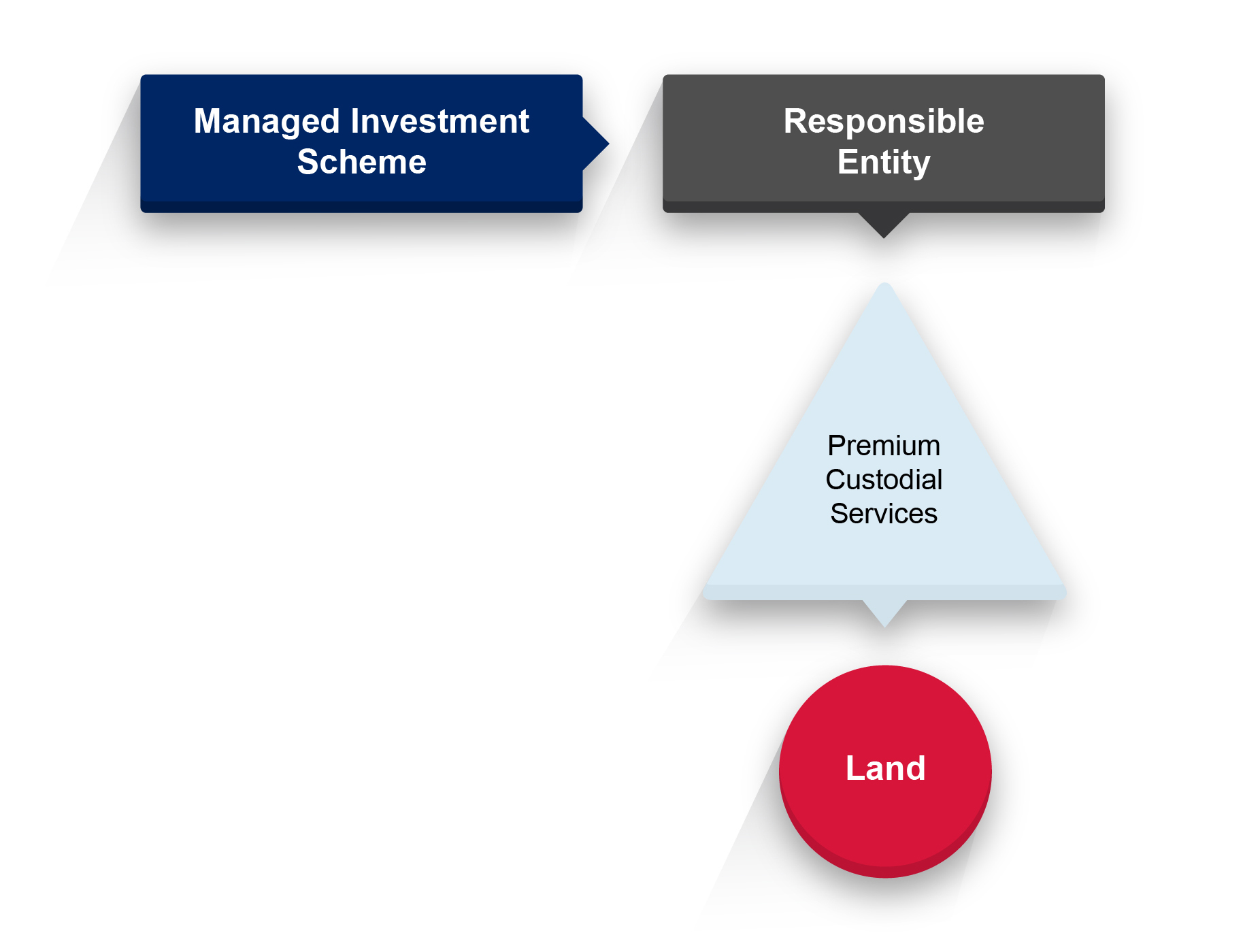

- Section 54A(1)(a) imposes nominal (fixed) duty of $50 on a transfer of dutiable property from a responsible entity of a MIS to a custodian or agent of the responsible entity as custodian or agent of the scheme in which the transferor held the dutiable property.

- This provision is self-explanatory, and applies in respect of a transfer of dutiable property -comprising all or part of the scheme property of the relevant managed investment scheme- from the responsible entity of the scheme to its custodian. Such a transfer will commonly occur upon the appointment of the transferee as the custodian of the scheme property.

- As the transfer instrument will usually be silent as to the capacity in which the transferee is taking the transfer -and the transferee might be a licensed custody services provider which acts as custodian for many different schemes- the Chief Commissioner may need to refer to additional sources in order to be satisfied of the respective roles of the parties to the transfer in the relevant MIS.Examples of acceptable sources include:

- a copy of the custody agreement (preferred);

- a letter from the board, legal counsel or legal advisor confirming the roles of the parties to the transfer;

- a statutory declaration by a person authorised to make statements on behalf of the custodian; or

- other evidence which in the opinion of the Chief Commissioner is sufficient to establish the roles of the parties to the transfer.

Example 1

By a custody agreement, the responsible entity of a MIS appoints an external custodian, Premium Custodial Services Ltd to hold the assets of the scheme which include land in NSW. The responsible entity then transfers this land to Premium Custodial Services Ltd. This transfer of dutiable property is liable to nominal duty of $50.00 under sec 54A(1)(a).

Section 54A(2) – Custodian to Responsible Entity

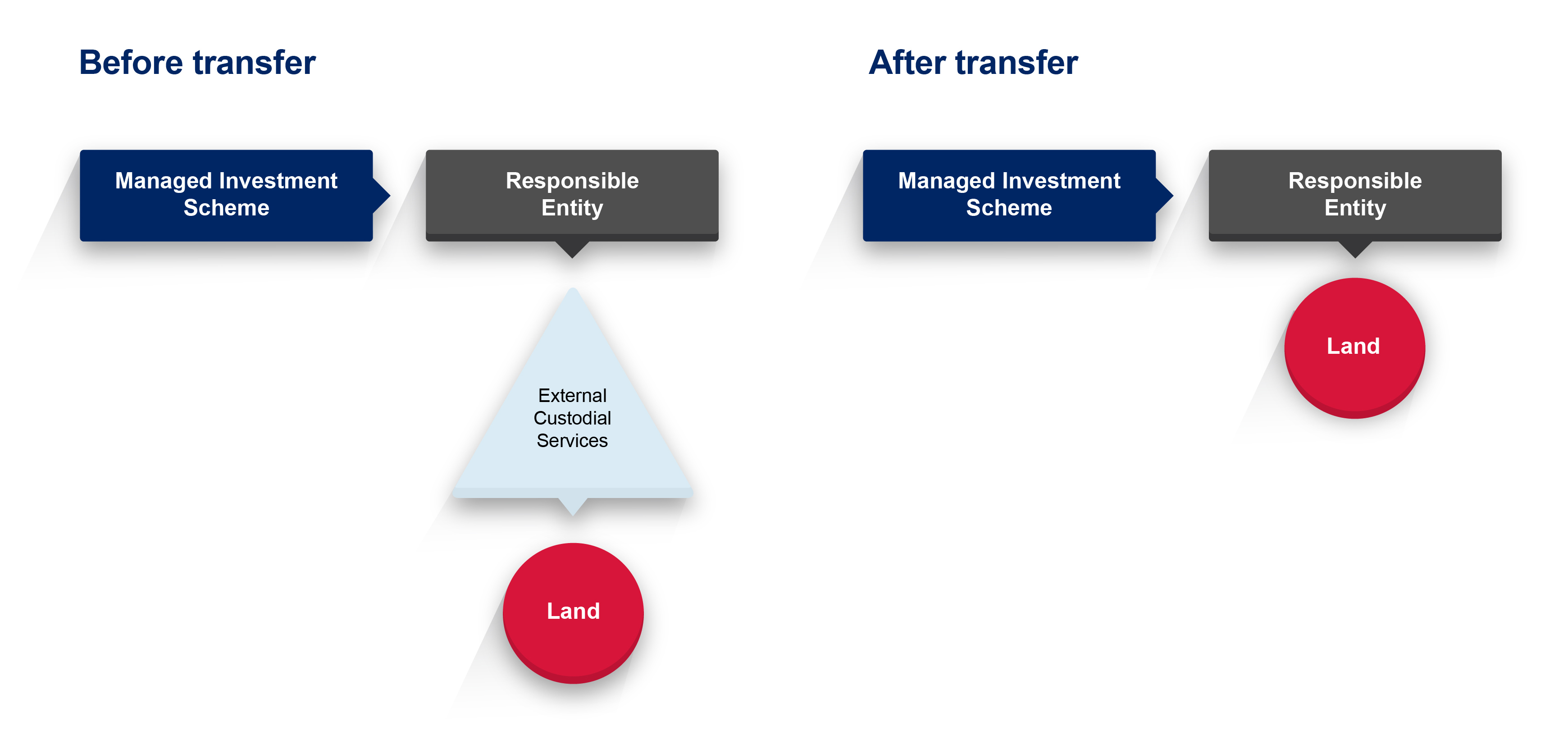

- Section 54A(2) imposes nominal (fixed) duty of $50 on a transfer of dutiable property (usually, land in NSW) from the custodian of the responsible entity of a MIS to the responsible entity.

- This commonly arises where there is a change in the identity of the custodian for the scheme (e.g. when the custodial function is internalised). In this situation, there may be an initial transfer of the dutiable property (comprising all or part of the scheme property) from the outgoing custodian to the responsible entity and then a second transfer of the same property from the responsible entity to the incoming custodian. Here, the first transfer (from the outgoing custodian to the responsible entity) will be liable to nominal duty of $50 under section 54A(2) and the second transfer (from the responsible entity to the incoming custodian) will be liable to nominal duty of $50 under section 54A(1)(a). If the responsible entity of the scheme (as distinct from another company in its corporate group) has decided to act as its own custodian then the second transfer will be unnecessary, but the first transfer will still fall within section 54A(2).

- As with section 54A(1)(a), it may be necessary to consult external sources in order to be satisfied as to the respective roles of the parties to the transfer in relation to the MIS concerned.

Example 2

The assets of a MIS include land in NSW which was acquired in the name of External Custodial Service appointed by the responsible entity of the scheme. With the view to minimising administrative costs, the responsible entity decides to terminate the existing custodial arrangements and act as its own custodian (for which it meets the requisite legislative requirements including holding an AFSL). The custodian then transfers the land to the responsible entity. This transfer is liable to nominal duty of $50 under sec.54A(2) of the Act.

Section 54A(3) - Vesting of Land

- Section 54A(3) imposes nominal (fixed) duty of $50 in respect of any vesting of land in NSW by statute law (as referred to in section 8(1)(b)(vii) of the Act) in a responsible entity if the Chief Commissioner is satisfied that subsection (2) would apply in respect of the dutiable transaction if it were a transfer of dutiable property.

- This provision refers to the situation where the relevant dutiable transaction (under section 8(1)(b)(vii) of the Act) is a statutory vesting of land in NSW in the responsible entity of the MIS rather than a direct transfer of this dutiable property.

- In this situation, if a direct transfer of the land in NSW (presumably involving the responsible entity and the person in whom the land was previously vested) would qualify for nominal duty of $50 under section 54A(2) of the Act then the statutory vesting of the land in the responsible entity will also be liable to nominal duty of $50.

Section 54A(4) – Sub-custodian to Custodian

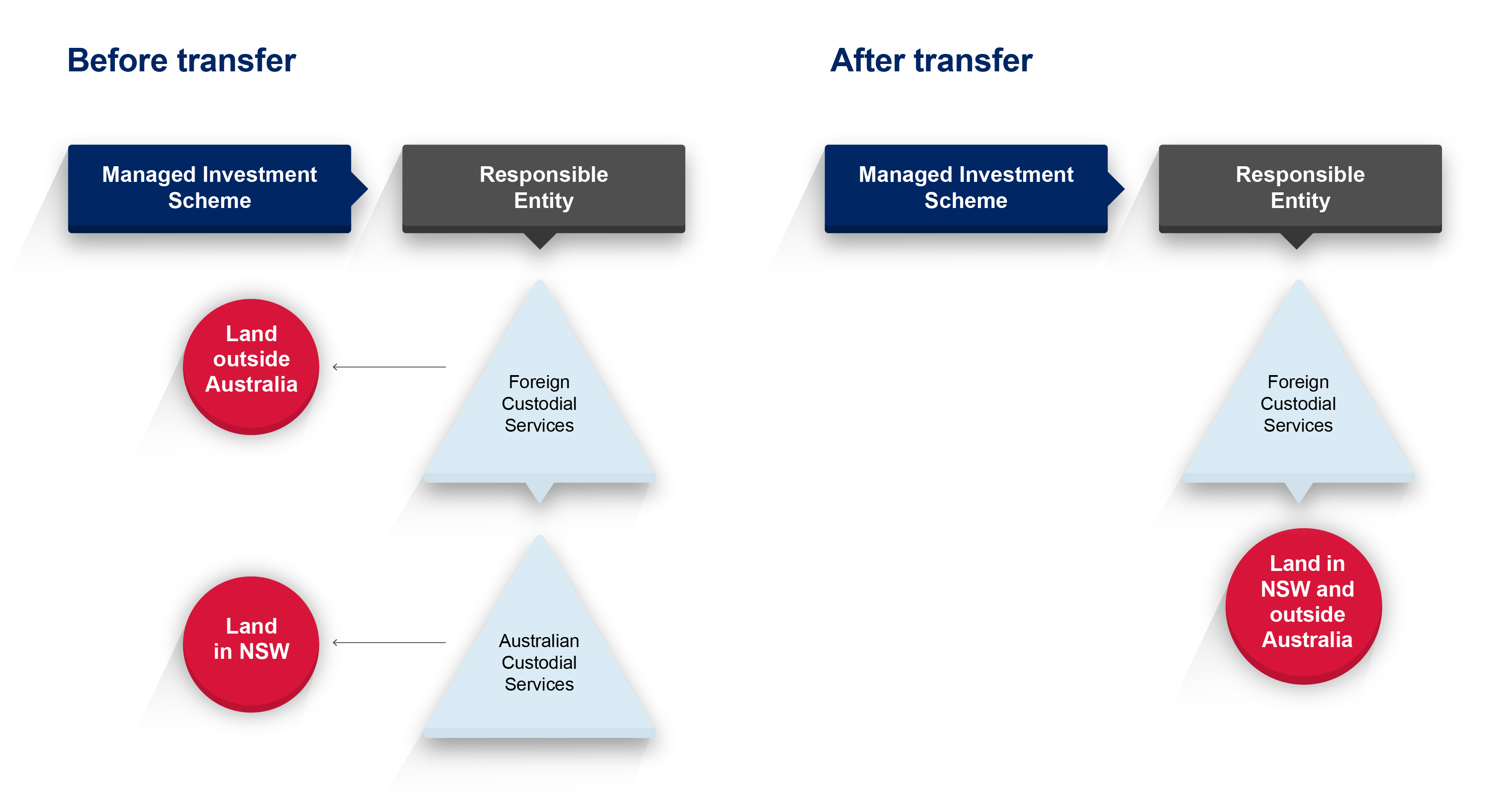

- Section 54A(4) imposes nominal (fixed) duty of $50 on a transfer of dutiable property from the sub-custodian of a custodian of the responsible entity of a MIS to a custodian of the responsible entity of the MIS.

- This provision refers to the situation where the relevant dutiable property - comprising all or part of the scheme property of the relevant MIS - is registered in the name of a sub-custodian of the custodian of the responsible entity of the scheme, and the sub-custodian then transfers the property to the custodian.

- A common situation where such a transfer will occur is where the existing sub-custodial arrangements with respect to the holding of the scheme property have been terminated (necessitating the vesting of the dutiable property in the custodian).

Example 3

The Responsible Entity of a registered MIS appoints Foreign Custodial Service as its custodian to hold the assets of the scheme, which include land in NSW as well as land outside Australia. The custodian appoints Australian Custodial Services (with the requisite AFSL) as its sub -custodian to hold the NSW land on its behalf. The sub-custodial arrangements are then terminated.

The resulting transfer of the NSW land from the sub-custodian to the custodian will be liable to nominal duty of $50 under sec.54A(4) of the Act.

Sections 54A(5)-(8) – Sub-trusts

- As already noted, secs.54A(5)-(8) deal with the situation where the relevant dutiable property is held through one or more wholly owned sub-trusts of the MIS.

- Section 54A(5) imposes nominal (fixed) duty of $50 on a transfer of dutiable property from a trustee of a wholly owned sub-trust of a MIS to a custodian of the trustee of that wholly owned sub-trust.

- Section 54A(6) -which is the reverse of sec.54A(5)- imposes nominal (fixed) duty of $50 on a transfer of dutiable property from a custodian of the trustee of a wholly owned sub-trust of a MIS to that trustee.

- Section 54A(7) provides that a reference (in secs.54A(5) and 54A(6)) to a wholly owned sub-trust of a MIS includes a sub-trust that is part of a chain of sub-trusts:

- that starts with a wholly owned sub-trust of a managed investment scheme, and

- in which a link in the chain is formed if the sub-trust wholly owns the next sub-trust in the chain.

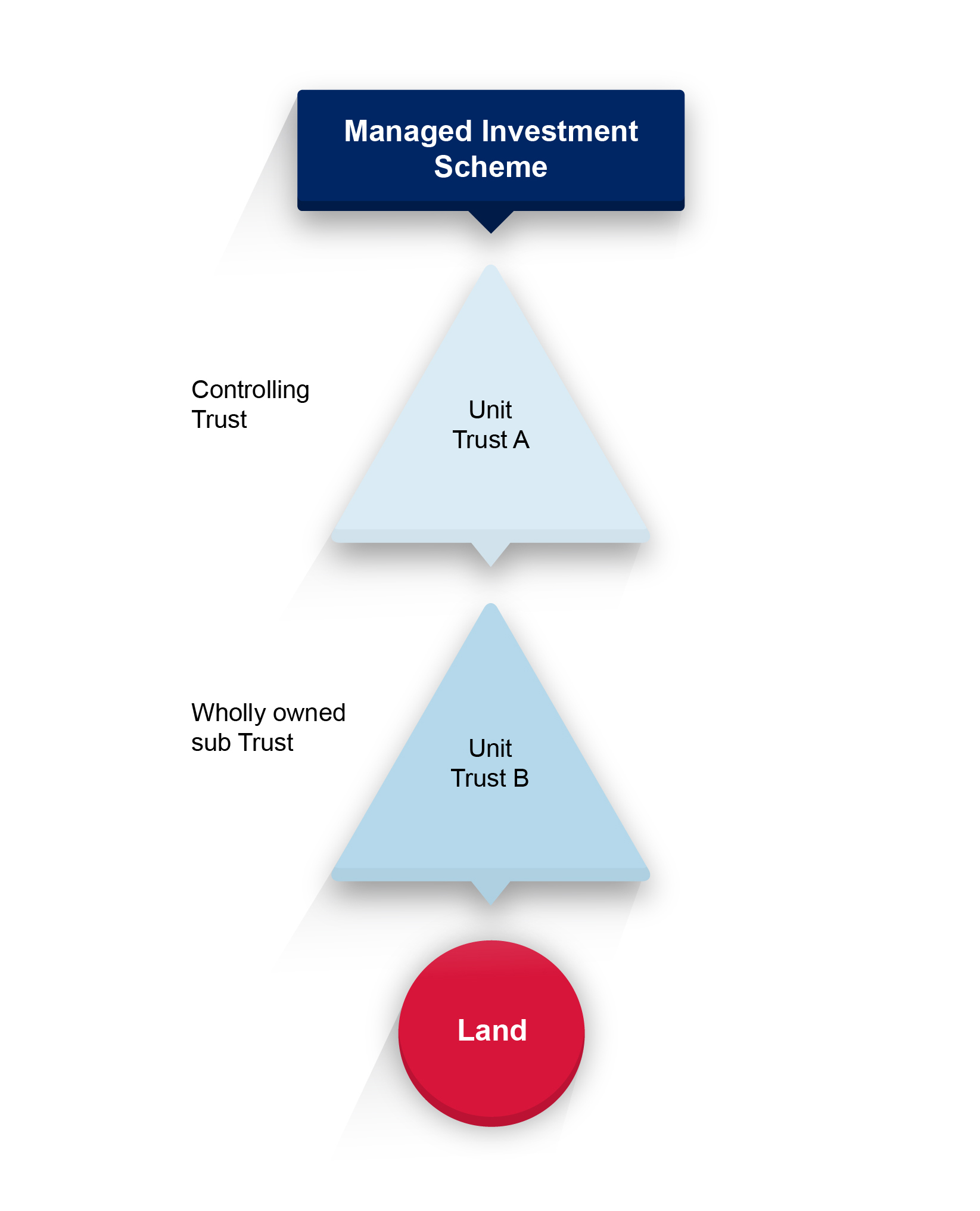

- By section 54A(8), a sub-trust is taken to be a “wholly owned” sub-trust of a managed investment scheme or sub-trust (the “controlling trust”) if the units in the sub-trust are wholly owned by the trustee of the controlling trust in the trustee’s capacity as trustee of the controlling trust.

- For example, assume a responsible entity of a MIS (or a custodian of the responsible entity) owns all the units in a unit trust (Unit Trust A) which holds land in NSW comprising scheme property. Unit Trust A is therefore a wholly owned sub-trust of the MIS. Accordingly:

- any transfer of the land in NSW from the trustee of Unit Trust A to its custodian will be liable to nominal duty of $50 under section 54A(5), and

- any transfer of the land in NSW from the custodian of the trustee of Unit Trust A to that trustee will be liable to nominal duty of $50 under section 54A(6) of the Act.

(In this way, secs.54A(5) and 54A(6) mirror secs.54A(1)(a) and 54A(2) of the Act, but at the level of the wholly owned sub-trust which actually holds the land.)

As section 54A(7) contemplates, there may be a chain of wholly owned sub-trusts of the management investment scheme.

Example 4

Unit Trust A (which is wholly owned by the MIS) owns all the units in Unit Trust B which holds the land in NSW which forms the scheme property of the MIS.

Unit Trust B, a wholly owned sub-trust of Unit Trust A (the controlling trust), will also be regarded as a wholly owned sub-trust of the MIS (sections 54A(7) & 54A(8)). Accordingly, any transfer of the land between the trustee and custodian of Unit Trust B (and vice versa) will be liable to nominal duty of $50 under section 54A(5) or 54A(6) of the Act (as the case may be).

Any transfer of the land between the trustee and custodian of Unit Trust B (and vice versa) will be liable to nominal duty of $50 under section 54A(5) or 54A(6) of the Act.

- However, sections 54A(5) and 54A(6) are not limited in their operation to the situation where (as in the above example) there is a wholly vertical chain of wholly owned sub-trusts of the managed investment scheme. The concession will also apply in respect of sub-trusts that are ultimately wholly owned by the managed investment scheme, but where the holding is split between other wholly owned sub-trusts. This interpretation of section 54A(7) is consistent with the underlying policy objectives of the concession. [3]

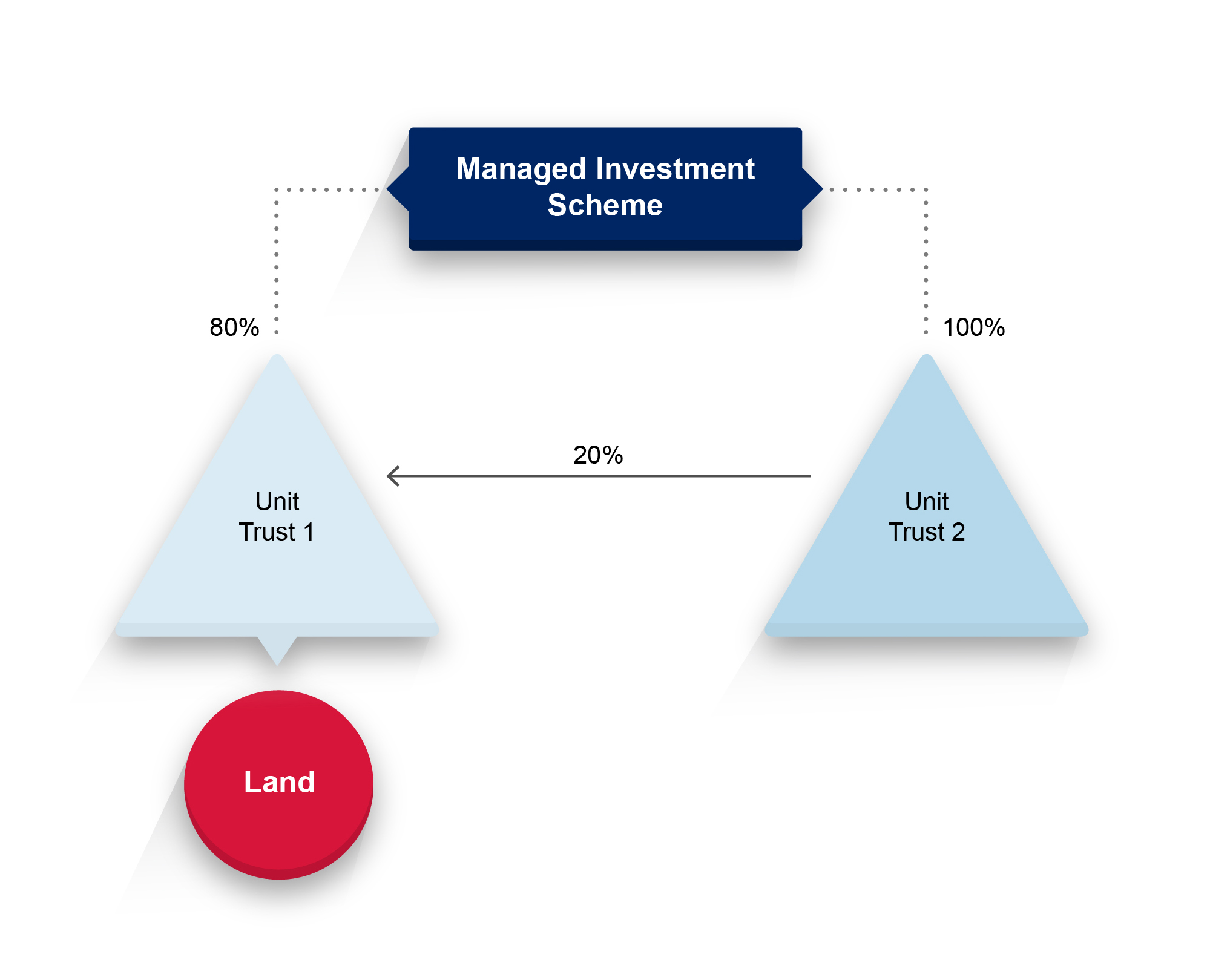

Example 5

The MIS holds 80 per cent of the units in a unit trust (Unit Trust 1) which holds the land in NSW which forms the scheme property of the MIS and 100 per cent of the units in another unit trust (Unit Trust 2) which holds the other 20 per cent of the units in Unit Trust 1. The MIS directly (through its 80 per cent unit holding in Unit Trust 1) and indirectly (through its 100 per cent unit holding in Unit Trust 2 which holds the other 20 per cent of the units in Unit Trust 1) holds 100 per cent of the units in Unit Trust 1. Accordingly, any transfer of the land actually held by Unit Trust 1 between the trustee and custodian of that trust (and vice versa) should also be regarded as falling within section 54A(5) or 54A(6) of the Act (as the case may be).

Any transfer of the land actually held by Unit Trust 1 between the trustee and custodian of that trust (and vice versa) should also be regarded as falling within section 54A(5) or 54A(6) of the Act.

Corresponding Landholder Duty Exemption (section 163A(1)(f))

- Chapter 4 of the Act charges duty (landholder duty) on certain acquisitions of interests (relevant acquisitions) in certain landholding entities.

- There are a number of exemptions from this duty. One of these is section 163A(1)(f), which provides that an acquisition by a person in a landholder is an exempt acquisition if it would be chargeable with duty of $50 under section 54 or section 54A if the property being acquired were land in NSW and the Chief Commissioner is satisfied that the acquisition is not part of a scheme to avoid duty under Chapter 4.

- ^ Often, the same corporation will act as the custodian of both the MIS and its wholly owned sub trust(s).

- ^ Historically speaking, it is logical to refer to sec.54A(1)(b) before sec.54A(1)(a).

- ^ It also makes the operation of section 54A(7) consistent with the definition (for landholder duty purposes) of a “linked entity” in sec.158 of the Act.