If you have been impacted by a natural disaster and require assistance with your fines or fees, call us on 1300 138 118 to discuss your options. Some online services will be unavailable on Sunday.

A new rebate has been made available from 4 September 2024. The rebate is available for medical centres who bulk bill a majority of their GP services. Click the arrow to find out more including detailed eligibility criteria.

Payment is due on the 7th day of the following month, or the next business day if the 7th day is on a weekend or public holiday.

Make your monthly returns easier

Save time calculating and paying monthly payroll tax. If you paid less than $150,000 in payroll tax during the previous financial year you can use the estimate wages method to calculate your liability.

Simplify your payments by setting up a direct debit to ensure your July to May payments are paid on time.

Annual payers

If your annual payroll tax liability for NSW is less than $20,000 you can pay your payroll tax annually.

All payroll tax customers must lodge an annual return

Regardless of whether you are a monthly or annual payer, you must lodge your annual return and pay using Payroll Tax Online by 28 July each year, or the next business day if the 28 July is on a weekend or public holiday.

Options for businesses in financial difficulty

Revenue NSW can assist customers who are having problems paying their payroll tax.

If your business is unable to pay its payroll tax due to unforeseen circumstances or financial hardship contact the payroll tax team before the due date of your payment or lodgement. You may avoid lodgement enforcement action and interest and penalty tax.

If your business is unable to pay the full amount of its payroll tax liability by the due date, we may be able to provide an extension or help you apply for a payment instalment plan.

Contact us to find out if your business is eligible to make payment by instalments.

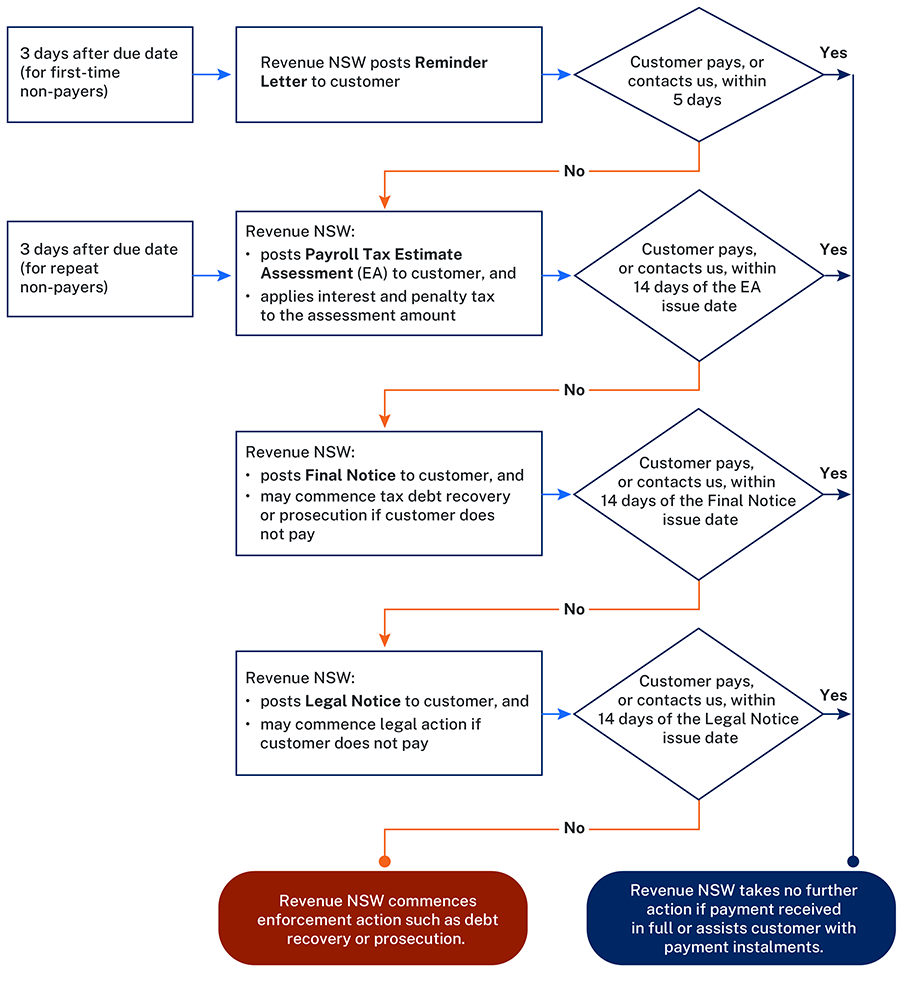

This flowchart shows the steps Revenue NSW will take to remind you of outstanding payroll tax liabilities.

The process ends when we receive payment or you contact us. The days in the chart are business days.

Flowchart 1: If you do not pay your payroll tax by the due date we will post a Reminder Letter to you within 5 business days. This is for first-time non-payers only. The letter will request the immediate payment of your outstanding payroll tax liability.

If you do not pay your payroll tax, or contact us, we will post a Payroll Tax Estimate Assessment (PTEA) to you. We post the PTEA 5 business days after the Reminder Letter for first-time non-payers. We post the PTEA 3 days after the due date for repeat non-payers. The PTEA will request payment of the estimate, or your actual payroll tax liability, within 14 days of the date of issue. Interest and penalty tax may be applied to the outstanding amount at this stage.

If you do not pay the PTEA, or contact us, we will post a Final Notice to you. The Final Notice will request payment of your outstanding payroll tax liability within 14 days of the date of issue. We may commence legal action if you do not pay.

If you do not pay the Final Notice, or contact us, we will post a Legal Notice to you. The Legal Notice will request payment of your outstanding payroll tax liability within 14 days of the date of issue. We may commence tax debt recovery or prosecution action if you do not pay.

Enforcement action

Please be aware that there are consequences if you do not pay your payroll tax on time.

A range of options are available to us. We will decide which action to take based on the circumstances of the individual business. Open the headings to read more.