Aim

The purpose of this CPN is to explain the application of the relevant contracts provisions under s32 of the Payroll Tax Act 2007 (the Act) to businesses providing:

- financial services under an Australian Financial Services (AFS) Licence issued under the Corporations Act 2001 (Cth); and

- credit services under an Australian Credit (AC) Licence issued under the National Consumer Credit Protection Act 2009 (Cth).

Payments of commission or other forms of remuneration by entities that hold an AFS licence or an AC licence (ie. payments by Licensees including Aggregators) to their authorised Agents may be liable for payroll tax if the contract between the Licensee and the Agent is a relevant contract.

Note: Failure to pay tax on remuneration, including commissions, paid or payable by Licensees to their Agents, may result in a tax default which incurs interest and penalty tax under the Taxation Administration Act 1996 (“TAA”).

Summary

- The relevant contracts provisions of the Payroll Tax Act may apply to contracts between:

- An Australian Financial Services Licensee and its Agents (called Authorised Representatives); and

- An Australian Credit Licensee (including an “Aggregator”) and its Agents (called Authorised or Sub-authorised Credit Representative).

- If a relevant contract exists:

- the Licensee or Aggregator is taken to be an employer;

- the Agent is taken to be an employee; and

- remuneration, commonly commission payments, including trail commissions are taken to be wages.

- A Licensee may be liable for payroll tax on remuneration unless an exemption applies.

- There are seven exemptions under the relevant contracts provisions, but the following 3 exemptions are the most likely to apply in this industry:

- services are provided by the Agent on no more than 90 days in the financial year;

- two or more persons to perform the work required under the contract in the financial year, and each worker performs work that is not de minimis; or

- the Chief Commissioner is satisfied that the Agent ordinarily performs services of that kind to the public generally (ie for other unrelated licensees) in the financial year.

- Commissions payable by a Licensee to another Licensee or Aggregator are exempt if the work is performed by two or more Agents engaged by the Licensee or Aggregator.

- Evidence that the Chief Commissioner may seek when conducting an audit or when considering applications for exemptions or rulings is outlined in this CPN.

Background

This Practice Note should be read together with Commissioner’s Practice Note CPN 007, which explains the general application of the relevant contracts provisions to independent contractors.

Contracts between persons who provide financial services which are subject to regulation by the Corporations Act 2001 (Cth) or the National Consumer Credit Protection Act 2009 (Cth) may be subject to payroll tax under the relevant contracts provisions in Division 7 of Part 3 of the Payroll Tax Act 2007 (“the Act”) unless an exemption applies.

Note: Persons who conduct financial services may incur a payroll tax liability under the relevant contracts provisions, whether or not they hold a licence or an authorisation to act as an agent of a licensee.

Australian Financial Services (AFS) Licences

(see Corporations Act 2001 (Cth) Part 7.6)

Under the Corporations Act 2001 (Cth) a person who carries on a business of providing financial services is required to hold an AFS Licence issued under that Act.

A Licensee may appoint Authorised Representatives (ARs) as its Agent to provide financial services on its behalf (see Part 7.6, including Division 5). A body corporate may sub-authorise a natural person as an AR, with the consent of the Licensee.

An AR may be appointed by more than 1 licensee. However Licensees are reluctant to agree to this practice because they are responsible to clients for loss or damage caused by the conduct of their Agents. If a person is appointed as an AR by multiple AFS Licensees, those licensees are jointly and severally liable for the conduct of the AR.

Licensees must notify ASIC within 15 days of the appointment of an AR.

Australian Credit (AC) Licences

(see National Consumer Credit Protection Act 2009 (Cth) Part 2.2)

Under the National Consumer Credit Protection (NCCP) Act 2009 (Cth) a person who carries on a business which engages in credit activities is required to obtain an Australian Credit (AC) Licence issued under that Act. However, this does not apply to employees and directors of licensees or related bodies corporate of licensees, or to credit representatives of licensees.

A Licensee may appoint an Authorised Credit Representative (ACR) or a Sub-Authorised Credit Representative (SCR) to carry on credit activities on behalf of the Licensee. ACRs and SCRs are commonly called mortgage brokers. An ACR and an SCR can be appointed as the credit representative of two or more licensees if:

- each licensee has consented to the person also being the credit representative of each of the other licensees; or

- each licensee is a related body corporate of each of the other licensees (without the need for approval of each of the licensees).

A Licensee may also appoint other licensees as agents (often referred to as “aggregators”) who may also engage ACRs and SCRs as their Agents to provide credit services on their behalf to clients. In some cases, ACRs who appoint multiple SCRs may be Aggregators.

Licensees must notify ASIC within 15 days of appointing an ACR or SCR as a credit representative.

Remuneration of Licensees and Agents

Remuneration paid or payable by Licensees and Agents generally takes the form of:

- up-front commissions which are paid or payable when an Agent arranges a sale of a financial product or when a customer introduced by an agent enters into a contract with a Licensee; and

- “trail” commissions, which are usually paid or payable on each anniversary of a sale of a financial product or successful introduction of a customer, for as long as the contract remains in place.

Note: Provisions contained in Division 7.7A of the Corporations Act 2000 (Cth), prohibit an authorised representative, including a Licensee acting in the capacity of an AR of another Licensee, from accepting conflicted remuneration, and exposes the AR to civil penalties for contravention.

A payment of conflicted remuneration may never-the-less constitute “wages” under s.35 of the Act. However, the Chief Commissioner may report any payments of conflicted remuneration to the Australian Securities and Investment Commission under s.82 (f) of the Taxation Administration Act 1996.

Commissioner’s Practice Note

1. Application of relevant contracts provisions

a) Deemed employers under s.33

Under s.33(1) of the Payroll Tax Act 2007 (“the Act”), a person who supplies services (s.33(1)(a)) or is supplied with services (s.33(1)(b)) under a relevant contract is taken to be an employer (ie a “deemed employer”).

An AFS Licensee or an AC Licensee (including an Aggregator) who is supplied with services, and also supplies services under a contract with an agent is therefore taken to be an employer. The agent may be another Licensee (including an Aggregator), or an AR, ACR or SCR.

b) Deemed employees under s.34

The person who performs the work under a relevant contract is taken to be an employee (ie a “deemed employee”). An AR, an ACR or an SCR (ie an “agent”) who supplies services to a licensee or aggregator may be a deemed employee under s.34(a).

A licensee or aggregator who performs work for another Licensee or Aggregator or for an AR, an ACR or an SCR under a relevant contract, is also a deemed employee under s.34(a).

c) “Wages” paid or payable under s.35

Amounts paid or payable under a relevant contract are taken to be wages under s.35. The payment need only be “for or in relation to the performance of work relating to a relevant contract” to be deemed wages. This means all amounts payable under the contract are deemed to be wages, even if they are attributed to non-labour costs.

d) Return of deemed wages in payroll tax returns

If a payment is deemed wages under s.35 of the Act, the payroll tax liability of the deemed employer arises when the commission is paid or when it becomes payable, whichever occurs first.

e) Exemptions

If an exemption applies under the relevant contracts provisions, no payroll tax liability arises. There are 7 available exemptions, and these are explained in CPN 007 (add link). The three exemptions which are commonly applicable in the financial services sector are explained with examples in Part 6 below.

f) Conflicted remuneration may be “wages”

Provisions contained in Division 7.7A of the Corporations Act 2000 (Cth), prohibit an authorised representative, including a Licensee acting in the capacity of an AR of another Licensee, from accepting conflicted remuneration, and exposes the AR to civil penalties for contravention.

A payment of conflicted remuneration may never-the-less constitute “wages” under s.35 of the Act. However, the Chief Commissioner may report any payments of conflicted remuneration to the Australian Securities and Investment Commission under s.82 (f) of the Taxation Administration Act 1996.

2. Common misconceptions which result in tax defaults

The following reasons are often given by Licensees, Aggregators and Agents to explain why they believe the relevant contracts provisions do not apply to their particular circumstances:

- the Agent does not provide any services to the Licensee who engages the agent, but instead provides services to its clients;

- the Agent services its own clients and can take those clients with them if they cease to be an agent for the Licensee;

- the Agent sources its own clients and the licensee does not provide “leads” or refer any clients to the Agent;

- the Licensee simply provides the regulatory framework required under the Corporations Act that allows the Agent to operate its own business;

- the relationship between Licensee and Agent is, in effect, a franchise arrangement rather than a provision of services by the agent to the licensee;

- payments made by the Licensee to the Agent is a return of the Agents money earned by the Agent for the provision of financial advice to its clients;

- the Agent does not operate from the Licensee’s premises;

- the commercial relationship between a Licensee and an Agent does not fit within the definitions in the contractor provisions;

- the Future of Financial Advice (“FoFA”) amendments to the Corporations Act 2001 (Cth) mean that the relevant contracts provisions do not apply to the financial planning industry.

a) General comments on misconceptions

These arguments are not accepted by the Chief Commissioner as reasons why the relevant contracts provisions don’t apply. An Agent is engaged to provide services for or on behalf of a Licensee under an arrangement that meets the definition of a “relevant contract” under the Act. The Commonwealth legislation [1] prohibits an Agent from providing relevant services to a client unless it is authorised as an agent or sub-agent by a licensee. However, a contract may be a relevant contract even if a party to the contract does not hold a licence or is not authorised by a licensee as required by Commonwealth legislation.

Even though an Agent may source their own clients, the clients are also clients of the Licensee, and in providing services to clients of a licensee, the agent may (also) supply services for or in relation to the performance of work to the Licensee under a “relevant contract”; (see Bridges Financial Services Pty Ltd v Chief Commissioner of State Revenue [2005] NSWSC 788, at [225]; Re D & D Tolhurst Pty Ltd and Cmr of State Revenue (Vic) 1997 ATC 2179 at [18]); Novus Capital Ltd v Chief Commissioner of State Revenue [2018] NSWCATAD 72 at [74] to [78]).

It does not matter that a licensee also provides services to its agents under a relevant contract. It is a general feature of most, if not all relevant contracts that services are provided by both parties to or on behalf of each other. Nor does it matter that the quantity or value of the services performed by an agent who is taken to be an employee exceeds the quantity or value of services performed by the Licensee who is taken to be an employer.

b) Impact of FoFA amendments

The FOFA were introduced into the Corporations Act 2001 by the Corporations Amendment (Future of Financial Advice) Act 2012 (Cth) and the Corporations Amendment (Further Future of Financial Advice Measures) Act 2012 (Cth). These reforms included the best interests duty, a ban on conflicted forms of remuneration, the opt-in obligation and changes to ASIC’s licensing and banning powers.

However these amendments did not affect the application of the Payroll Tax Act, including the requirements to pay payroll tax if the relevant contracts provisions apply to a contract between a licensee and an authorised representative[2].

c) Impact of s.769B(7) of the Corporations Act

S.769B(7) of the Corporations Act limits the liability of a licensee for a breach of provisions in Part 7.7 (Financial services disclosure) and Part 7.7A (Best interests obligations and remuneration) of the Corporations Act.

However, this does not mean an AR does not perform work or provide services under a contract with a Licensee. It makes it clear that a licensee does not commit an offence merely because from a specified offence is committed by an agent of the licensee.

3. When commissions must be included in returns

A commission which is taxable wages must be included in the deemed employer’s payroll tax return for the month or financial year in which the commission is paid or when it becomes payable, whichever occurs first (see s.11(7) of the Act). If the months in which a trail commission becomes payable and is paid occur in different financial years, it must be returned in the earlier of the two financial years. Taxable wages must be included in either the relevant monthly return, or the relevant annual return if the deemed employer is an annual lodger.

A trail commission must be included in a deemed employer’s monthly or annual return for the financial year in which it is paid or becomes payable, whichever occurs first.

Note: Trail commissions are generally “paid or payable” on the anniversary of a contract.

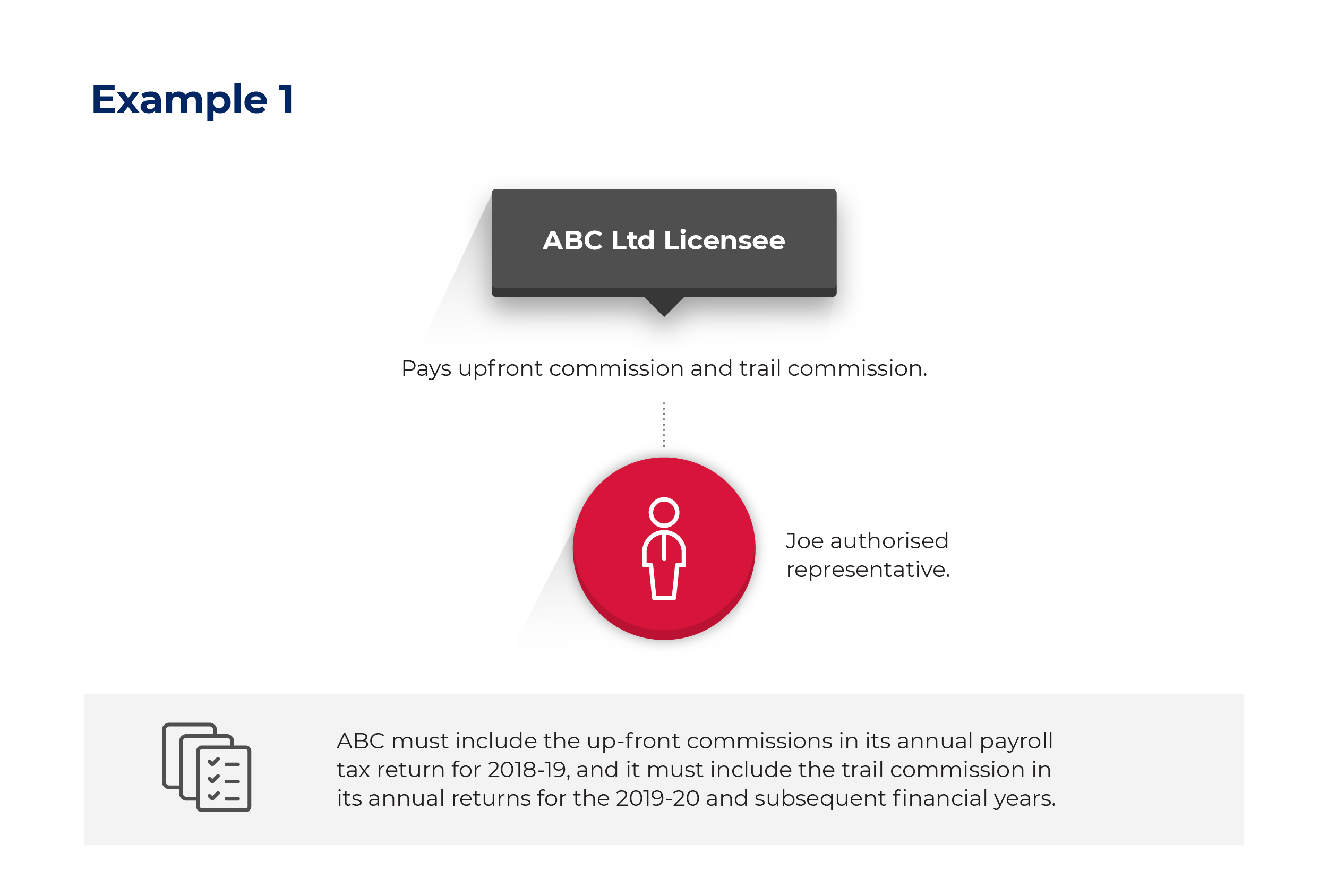

Example 1:

ABC Ltd is a Licensee and engages Joe as an AR for the 2018-19 financial year. Joe worked exclusively as an AR for ABC Ltd during the 2018-19 financial year, and none of the exemptions under the relevant contracts provisions applied for the 2018-19 financial year.

ABC Ltd pays up-front commissions to Joe during 2018-19 and also pays trail commissions in subsequent years on the anniversary of the contracts arranged by Joe, in accordance with the terms of the contracts.

ABC must include the up-front commissions in its annual payroll tax return for 2018-19, and it must include the trail commission in its annual returns for the 2019-20 and subsequent financial years.

Evidence

ABC Pty Ltd should maintain the following records as evidence, and may be asked to produce the records when an audit is conducted. Additional information may be sought to confirm the accuracy of records.

- Copy of contract between ABC Ltd and Joe.

- FY 2018-19 and FY 2019-20 General Ledger showing commission payments.

- Sample of invoices and/or payslips.

- Bank Statements.

- Workcover certificate of ABC Ltd to cover Joe if applicable.

A commission that is payable in a financial year following the year in which the services were performed by the Agent must be included in a return in the year in which the commission is paid or becomes due for payment, whichever occurs first.

4. Determining whether an exemption applies

The application of an exemption with both an up-front and a trail commission payment is determined having regard to the circumstances applying to the provision of the services in the year in which the services were provided, not the year in which the commission was paid or became payable.

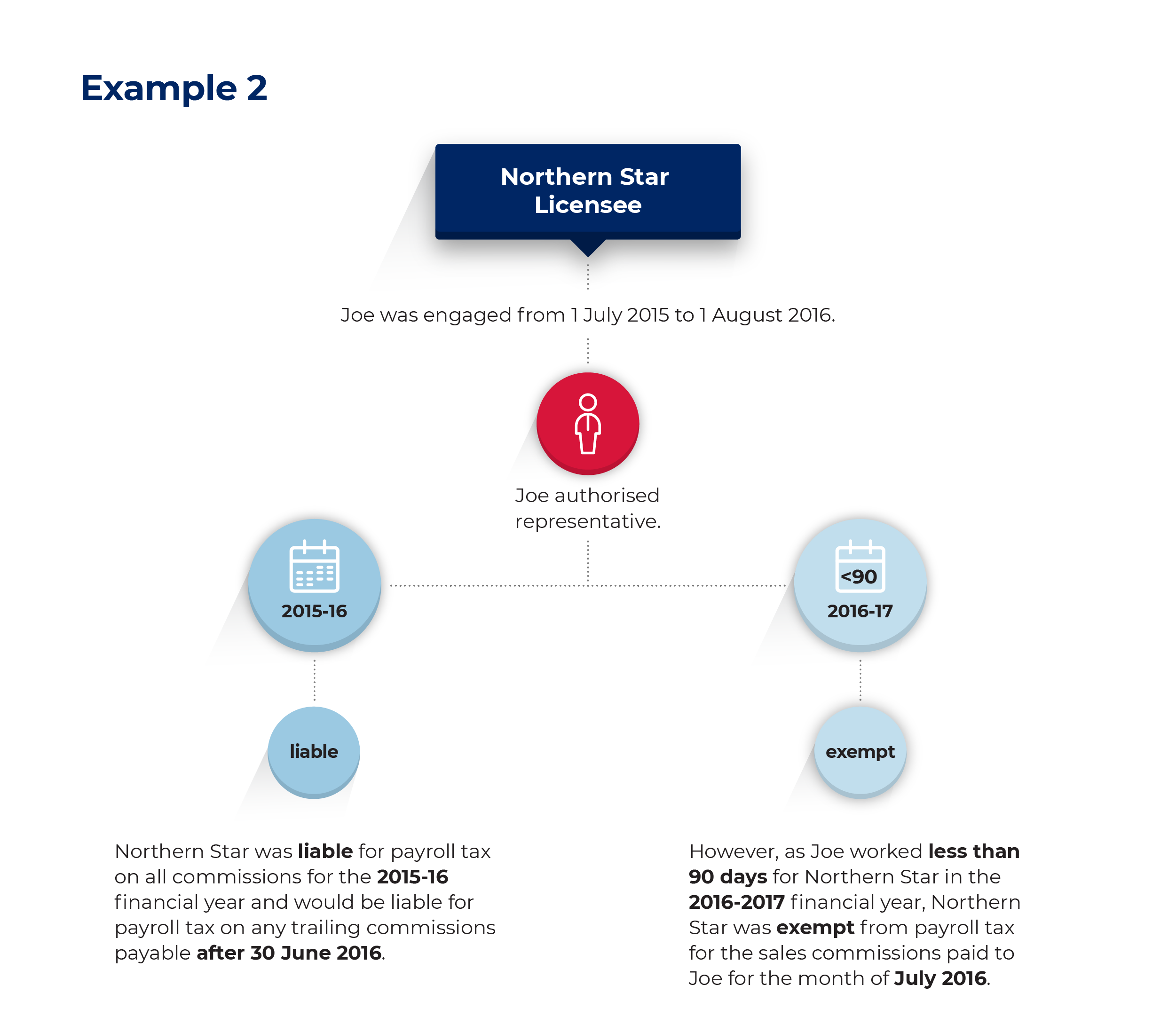

Example 2:

Joe is engaged as an Agent by Northern Star (a Licensee) from 1 July 2015 until 1 August 2016. Joe ends his relationship as an Agent of Northern Star on 1 August 2016 and shortly afterwards commences work as an Agent for another Licensee.

During the 2015-16 financial year none of the relevant contracts exemptions applied, and Northern Star was liable for payroll tax on all commissions payable to Joe during that financial year, including trail commissions payable after 30 June 2016.

For the month of July 2016, Northern Star was entitled to an exemption because it engaged Joe for no more than 90 days during the 2016-17 financial year. Trail commissions payable to Joe in subsequent years as a result of contracts executed in July 2016 are also exempt.

Evidence

Northern Star should maintain the following records as evidence and may be asked to produce the records when an audit is conducted. Additional information may be sought to confirm the accuracy of records.

- Copy of contract between Northern Star and Joe.

- Copy of general ledger entries for Joe’s commission for the period under review and records of corresponding contracts to which the commissions relate.

- Evidence of Joe’s Agency Contract termination to confirm effective date.

- Invoices and/or payslips to confirm the accuracy of the general ledger.

- Bank statements.

- Work schedules/logbooks to evidence days on which Joe worked.

- Workcover certificate of Northern Star to cover Joe if applicable.

5. Licensees engaging other Licensees/aggregators

Licensees under both Commonwealth Acts often appoint a second licensee/aggregator to market and sell their products. The second Licensee/Aggregator appoints its own Agents to sell the products of the first Licensee (and products of other Licensees).

A Licensee who appoints another Licensee/Aggregator will generally have no payroll tax liability on commissions, because the second Licensee/Aggregator engages multiple Agents, and the “two or more persons” exemption applies.

If a licensee engages a second Licensee/Aggregator, and pays an Agent of the second Licensee/Aggregator part of the commission, the second Licensee/Aggregator is liable for payroll tax under s.46(1) (Wages paid by or to third parties) unless an exemption applies to the contract between the second Licensee/Aggregator and the agent.

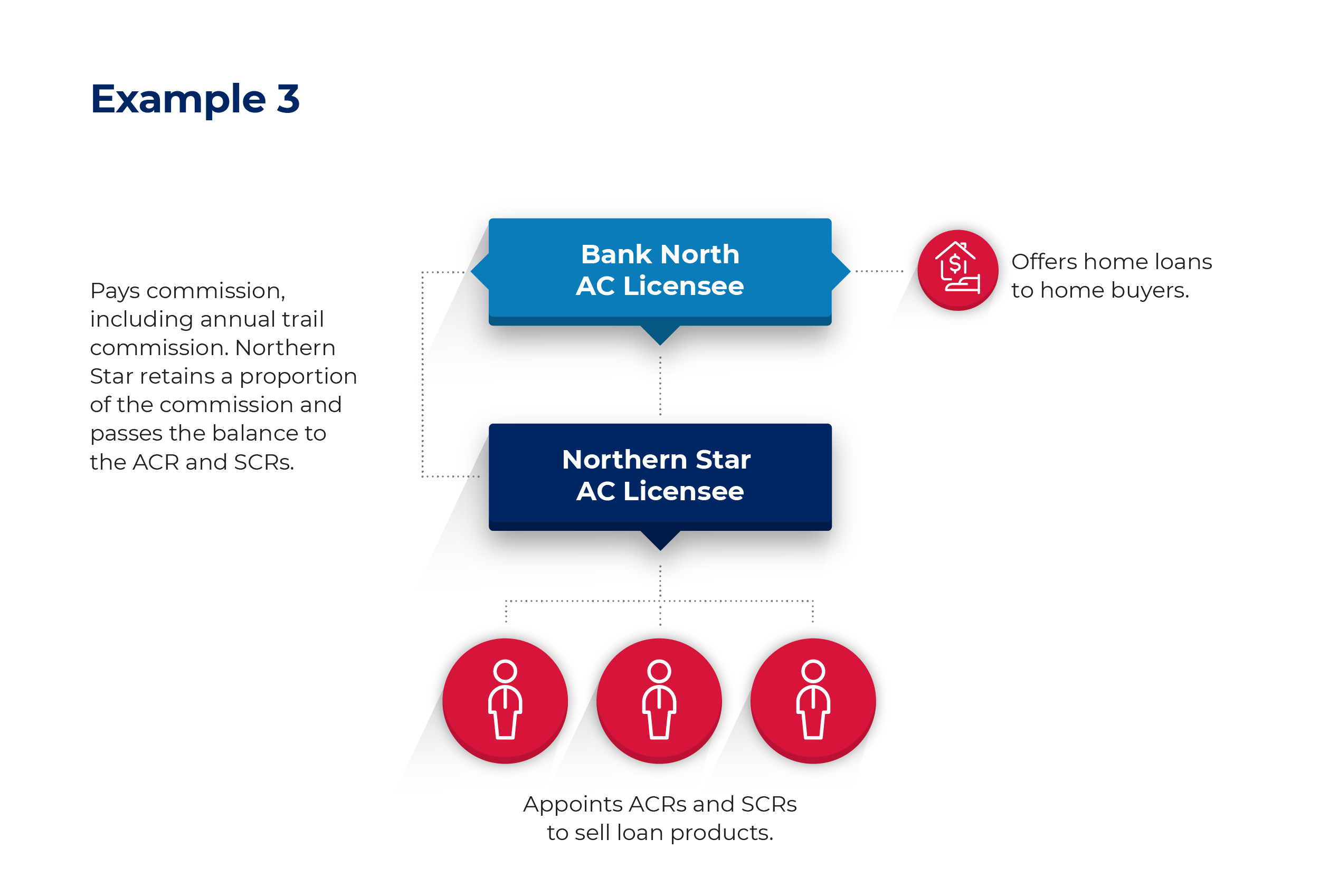

Example 3:

Bank North is an AC Licensee and offers home loans to home-buyers. Bank North enters into a contract with AC Licensee Northern Star, to market the loan products offered by Bank North.

Northern Star appoints several ACRs and SCRs to sell the loan products offered by Bank North. Bank North pays commissions to Northern Star, including annual trail commissions which are payable on the anniversary of a loan for the life of the loan. Northern Star retains a proportion of each commission, and passes on the balance of the commission to the ACR or SCR who arranged the loan.

Under this arrangement there are several possible relevant contracts. One is between Bank North and Northern Star in which Bank North is the deemed employer and Northern Star is the deemed employee.

Other relevant contracts may exist between Northern Star and the ACRs and SCRs that Northern Star engages to fulfil it’s obligation under its’ contract with Bank North. Under these contracts Northern Star is the deemed employer and the ACRs and SCRs are deemed employees

The contract between Bank North and Northern Star is exempt because the work is performed by 2 or more persons (ACRs) engaged by Norther Star to provide services to Bank North on behalf of Northern Star.

Northern Star may be liable for payroll tax on the amount of each commission that is paid or payable to an ACR or SCR, unless an exemption applies. Bank North is not liable for payroll tax in respect of this contract

Even if Bank North pays the Agents of Northern Star their respective shares of commissions, Northern Star may be liable for payroll tax under s.46 of the Act (“Wages paid by third parties”).

Evidence

Northern Star and Bank North should maintain the following records as evidence, and may be asked to produce the records when an audit is conducted. Additional information may be sought to confirm the accuracy of records.

- List of Northern Star ACRs/SCRs who sold Bank North’s loan products during review period.

- Copy of Contracts between Northern Star and Bank North, and between Northern Star and its ACR.

- Copies of general ledger entries for ACR/SCR’s commission paid by Bank North and Northern Star.

- Sample of invoices to enable accuracy of General Ledger to be checked.

- Role descriptions of the ACRs and SCRs if applicable.

- Workcover certificate of Northern Star to cover its ACRs and SCRs if applicable.

- Payment records for payments from Northern Star to its ACRs and SCRs such as invoices, payslips, ledgers etc.

- Schedules of working days/hours for ACRs and SCRs.

6. Exemptions

A contract is exempt from payroll tax if 1 of the exemptions in s.32 of the Act apply. There are seven exemptions which are explained in CPN 007.

In the financial services industry, there are 3 exemptions which are more commonly applicable, and these are explained below.

i. Exemption if services are performed by two or more persons

Where a Licensee engages an Agent to provide services, and the Agent engages another person to assist them in performing their duties, then the above exemption may apply.

Note: The second person that provides services to or for the agent may be a company.

The 2nd person must be engaged by, or perform work for the Agent in the course of the agent’s business. The work performed by the second person must be directly related to the work required to be performed under the contract between the Licensee and the Agent. This includes administrative work directly related to the services required under the contract.[3]

However, the Chief Commissioner may not be satisfied that the exemption applies in the following circumstances:

- the second person is engaged by the Licensee, not by the AR;[4]

- the second person provides general business-related services that are not required to be provided to the Licensee under the relevant contract, eg tax, accounting and business advisory services provided to the AR, not to the Licensee.[5]

The work performed by the second person must not be de minimis. The amount of work performed is de minimis if it is an insignificant proportion of the total work performed under the contract during the financial year (see Zuccula Homes[6]).

The exemption may apply where an Agent engages another agent to perform work under a fee-splitting arrangement; (see for example, Novus Capital Ltd v Chief Commissioner of State Revenue [2018] NSWCATAD 72 at [231] – [232], [364] – [367] and [458] – [472]).

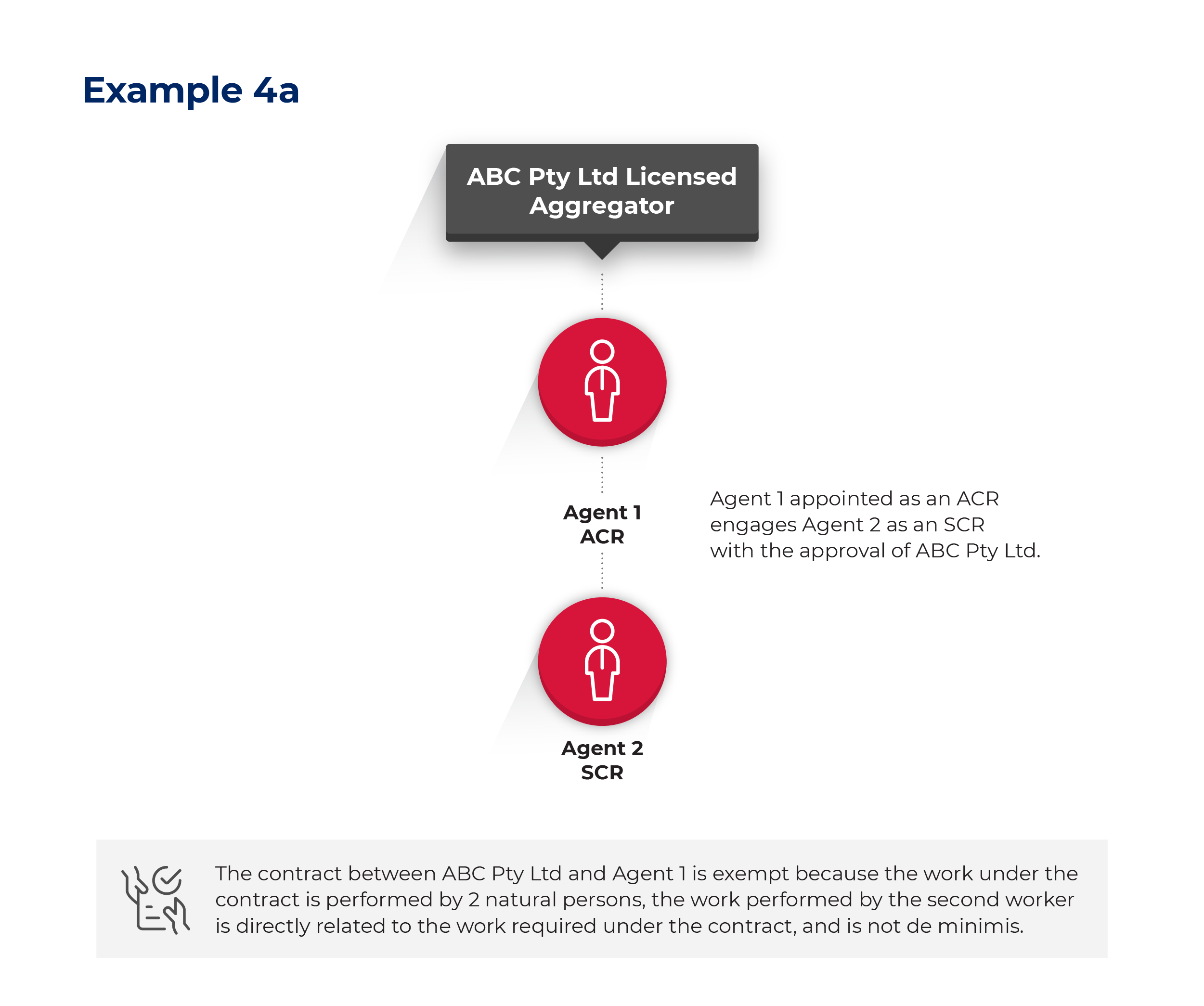

Example 4:

ABC Pty Ltd is a Licensed Aggregator and engages ACRs and SCRs to market the mortgage products of several financial institutions.

ABC Pty Ltd appoints Agent 1 as an ACR, who engages Agent 2 as an SCR with the approval of ABC Pty Ltd. Agent 1 and Agent 2 work together to engage with potential borrowers, prepare and submit loan applications to financial institutions on behalf of ABC Pty Ltd. Agent 1 and Agent 2 reach agreement between themselves regarding allocation and performance of work and splitting of fees and commissions.

The contract between ABC Pty Ltd and Agent 1 is exempt because the work under the contract is performed by two natural persons, the work performed by the second worker is directly related to the work required under the contract, and is not de minimis.

Evidence

ABC Pty Ltd should maintain the following records as evidence, and may be asked to produce the records when an audit is conducted. Additional information may be sought to confirm the accuracy of records.

- Copy of contract between ABC Pty Ltd and Agent 1.

- Approval letter/correspondence between Agent 1 and ABC Pty Ltd to confirm approval of the engagement of Agent 2.

- Copy of agreement between Agent 1 and Agent 2 to understand terms of agreement and scope of work including details of commission sharing.

- Copy of general ledger entries for distribution of commission between Agent 1 and Agent 2 for the period under review.

- Other payment records such as invoices, bank statements, payslips and ledgers.

Schedules of working days/hours for ACRs and SCRs (if any).

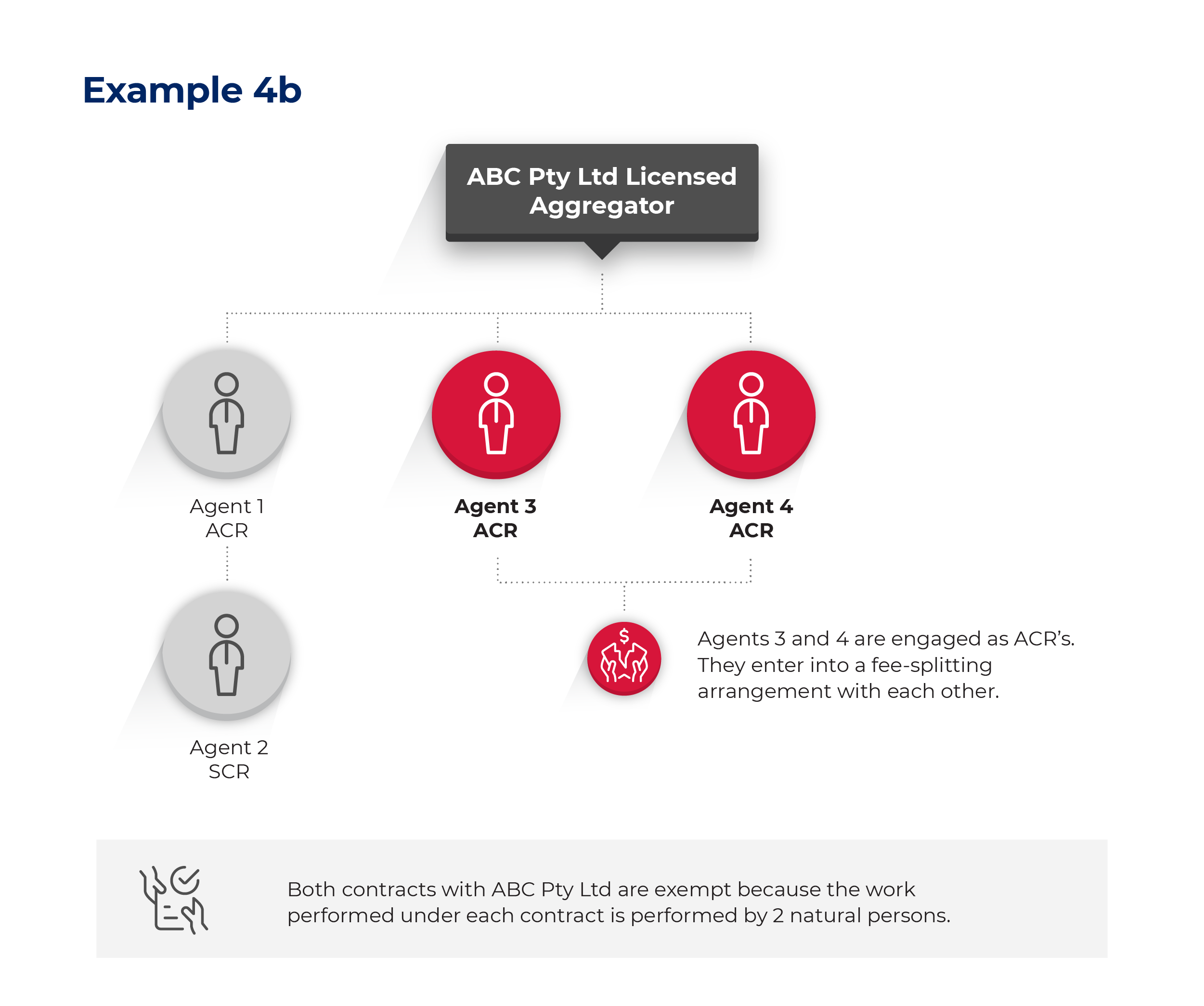

Agent 3 and Agent 4 are engaged by ABC Pty Ltd as ACR’s. Agents 3 and 4 enter into an agreement to refer some of their work for their respective clients to each other because they each have different specialist skills. They agree to a fee-splitting arrangement when they perform work for each other’s clients.

Both contracts with ABC Pty Ltd are exempt because the work performed under each contract is performed by two persons.

Evidence

ABC Pty Ltd should maintain the following records as evidence, and may be asked to produce the records when an audit is conducted. Additional information may be sought to confirm the accuracy of records.

- Copy of Agency Contracts between ABC Pty Ltd and Agents 3 and 4 to understand terms of agreement including percentages in commission.

- Copy of contract between Agent 3 and Agent 4 including the agreement to split commissions.

- Copy of ABC Pty Ltd’s general ledger entries for commission payments to Agent 3 and Agent 4 for the period under review.

- Copy of general ledger or bank statements evidencing the payments between agents, or advice to the Licensee regarding splitting of commissions.

However, exemption does not apply if an agent merely refers a client to another Agent.

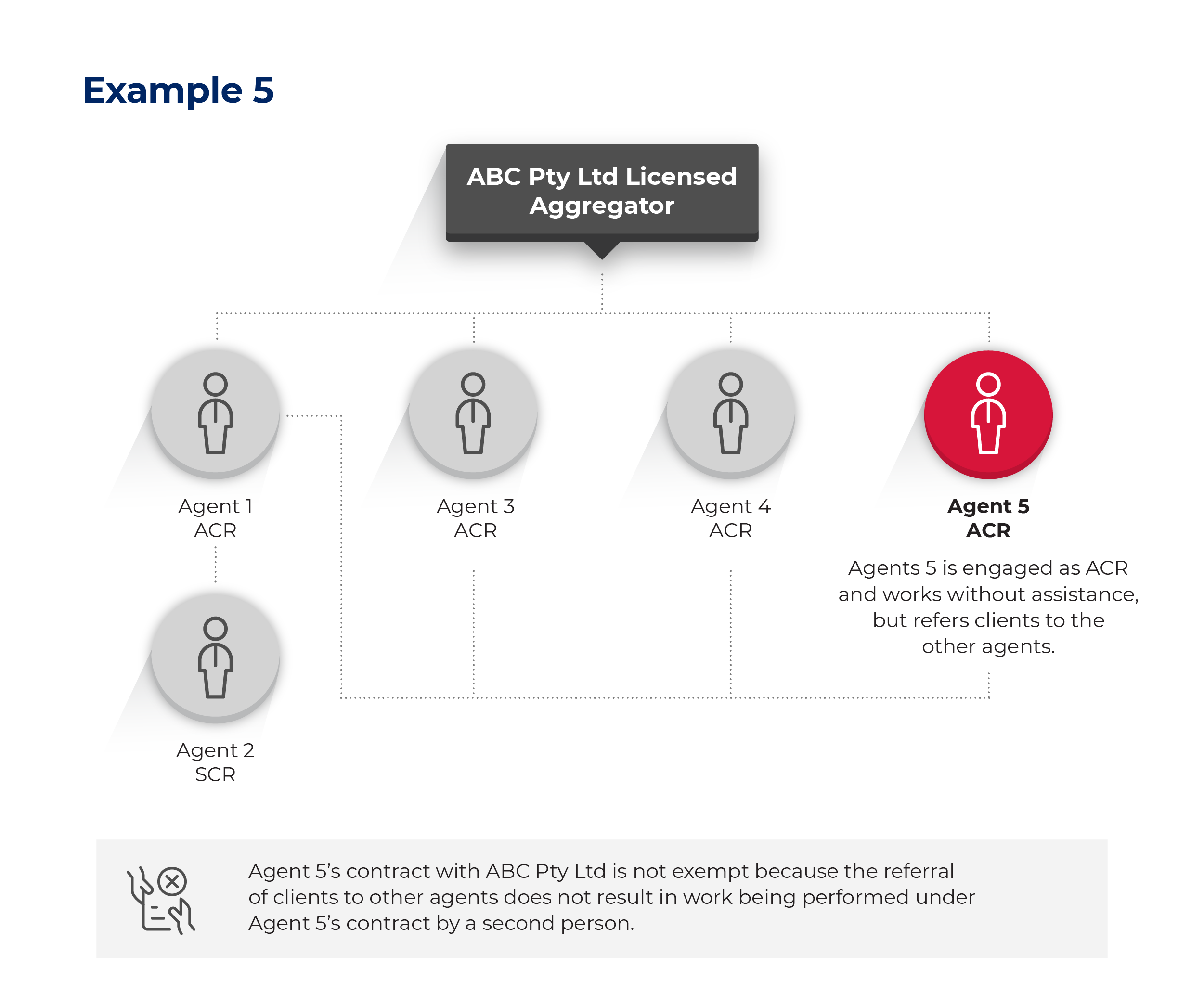

Example 5:

Agent 5 is engaged by ABC Pty Ltd as an ACR and works without assistance from other agents. If unable to meet a client’s needs, whether due to the special needs of the client or a heavy workload servicing existing clients, Agent 5 refers clients to other agents and does not receive a share of any commissions payable by ABC Pty Ltd to other agents .

Agent 5’s contract with ABC Pty Ltd is not exempt because the referral of clients to other agents does not result in work under Agent 5’s contract with ABC Pty Ltd being performed by two or more persons.

The work performed by the second person must be directly related to the work required to be performed under the contract.

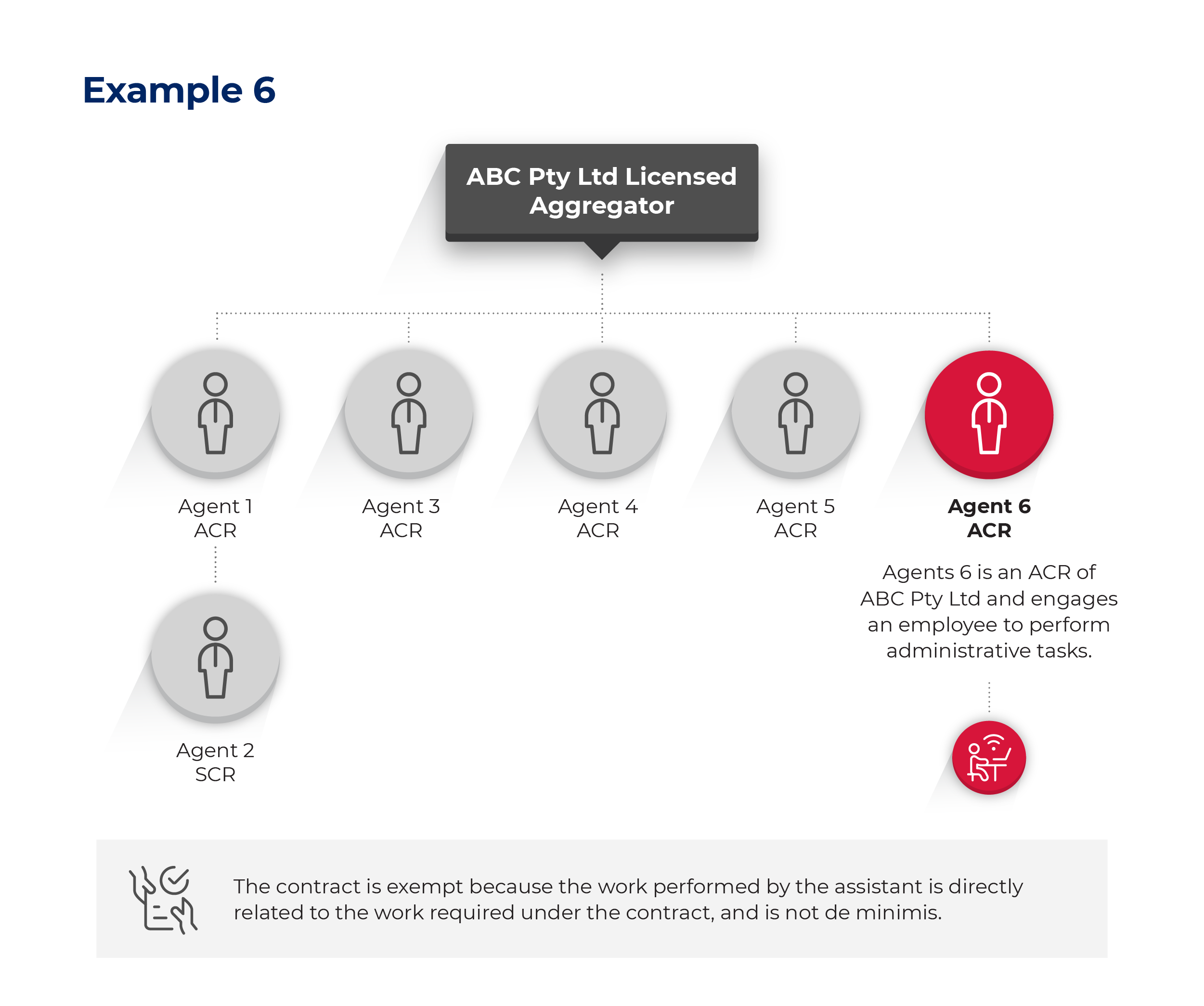

Example 6:

Agent 6 is an ACR of ABC Pty Ltd and engages an employee to deal with initial inquiries from clients, complete loan application forms, prepare and issue correspondence, maintain files and other records, financial management, liaise with web developers, general marketing and advertising activities.

The contract is exempt because the work performed by the assistant is directly related to the work required under the contract between the agent and the Licensee, and the relevant work is not de minimis.

Evidence

ABC Pty Ltd should maintain the following records as evidence, and may be asked to produce the records when an audit is conducted. Additional information may be sought to confirm the accuracy of records.

- Agency Contract copy with ABC Pty Ltd and Agent 6 to understand terms of agreement including payment of commissions.

- General Ledger copy for commission distributed to Agent 6 during the review period.

- Payroll and PAYG records.

- Copy of employee’s role description.

- Workcover certificate.

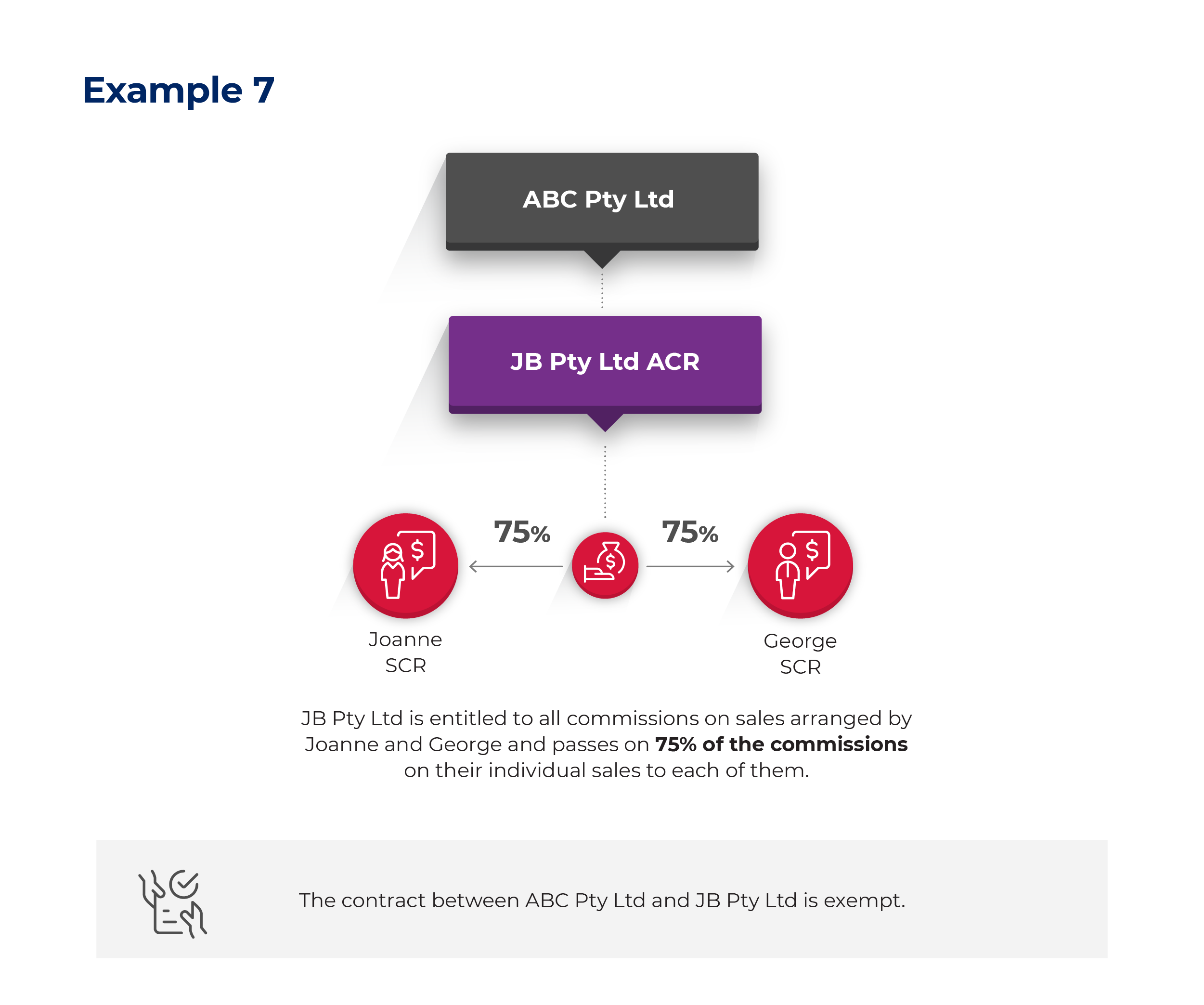

Example 7:

ABC Pty Ltd appoints JB Pty Ltd as an ACR.Joanne and George are engaged by JB Pty Ltd as SCR’s with the approval of ABC Pty Ltd. JB Pty Ltd is entitled to all commissions on contracts with customers introduced by Joanne and George and passes on 75 per cent of the commissions attributed to each of them.

The contract between ABC Pty Ltd and JB Pty Ltd is exempt because the services required to be performed by JB Pty Ltd under the contract are performed by two persons.

Evidence

ABC Pty Ltd should maintain the following records as evidence, and may be asked to produce the records when an audit is conducted:

- Copy of Agency Contract between ABC Pty Ltd and JB Pty Ltd to understand terms of agreement including payment of commissions.

- Copy of JB Pty Ltd’s contracts with Joanne and George to understand terms of agreement including payment of commissions.

- Approval letter/correspondence between ABC Pty Ltd and JB Pty Ltd regarding engagement of Joanne and George.

- Copy of general ledger entries for commission payments to Joanne and George.

The exemption does not apply if the second person who performs work required under a contract between a Licensee and an Agent is performed by a person engaged by the Licensee[7].

Example 8:

Broker Pty Ltd is a Licensee and requires its Agents to use an electronic service provided by Electronic Systems Pty Ltd for all communications between the Licensee, agents and clients, including transfer of copies of documents and lodgement of applications.

The arrangement does not satisfy the two-person exemption because the services of Electronic Systems Pty ltd were engaged by the licensee, not by the agents.

ii. Exemption if agent performs work for no more than 90 days

If an agent performs work under a contract for no more than 90 days during a financial year, the contract is exempt for that financial year. Each day on which the agent performs work counts as 1 day, regardless of how much time is spent working on a particular day; see Revenue Ruling PTA 014 - What Constitutes a Day's Work?

If an agent is appointed by a Licensee and the appointment extends over a period that exceeds 90 days in a particular financial year, the contract is not exempt unless the Licensee provides probative evidence which proves on the balance of probabilities that the agent provided services to the licensee’s clients on no more than 90 days during the financial year. Unsubstantiated submissions to that effect are not sufficient.[8]

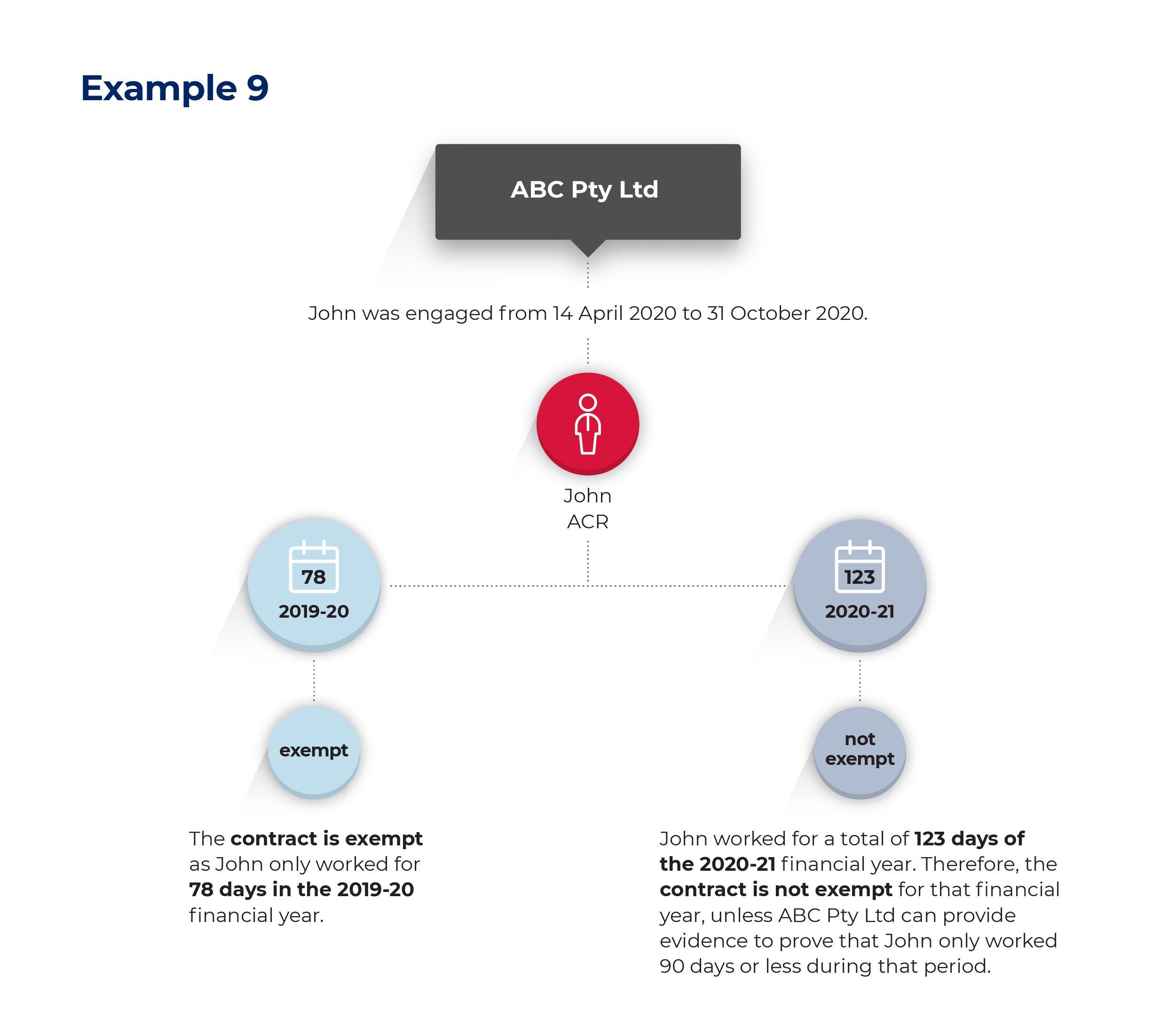

Example 9:

John is appointed as an ACR by ABC Pty Ltd from 14 April 2020 until 31 October 2020. This equates to 78 days in 2019-20, and 123 days in 2020-21.

As John could not have worked on more than 90 days in the 2019-20 financial year, the contract is exempt for that financial year.

John was appointed for a total of 123 days of the 2020-21 financial year. Therefore, the contract is not exempt for that financial year, unless ABC Pty Ltd can provide probative evidence to prove on the balance of probabilities that John worked on no more than 90 days during that period.

Evidence

ABC Pty Ltd should maintain the following records as evidence, and may be asked to produce the records when an audit is conducted. Additional information may be sought to confirm the accuracy of records.

- Copy of contract between ABC Pty Ltd and John.

- Records showing days on which work was performed by John.

- Invoices issued by John to ABC Pty Ltd.

ABC Pty Ltd’s general ledger and supporting financial records for commission payments.

iii. Exemption if Agent provides services to the public generally

A contract between a licensee and an Agent is exempt if the agent provides services of the same kind to the public generally during a financial year. The Agent must provide similar services during the financial to two or more Licensees who are not grouped for payroll tax purposes under Part 5 of the Act (“Grouping of employers). The work performed by the agent for each licensee must be significant and not de minimis. The Licensee must be able to produce evidence that the agent is an authorised agent of each of the licensees.

However, a contract with an agent is not exempt if the Agent provides services to two or more Licensees who are member of the same group, because the Agent is not considered to be providing services to the public generally.

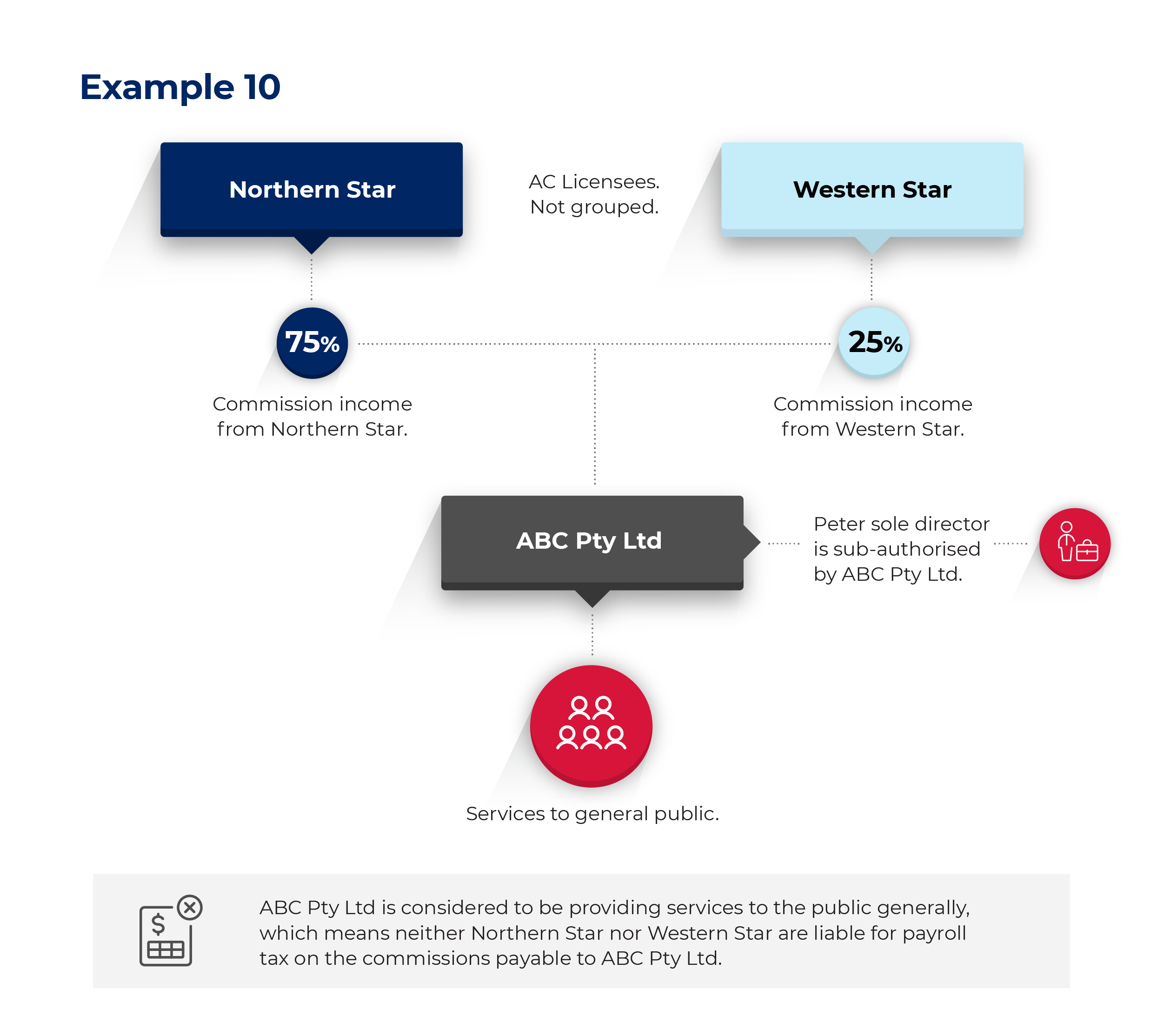

Example 10:

ABC Pty Ltd is an ACR for two AC Licensees (Aggregators), Northern Star and Western Star. Northern Star and Western Star are not grouped for payroll tax purposes.

ABC Pty Ltd has sub-authorised its sole director Peter, with approval of both Northern Star and Western Star.

ABC Pty Ltd generates 75 per ccent of its commission income from Northern Star and 25 per cent from Western Star.

ABC Pty Ltd is considered by the Chief Commissioner to be providing services to the public generally, which means neither Northern Star nor Western Star are liable for payroll tax on the commissions payable to ABC Pty Ltd.

Evidence

ABC Pty Ltd should maintain the following records as evidence, and may be asked to produce the records when an audit is conducted. Additional information may be sought to confirm the accuracy of records.

- Copy of Agency Contracts between ABC Pty Ltd and Northern Star.

- Copy of contract between ABC Pty Ltd and Western Star.

- Copy of General Ledger entries for successful contracts, or audited financial statement showing commissions paid by ABC Pty Ltd to both Northern Star and Western Star.

- Copy of Sales Ledger and Bank Statement of ABC Pty Ltd showing income source.

- Invoices between ABC Pty Ltd and Northern Star.

- Invoices between ABC Pty Ltd and Western Star.

7. Records must be kept for at least five years

Licensees and agents must keep records which enable their tax

liability under the payroll Tax Act to be properly assessed, and must keep the records for a minimum of five years after the end of the financial year in which commissions that were or may be liable to payroll tax were paid or became payable (see Part 8 of the Taxation Administration Act 1996).

An employer who disputes the correctness of a payroll tax assessment in an objection to the Chief Commissioner or in a request for review by the NSW Civil and Administrative Tribunal or a Court bears the onus of proving the assessment was incorrect (see ss.88 and 100(3) of the Taxation Administration Act 1996).

Footnotes

- ^ Part 7.6 Corporations Act 2000 (Cth); Chapter 2 National Consumer Credit Protection Act 2009(Cth).

- ^ See Novus Capital Ltd v Chief Commissioner of State Revenue [2018] NSWCATAD 72 at [74] to [78].

- ^ See Bridges Financial Services Pty Ltd v Chief Commissioner of State Revenue [2005] NSWSC 788 at [234]

- ^ See Novus Capital Ltd v Chief Commissioner of State Revenue [2018] NSWCATAD 72 at [208].

- ^ See Novus Capital Ltd v Chief Commissioner of State Revenue [2018] NSWCATAD 72 at [241(4)].

- ^ Zuccala Homes Pty Ltd v Commissioner of State Revenue Victoria (1994) ATC 2087.

- ^ Novus Capital Ltd v Chief Commissioner of State Revenue [2018] NSWCATAD 72 at [208].

- ^ Novus Capital Ltd v Chief Commissioner of State Revenue [2018] NSWCATAD 72 at [87] & [106].