A new rebate has been made available from 4 September 2024. The rebate is available for medical centres who bulk bill a majority of their GP services. Click the arrow to find out more including detailed eligibility criteria.

Interest and penalty tax is applied to taxpayers who commit a tax default under various taxation and revenue laws we administer. Larger penalties apply to businesses that are significant global entities.

On this page

A taxpayer commits a tax default by:

failing to make a payment (in whole or part) by the due date, or

failing to submit a return in accordance with a taxation law.

Interest and penalty tax rates

The rates of interest and penalty tax vary, depending on the circumstance of the tax default.

The level of interest and penalty tax applied should match the degree of culpability of the taxpayer.

For example, taxpayers who exercise reasonable care and voluntarily disclose their tax liability, as soon as they know, will have less interest and/or penalty tax imposed than those who do not.

Calculating the interest

Interest is calculated daily, from the end of the day on which the tax should have been paid until the day on which the tax is paid.

Interest is not calculated on unpaid interest – and is not payable if the amount of interest is less than $20.

There are two components of interest.

Market rate

The market rate is not regarded as a penalty but reflects the revenue lost by the government.

The market rate is adjusted in line with the 90-day bank-accepted bill rate published by the Reserve Bank in May, August, November and February, immediately before the commencement of each quarter.

Premium rate

The premium rate is imposed to deter non-compliance and ensure that defaulting taxpayers are not advantaged when compared to other taxpayers who meet their obligations.

Interest rates

View the rate of interest imposed for the past seven years.

We may reduce the market and premium rate if there is evidence that the tax default was beyond your control. For example, postal delays, natural disasters, and circumstances where it’s impossible to submit a return or pay on time (excluding financial incapacity).

The premium rate of interest may be reduced if there is evidence you took reasonable care, or made a voluntary disclosure before the commencement of an investigation. However, for the purposes of payroll tax, the premium rate of interest is not reduced. Please refer to revenue ruling PTA 036v3 for application of the interest and penalty provisions for payroll tax.

Write to us to request a reduction. It should detail the circumstances surrounding the default and reasons why the interest should be reduced.

When determining whether reasonable care was taken, we’ll consider whether you:

kept complete and accurate records

made a diligent effort to understand and comply with the law

sought expert advice on uncertain or complex matters

were honest in your dealings with us.

We’ll also consider your:

understanding of the law

commercial experience

access to expert advice.

Meeting one or more of these criteria does not necessarily mean that reasonable care has been taken. All factors leading to the tax default are taken into consideration.

Penalty tax

If a tax default occurs, a penalty tax may be payable.

A penalty tax is not imposed on interest or on any penalty tax already imposed. The penalty tax will be:

nil, where there is evidence that:

the tax default occurred because of circumstances beyond your control

you took reasonable care to comply with the law

up to 30 per cent, depending on the circumstances, where you failed to take reasonable care but there was no intentional disregard of the law

between 15 and 90 per cent, depending on the circumstances, where you intentionally disregarded the law.

What is intentional disregard of the law?

You intentionally disregard of the law when you:

make false or misleading statements or keep false records

conceal relevant facts

commit deliberate acts of non-compliance

fail to keep relevant records in English for the required period, or make them easily accessible

ignore a private ruling

fail to meet a tax liability after being told about it.

Penalty tax rates

No penalty tax will be imposed where a voluntary disclosure is made in writing before the commencement of an investigation, unless there is intentional disregard of the law.

Where reasonable care is not taken but no intentional disregard of the law

20% if a voluntary disclosure is made in writing during an investigation

25% if a voluntary disclosure is made after an investigation

30% if you take steps to hinder the Chief Commissioner's investigation after being advised that an investigation is to be carried out

Where there is intentional disregard of the law

15% if a voluntary disclosure is made in writing before an investigation has commenced

60% if a voluntary disclosure is made during an investigation

75% if a voluntary disclosure is not made

90% if you take steps to hinder the Chief Commissioner's investigation after being advised that an investigation is to be carried out.

Penalty tax reduction

You are entitled to a reduction in penalty tax if you voluntarily make a written disclosure that enables the Chief Commissioner to determine the nature and extent of the tax default.

The rate of penalty tax is reduced by:

80 per cent if the written disclosure is made before the Chief Commissioner commences an investigation, and

20 per cent if it is made after the Chief Commissioner commences an investigation.

This does not apply to registered taxpayers if a voluntary disclosure is made after a failure to lodge a return or pay tax in accordance with the relevant legislation.

To get the penalty tax reduced, write to us outlining reasons why.

Significant global entities

Amendments made to the Taxation Administration Act 1996 (TAA) in May 2022 apply a higher rate of penalty tax to customers who are “Significant Global Entities” (SGE).

SGEs are large businesses that have an annual global income of A$1 billion or more, including any smaller entities that are part of the larger global group.

Grouping for SGE purposes is established through accounting principles instead of grouping provisions under State tax legislation.

Section 27 of the TAA refers to the Income Tax Assessment Act 1997 (ITAA) for defining an SGE.

The information below consists of extracts from the Australian Taxation Office (ATO) website. For more detailed information, visit the ATO page for SGEs.

SGEs are defined in Subdivision 960-U of the ITAA. An entity is an SGE for a period if it is any of the following:

a global parent entity (GPE) with an annual global income of A$1 billion or more

a member of a group of entities consolidated for accounting purposes as a single group and one of the other group members is a GPE with an annual global income of A$1 billion or more

a member of a notional listed company group and one of the other group members is a GPE with an annual global income of A$1 billion or more.

An SGE can be a public or private company, a trust, a partnership, or an individual.

Global parent entity

A global parent entity (GPE) is an entity that is not controlled by another entity according to Australian or commercially accepted accounting principles (CAAP).

Note, grouping provisions under State tax legislation are not relevant in determining if an entity is part of a group for SGE purposes. For more details, see the Determining grouping control using accounting principles section.

A GPE is usually a member of a group of entities. However, a GPE may be a single entity that does not control any other entities.

Notional Listed Company Group

A notional listed company group is a group of entities that would be required to be consolidated as a single group for accounting purposes if a member of that group were a listed company.

Annual Global Income

Annual global income is the total annual income of the entity (if not grouped), or the consolidated group as a whole, as disclosed in the GPE’s latest “global financial statements”.

Amounts shown in global financial statements in currencies other than Australian dollars must be converted into Australian currency, at the average exchange rate for the period for which the statements are prepared.

The annual global income is the total of income that goes to the determination of profit or loss in accordance with Accounting Standard AASB 101. Typically, this would include:

revenue

gains from investment activities

other inflows that go to the determination of the profit or loss.

Global Financial Statements

The financial statements of a GPE for an income year are global financial statements if they are prepared and audited in accordance with either:

Australian accounting standards and auditing principles, or

if Australian accounting standards and auditing principles do not apply, with other commercially accepted principles relating to accounting and auditing.

Determining grouping control using accounting principles

Whether an entity controls other entities is a factual matter determined by the application of Australian accounting principles or other applicable commercially accepted accounting principles (CAAP).

In most cases, assessing control should be straightforward, such as where control is clear by virtue of the ownership of the majority of the voting power in a company.

In other cases, assessing control can be more complex, such as when the control arises from one or more contractual arrangements. In such cases, the elements outlined in Appendix B of AASB 10 may be relevant to determining control.

Paragraphs B2–B4 of AASB 10 were updated on 2 March 2020 and provide the framework for assessing control as follows:

B2 - An investor controls an investee if and only if the investor has all the following characteristics:

Power over the investee.

Exposure, or rights, to variable returns from its involvement with the investee.

The ability to use its power over the investee to affect the amount of the investor's returns.

B3 - Consideration of the following factors may assist in making that determination:

the purpose and design of the investee (see paragraphs B5–B8)

what the relevant activities are and how decisions about those activities are made (see paragraphs B11–B13)

whether the rights of the investor give it the current ability to direct the relevant activities (see paragraphs B14–B54)

whether the investor is exposed, or has rights, to variable returns from its involvement with the investee (see paragraphs B55–B57), and

whether the investor has the ability to use its power over the investee to affect the amount of the investor’s returns (see paragraphs B58–B72).

B4 - When assessing control of an investee, an investor shall consider the nature of its relationship with other parties (see paragraphs B73–B75).

SGE status determined at the end of the assessing period

Following ATO rules, the question of whether an entity is an SGE is determined with reference to the circumstances at the end of the relevant assessment period. The relevant period may be anywhere from one month to a whole tax year.

For an assessment covering a whole financial year ending 30 June, the circumstances of the entity as at 30 June will determine if the entity is an SGE.

For an assessment covering part of a financial year (e.g. 1 July to 31 December), the circumstances of the entity at the end of the relevant period (i.e. 31 December) is used to determine if the entity is an SGE.

For a period covering only one month, the circumstances at the end of that month determine if the entity is an SGE.

Joining and leaving groups during an assessing period

If an entity joins an SGE group part way through an assessing period, it is considered an SGE entity for the whole assessing period.

If an entity leaves an SGE group part way through an assessing period, its status at the end of the assessing period (SGE or not) will determine its status for the whole assessing period.

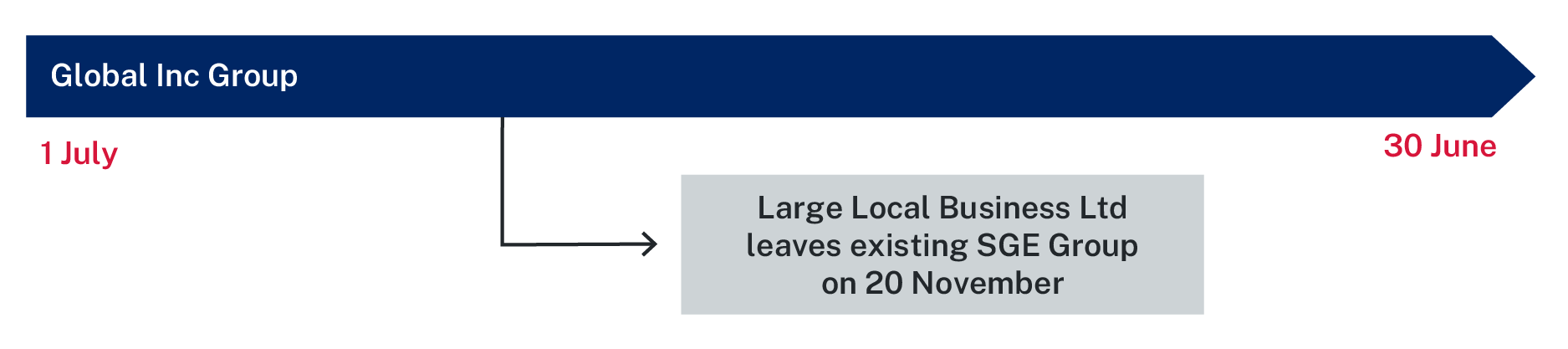

Example scenarios

Small Local Business Pty Ltd – less than $1bn income, not an SGE on its own.

Large Local Business Ltd – more than $1bn income, is an SGE on its own.

Global Inc Group – large global group with more than $1bn income and is an SGE on its own

Small entity joins an SGE group

The status of the Small Local Business Pty Ltd status for whole period assessment is SGE.

Small Entity leaves an SGE group

The status of the Small Local Business Pty Ltd for whole period assessment is not an SGE.

Large Entity leaves SGE group

The Large Local Business Ltd status for whole period assessment is SGE (because it is an SGE in its own right).

Paying a penalty

If you owe money and are unable to pay the amount in full, we will negotiate an appropriate payment arrangement.

For short-term payment arrangements, write to us with your financial information (including detailed cash flow projections).