Visit the key dates for payroll tax webpage and schedule these dates in your calendar to avoid missing lodgement dates and additional costs associated with late lodgement.

Learn more about becoming a shared equity partner approved by the Chief Commissioner of State Revenue, to support home buyers in purchasing property in NSW.

Chapter 8, Part 2 of the Duties Act 1997 (‘Act’) charges duty on life insurance policies and life insurance riders.

Life insurance is defined in section 240 of the Act to mean insurance described in section 9 (1) (a)–(g) and 9A of the Commonwealth Life Insurance Act 1995, in respect of a life or lives, or any event or contingency relating to or depending on a life or lives of a person whose principal place of residence is, or persons whose principal places of residences are, in New South Wales at the time the policy that effects the insurance is issued.

Life policy as defined in section 9 (1) (a)-(g) of the Life Insurance Act 1995 means:

a contract of insurance that provides for the payment of money on the death of a person or on the happening of a contingency dependent on the termination or continuance of human life;

a contract of insurance that is subject to payment of premiums for a term dependent on the termination or continuance of human life;

a contract of insurance that provides for the payment of an annuity for a term dependent on the continuance of human life;

a contract that provides for the payment of an annuity for a term not dependent on thecontinuance of human life but exceeding the term prescribed by the regulations;

a continuous disability policy;

a contract (whether or not it is a contract of insurance) that constitutes an investment account contract;

a contract (whether or not it is a contract of insurance) that constitutes aninvestment‑linked contract.

Note: A contract that provides for the payment of money on the death of a person is not a life policy if:

by the terms of the contract, the duration of the contract is to be not more than one year; and

payment is only to be made in the event of:

death by accident; or

death resulting from a specified sickness.

A life insurance rider is defined in section 241 of the Act as insurance that is attached to a policy of life insurance, adds specified events and contingencies to those insured under the policy and is subject to the terms and conditions of the policy. The life insurance rider may be classified as life insurance (in addition to the main life insurance purpose of the life insurance policy) but will not be a ‘life insurance policy’.

This ruling explains the characteristics of life insurance riders. It broadly reflects Revenue Ruling SD 185 and takes into account the commencement of the Duties Act in 1997.

Ruling

Life Insurance Riders

A life insurance rider is insurance which would otherwise be general insurance or life insurance in addition to the main life insurance purpose of the policy and would be subject to the respective rates of duty that apply to those types of insurance policies but for satisfying the definition in section 241 of a life insurance rider.

Life insurance riders are chargeable with duty of 5% of the first year’s premium. To be classified as a rider, the 3 main conditions of the policy as defined in section 241 of the Act must be satisfied. These are:

“Attached to a policy of life insurance”

A life insurance rider is an additional insurance cover attached to a life insurance policy. Some of the factors that generally identify riders are that they are:

additional insurance to the main life insurance purpose of the policy to which they are attached

integrated with the life insurance policy

joined or connected to the life policy

add-ons to suit specific needs, which (as expressed in the policy) do not stand-alone independent of the life insurance policy of which they form part

optional with a specifically identified additional premium, or a premium which is severable and identifiable and

approved by APRA as if it were a class of life insurance business. (Under section 12A of the Life Insurance Act 1995, on an application by a company, APRA may declare that the company is a life insurance business. The declaration will also include any riders that are attached to the life policy.)

Some typical riders although not an exhaustive list, include

total and permanent disability

crisis/trauma

accidental death

guaranteed insurability which provides insurance

waiver of premium in case of disablement

Note 1: If a cover is part of your main life insurance purpose of the policy and/or if they do not provide any additional financial benefit, then the cover is not a rider and premiums will be charged at the same rate as life insurance policies. Exceptions are where insurance is guaranteed to commence at a future time, which is subject to the life insurance rider rate of duty and an ‘option’ for the policy owner to apply for insurance at a future time, which is not subject to duty.

Note 2: If the additional insured cover is a stand-alone cover, separate from the main life insurance purpose of the policy, then it is not a rider and is subject to the appropriate rate of insurance duty.

“Adds specified events and contingencies to those insured under the policy”

The rider provides for insurance on a contingency or an event occurring that may not relate to or depend on a life of the insured or is additional to the continuous disability main purpose of the policy. In other words, the events covered may happen in the lifetime of the insured and are not limited to the death of the insured. If an event occurs and a payment is made on a rider, the life insurance policy may or may not remain intact.

The policy premium is waived and treated as if paid if an accident or illness resulted in total disability, for as long as the total disability persists.

If the insured person dies due to an accident, the specified cover is paid. If the insured person is the only person insured under the policy, the policy will end.

This ensures that the insured gets an early payment of the life insurance benefit cover if the life insured is diagnosed with terminal illness or is paid a benefit on diagnoses of a specified illness or condition and is still alive. As a result of such a payment the policy may or may not end.

This ensures that the insured gets an early payment of the life insurance benefit cover if the life insured becomes disabled as defined in the policy. As a result of such a payment the policy may or may not end.

“Subject to the terms and conditions of the policy”

The rider (although an additional insurance attached to the life insurance policy) must adopt the general terms and conditions of the life insurance policy that it is attached to. The life insurance policy terms and conditions will also include specific conditions relating to the policy insurance riders. If the rider is not included in the terms and conditions of the life insurance policy, then it is not a rider.

For some types of life insurance rider, if the same sum insured benefit is paid for any other reason, apart from the death of the insured, the other benefits included in the policy are generally reduced by the amount already paid out. Where the financial benefit (lump sum insured) does not allow for the reduction of the basic life insurance benefit, then the cover may not be a life insurance rider and may be liable at the insurance rate of duty applicable to that type of insurance.

The insured is paid $800,000, but the basic benefit still remains at $1,000,000

Additional cover 2

$200,000

The insured is paid $200,000 which reduces the policy to $800,000

Cover 1 is not a life insurance rider as the financial benefit is over and above the basic cover amount and will indicate that it is a stand-alone policy independent of the life insurance policy.

Cover 2 is a life insurance rider as the financial benefit reduces the basic cover benefit.

The insured is paid $1,000,000 which terminates the policy

Additional cover 2

$1,000,000

The insured is paid $1,000,000 which terminates the policy

Additional cover 1 & 2 are life insurance riders.

Life Insurance and Superannuation

The superannuation rules do not allow superannuation funds to own insurance policies which provide total and permanent disability cover where the cover provides benefits when the individual member is not able to work in the occupation they performed prior to the claimable event. They are restricted to owning a policy which covers the individual member only where they are unable to work in any occupation for which they are reasonably qualified by education, training or experience. Further, the superannuation law does not allow superannuation funds to take out critical illness insurance with respect to their members.

In response to these superannuation law restrictions, life insurance companies offer a product which allows individuals to purchase these additional types of cover outside of a superannuation fund and link that insurance to life insurance held for them through a superannuation fund.

In these instances, there will be two different policy holders for each cover. The trustee of the superfund and the person who is insured. If the riders to each policy or the insurance provided by each policy, would otherwise adhere to the 3 conditions as defined in section 241 of the Act, if they were part of the one policy, the linked policy or policies are classified as riders for the purposes of the Act.

Life insurance with the following benefits is obtained by 2 policyholders:

Life cover under a life policy issued to a superannuation trustee

TPD cover 1 linked to life cover under the life policy issued to superannuation trustee

TPD cover 2 outside super under a policy issued to the life insured (or other interested party); TPD cover 2 is linked to the life cover issued to the superannuation trustee

If the life insured passes away or either policy lapses, the other policy will also cancel/lapse.

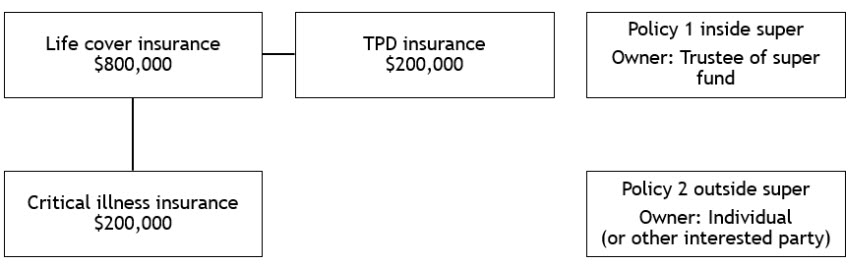

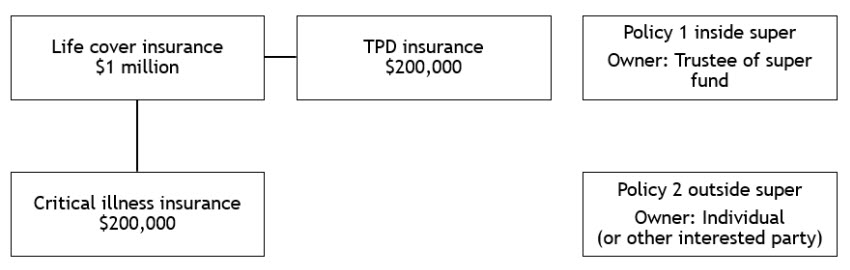

Life insurance with the following benefits is obtained by 2 policyholders:

Life cover under policy 1 issued to a superannuation trustee (with TPD cover linked to the life cover)

Trauma cover outside super (for example, Critical Illness insurance under a policy 2 issued to the life insured (or other interested party) If the life insured passes away or either policy lapses, the other policy will also cancel/lapse.

The TPD cover and the Critical Illness cover are life riders.

Connected benefits inside/outside super

Connected insurance with TPD and critical illness extensions before claim

Connected insurance with TPD and critical illness extensions after claim