A new rebate has been made available from 4 September 2024. The rebate is available for medical centres who bulk bill a majority of their GP services. Click the arrow to find out more including detailed eligibility criteria.

An employment agency contract exists if an employment agent obtains a worker to provide services to a client for a fee. Under such a contract, the worker does not become an employee of the client.

A worker can also provide these services individually, or through a corporation or trust.

Employment agency contracts are used:

in a broad range of industry and business contexts

for skilled or unskilled work, and

for short or long-term engagements.

An employment agency contract may be:

written or oral

formal or informal, and/or

expressly made or implied.

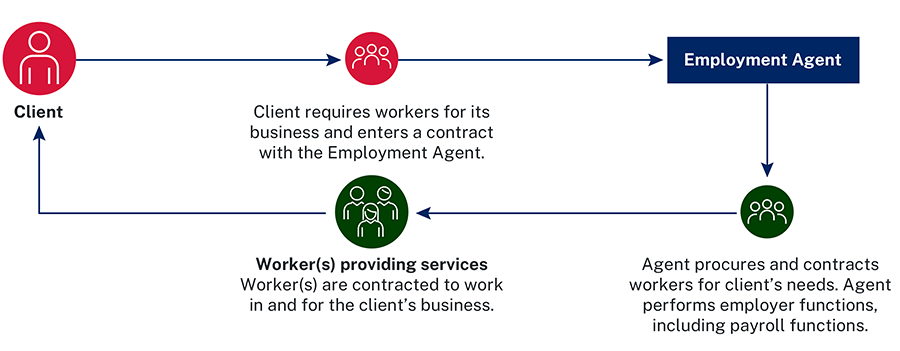

The diagram below shows a typical employment agency contract.

Diagram 1: The Client requires workers for its business and enters into a contract with an Employment Agent. The Employment Agent then procures and contracts workers, performing employer functions including payroll functions. The Workers are contracted to work in and for the Client’s business.

Employment agents may on-hire workers to government departments or bodies.

Payments to the on-hired workers are treated differently depending on which level of government is party to the arrangements.

Commonwealth Government

Although the Commonwealth Government is not subject to payroll tax, an employment agent is still liable for payroll tax on wages paid to workers on-hired to the Commonwealth Government.

The exemption in section 40(2) of the PTA does not apply since the Commonwealth Government is not specified as an exempt employer.

State Government

All State Government departments are liable for payroll tax in their respective state.

Employment agents must pay payroll tax on wages paid to workers on-hired to New South Wales government departments under an employment agency contract.

Local Government

Local government (municipal councils) are exempt from payroll tax except for wages related to certain activities outlined in section 60 of the PTA.

Employment agents are exempt from payroll tax on wages to workers on-hired to local government bodies so long as the workers are not engaged in the activities listed in section 60 of the PTA.

You need to correctly declare the wages paid to workers under employment agency contracts in your annual returns and monthly returns. For help in calculating the amounts follow these steps.

Errors may result in a tax default. If you have a tax default we will apply interest to the outstanding amount. Penalty tax may also be imposed. Read the interest and penalty tax page for more details.

Always maintain relevant records to verify the calculation methods you used to include payments to workers in your monthly returns and annual returns.

Step 1: Work out the taxable wages

When there is an employment agency contract, the employment agent must declare all wages paid to workers. Wages include:

gross salaries and wages

fringe benefits

employer superannuation contributions

termination payments

contractor payments

allowances

bonuses and commissions

directors’ fees

shares and options, and

apprentice and trainee wages.

Read the taxable wages section for more details about how to calculate each taxable wage.

Example 1 – worker is an individual

A client pays $12,000 to an employment agency and the employment agency pays $10,000 to the worker.

The liable employer is the employment agency and the $10,000 is a liable wage.

Example 2 – worker is engaged through a company

A client pays $1 million to an employment agency for the services of Andrew Green through Green Pty Ltd.

The agency pays $800,000 to Green Pty Ltd.

The liable wages of the employment agent should include the $800,000 paid by the agency to Green Pty Ltd.

Step 2: Work out the non-taxable payments

The following are not taxable wages and do not need to be declared in monthly or annual returns:

GST component of a payment.

Fees the client pays to an employment agency.

One-off fees paid by a client to a recruitment agency for placing a person with the client where the person becomes an employee of the client. Under this arrangement the client is responsible for any payroll tax liability.

ABC Nurses Pty Ltd (ABCN) is an employment agent that supplies nurses to major public and private hospitals under employment agency contracts.

In the 2023/24 financial year ABCN paid:

$5,000,000 in wages to nurses who provided services in public hospitals

$4,000,000 in wages to nurses who provided services in private hospitals (for profit), and

$1,000,000 in wages to nurses who provided services in non-profit hospitals operated by an association.

ABCN obtains declarations (PDF, 599.29 KB) from their public and non-profit hospital clients which confirms they are exempt employers. As such, ABCN is entitled to claim an exemption on the amounts it paid to nurses who provided services in those public and non-profit hospitals.

However, since the private (for profit) hospitals are not exempt employers, ABCN is liable for payroll tax on the $4,000,000 it paid in wages to nurses working in the private hospitals.

ABCN must also continue to declare liable wages paid to workers and employees:

who are providing services to ABCN such as administration roles

where workers have been supplied to clients who are not exempt from payroll tax, and

if a declaration for exempt clients is not obtained.

A chain of on-hire arrangement is where 2 or more employment agents stand between the worker and the client.

In most cases, the employment agent closest to the ultimate client (Agent 2 in the diagram below) will be regarded by Revenue NSW as the employment agent who is liable for payroll tax.

This declaration must be kept by Agent 1 for five years. Agent 1 must ensure that this declaration can be readily produced upon request by Revenue NSW.

If Agent 2 is below the payroll tax threshold and does not pay payroll tax, then Agent 1 would be liable.

The diagram below shows a typical example of a chain of on-hire.

Diagram 2: A linear representation of a chain of on-hire arrangement when there are 2 employment agents acting between the client and worker(s).

Example 4 – Chain of on-hire

A client business is seeking labour and pays $120,000 to Agent 2, which pays $110,000 to Agent 1 which pays $100,000 to the worker.

Agent 2’s wages are over the payroll tax threshold.

Only Agent 2 is liable and the liable wages are the $110,000 paid to Agent 1.

Payroll tax audits often uncover errors caused by misunderstandings of how the employment agency provisions apply. These include:

Businesses failing to realise that the employment agency provisions apply to their situation.

Employment agents not including payments to workers obtained through another business or company.

Misconceptions that employment agency contracts:

only apply to traditional “employment agents” or “labour hire firms” (as they are commonly understood)

cannot be results-based contracts

cannot be a fixed-price contract

only apply if the worker undertakes “core business activity” during normal trading hours, or

require the relationship between worker and client business be an employee-employer relationship.

Errors by industry

Certain industries frequently engage workers through employment agency contracts. Businesses in these industries often make errors when calculating their taxable wages. For more details, visit the following industry pages:

Example 5 – Business unaware that they are an employment agent

ABC Poultry Pty Ltd (ABC Poultry) operates a poultry processing facility and engages Chicken Deboners Pty Ltd (Chicken Deboners) to provide a team of workers to carry out chicken deboning and filleting during periods of high demand.

The agreement between ABC Poultry and Chicken Deboners has the following features:

The work is carried out in ABC Poultry facilities, following its general instruction and procedures.

Chicken Deboners supplies a supervisor and team of workers that operate in different shifts to ABC Poultry’s employees but carry out similar tasks.

Chicken Deboners workers bring their own knives and personal safety equipment but otherwise use benches and facilities of ABC Poultry.

ABC Poultry will make payment to Chicken Deboners based on a dollar amount per kilogram of processed cuts of meat.

ABC Poultry engages Chicken Deboners on a regular and continuing basis.

Chicken Deboners workers are a mix of employees and workers sourced through other subcontractor companies.

Chicken Deboners did not register for payroll tax because the wages it paid to its employees was below the payroll tax threshold.

It was also of the view that payments made to subcontractors were not subject to payroll tax because:

as companies running their own businesses, the subcontractors were responsible for payroll tax on their own workers

the contract was not primarily for supplying labour to ABC Poultry, but rather to produce a result (specified quantities of processed meat paid per kilogram)

they were not a traditional “employment agent” as it is commonly understood, and

it failed to consider whether the employment agency provisions applied.

A payroll tax audit of Chicken Deboners found it to be classified as an employment agent because:

Chicken Deboners expended care and effort in procuring the services of the workers for ABC Poultry, and

the workers were working in and for the conduct of ABC Poultry’s business and undertaking work in the same or similar way as ABC Poultry’s employees.

The fact that workers supplied by Chicken Deboners had their own shift supervisor and were paid by the volume of meat they processed did not preclude the finding that the contract was an employment agency contract.

Contact us to make a voluntary disclosure if you have not declared all liable amounts in your monthly and/or annual returns, including previous financial years.

Voluntary disclosures attract a reduced level of penalty tax compared to cases where we identify an underpayment. Interest will still be imposed.

Non-compliance identified through our data matching activities will result in penalty tax and interest charges, in addition to any underpayments detected.

Anti-avoidance provisions

The payroll tax anti-avoidance provisions apply where an arrangement reduces or avoids liability for payroll tax.

There does not need to be proof the arrangement was intentional. What matters is the effect the arrangement has on the payroll tax liability.

We examine the facts and circumstances of your business to work out whether to apply the provisions.

The Chief Commissioner may disregard the agreement, transaction or arrangements and determine that any:

party to the arrangement is taken to be an employer, and/or

payment in respect of the arrangement will be deemed taxable wages.