- This Ruling explains the land tax liability of owners of land subject to a life interest. It explains the liability of the person who has the life interest, and of the persons who have an interest in the remainder or on reversion when the life interest expires. It also explains the different outcomes resulting when an interest in the land is held by a company, a fixed trust or a special trust, and application of an exemption when the land is used and occupied as a principal place of residence.

Note: Failure to lodge a return and pay land tax in respect of taxable land is a tax default which may result in interest and penalty tax being applied under the Land Tax Management Act 1956 (“LTMA”) and the Taxation Administration Act 1996 (“TAA”).

Background

- The LTMA together with the TAA provides that land tax is payable by all owners of land in NSW unless an exemption applies. An “owner” of land is defined in s. 3(1) of the LTMA and includes the owner of the freehold in possession.

- S.20 of the LTMA deals with the land tax liability of a person who has a freehold estate in land less than the fee-simple (that is, a limited estate). A limited estate includes a life estate, and an interest in reversion or remainder.

- This ruling explains the land tax liability of persons who have a limited estate in land consisting of a life estate, or an interest in reversion or remainder.

Ruling

What is a life estate?

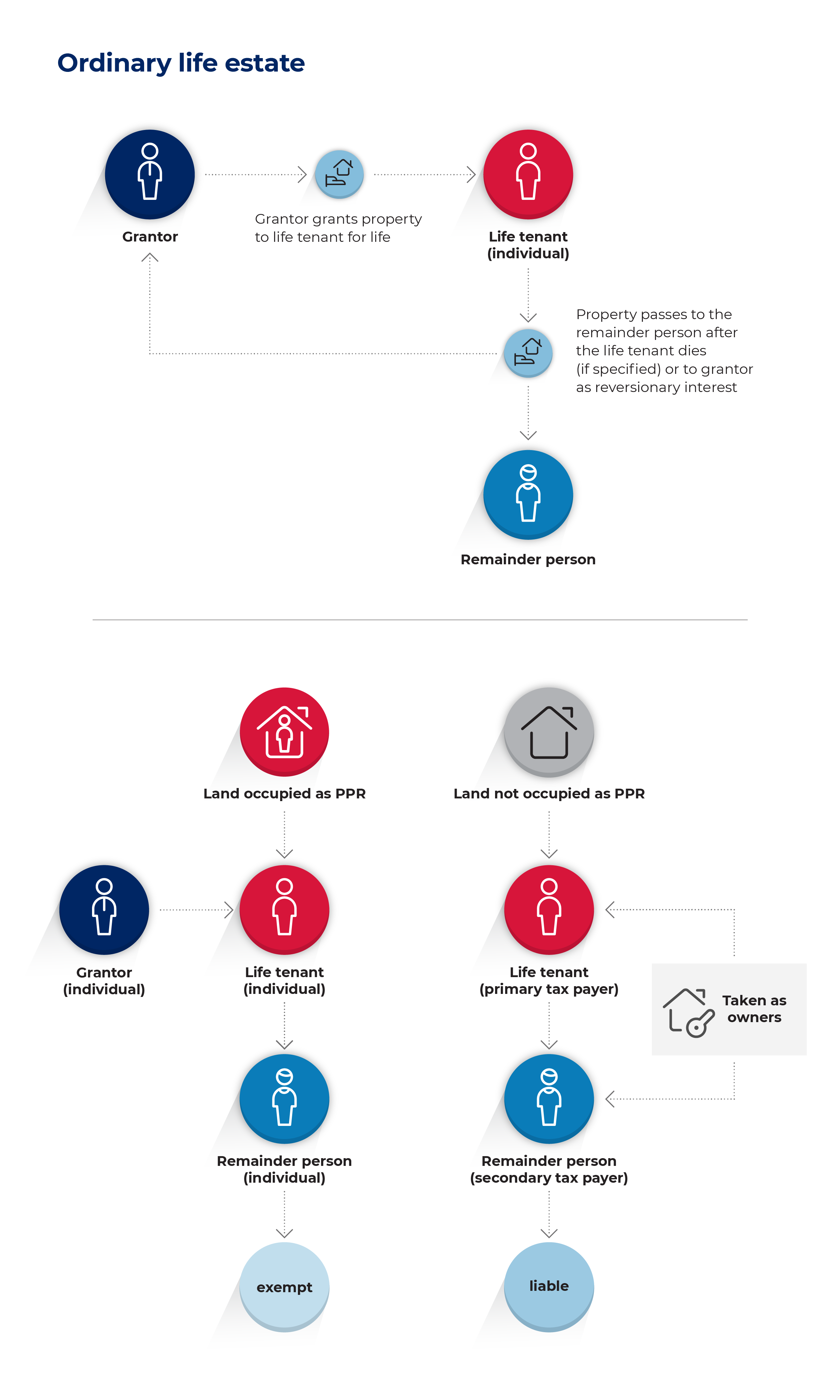

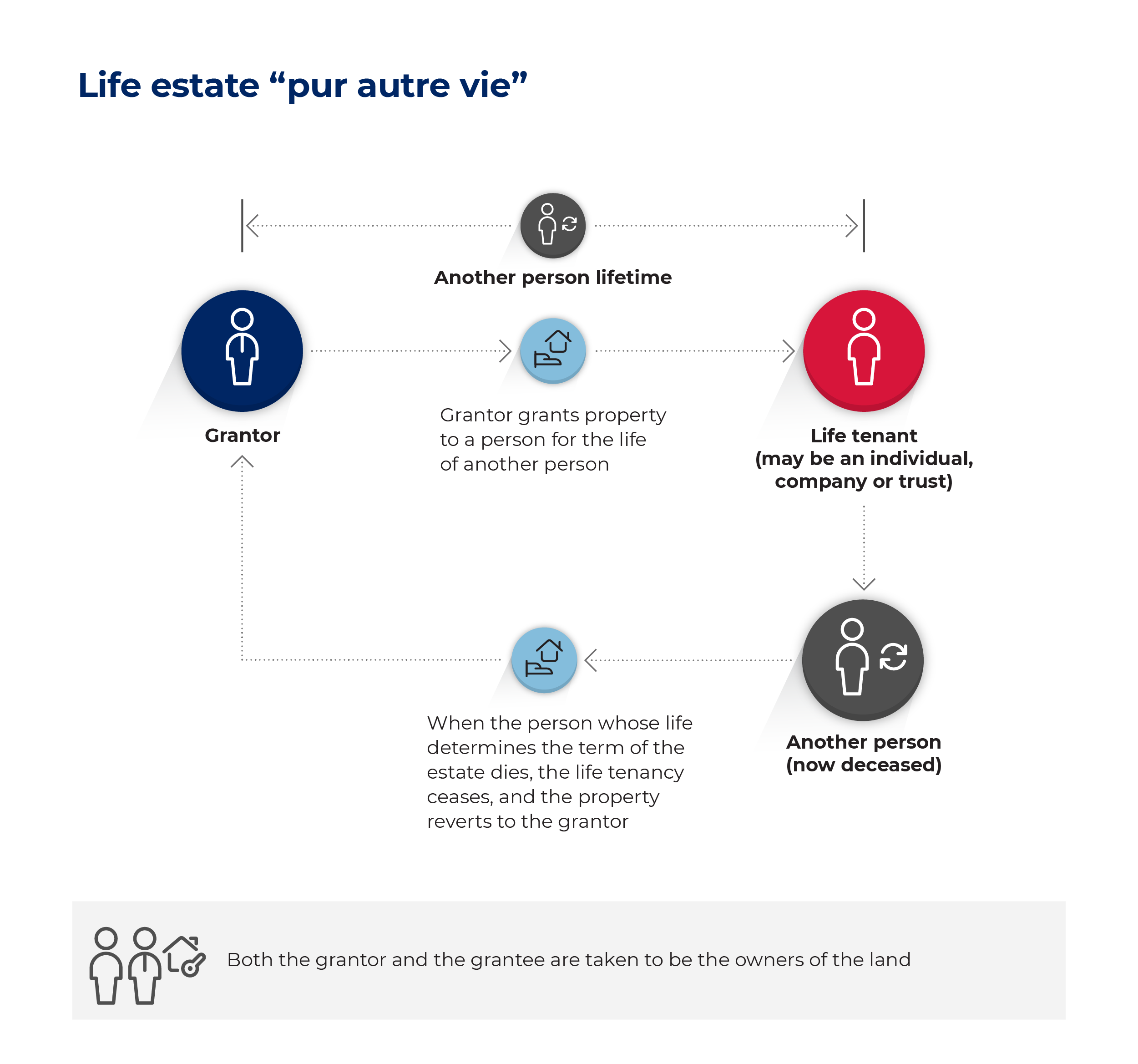

- A life estate is an interest in land granted by the owner of a freehold interest in possession, to another person for the life of that person or another person. A life estate entitles the holder to the use of the property and the right to any income from the use of the property (such as rent), for the remainder of the life of the holder or of another person. A life estate in land is a limited interest that is less than an estate of freehold in possession, however the owner of a life estate is taken to be an owner of the land for land tax purposes under s.20 of the LTMA. On the death of the holder or other person, the ownership of the land reverts to the owner of the freehold in possession or passes to another person (the “remainder-person”).

- The two most common forms of life estate are:

- an “ordinary” life estate, which is granted to a natural person for the duration of the life of that person;

- a life estate “pur autre vie” (for another’s life) which is an estate granted for the life of a natural person to another person; the person who receives the grant does not have to be a natural person, and may be a company or a trustee of either a fixed trust or a special trust.

The holder of a life estate is called the “life tenant”.

A life estate, whether created by a will or otherwise may be created as an equitable life estate, with the legal owner recorded on title as the legal owner.

What is an interest in reversion?

- If a person who owns the freehold estate in land grants a life estate to another person and is entitled to the land when the life estate expires, the owner retains an estate in reversion. The owner of an estate in reversion is taken to be an owner of the land for land tax purposes, for as long as the land is subject to a life estate and is taken to be a secondary taxpayer.

Note: The person entitled in reversion may be entitled to sell or otherwise dispose of the interest in reversion before the death of the life tenant, in which case the purchaser would be entitled to the land in reversion.

What is an interest in remainder?

- If a life estate in land is granted by a person who is the owner of the freehold estate, and another person is entitled to the land when the life estate expires, that other person has an interest in the remainder. A person who has an interest in remainder is taken to be an owner of the land until the holder of the life estate dies and is taken to be a secondary taxpayer; s.20(2) of the LTMA.

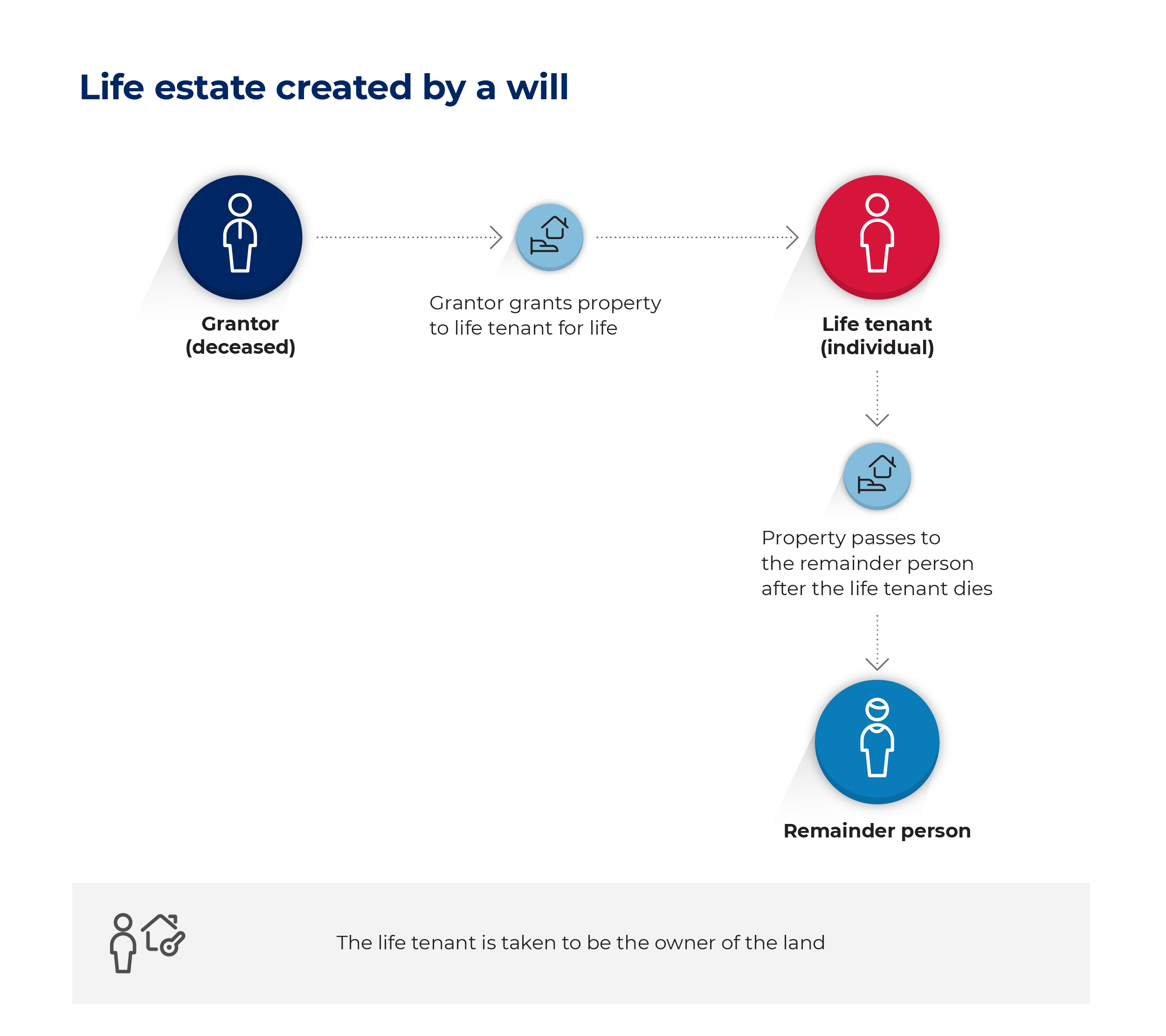

Life estate created under the express terms of a will

- If a life estate over a parcel of land is granted to a natural person under the express terms of a will, and the duration of the life estate is based on the life of the life tenant, the life tenant is treated as the sole owner of the land for land tax purposes; s.20(3) of the LTMA.

Note: If a life estate is created under a power granted under a will, the life estate has not been created by the express terms of the will (see Example 12 below).

- If a life estate is granted over a property to more than one person, whether jointly or separately, the joint tenants are treated as joint owners for land tax purposes.

- The persons entitled in reversion or remainder when the life tenant dies are not regarded as owners for land tax purposes while the life tenant is living, and therefore have no land tax liability.

- In some cases, a will may provide that any tax or expenses payable in relation to a life interest are to be paid by someone other than the life tenant. Such a provision does not affect the land tax liability of the life tenant or any other person, including the person responsible for payment of such expenses.

- If the land is the life tenant’s principal place of residence (“PPR”), the land is exempt. If there are joint life tenants, the land is exempt if any one of them uses and occupies the property as that person’s PPR. Following are examples of cases where land subject to a life estate created by a will is or is not exempt.

Examples of life estate scenarios created by a will

Example 1 – life tenant is entitled to PPR exemption

Under his will, Bob (deceased) grants a life estate in his residence to Mary (his spouse), and on her death, the land is to pass to their child, Jeremy. Mary continues to use and occupy the residence as her PPR until her death.

Mary is taken to be the owner of the property for land tax purposes and is entitled to the PPR exemption as long as she resides in the residence.

Jeremy is not taken to be an owner of the land and is not liable for land tax prior to Mary’s death.

Note: the position is the same even if the property was not Bob’s residence at the time of his death, e.g. the property may have been vacant or rented to tenants.

Example 2 – life tenant is entitled to PPR exemption

Under her will, Mary (deceased) grants a life estate in her residence to Bob (her spouse), and her adult daughter, Jill. On the death of Bob and Jill, the land is to pass to the family trust, which is a special trust for land tax purposes. Bob continues to use and occupy the residence as his PPR until his death. Jill lives elsewhere.

Bob and Jill are taken to be the joint owners of the property for land tax purposes, and the property is entitled to the PPR exemption until Bob’s death because the exemption applies if any owner uses and occupies the land as that owner’s PPR (see LTMA s.11(2) and Cl.2(3) of Schedule 1A). If Jill does not use and occupy the property as her PPR after Bob’s death, the property will cease to be exempt whether or not it is rented.

The family trust is not taken to be an owner of the land prior to the deaths of Bob and Jill, so the PPR exemption may apply for the duration of Bob’s life despite the fact that a special trust is entitled to the remainder interest. After Bob’s death, Jill will be entitled to the threshold if she does not use and occupy the property as her PPR.

Example 3 – life tenant may require residence to be sold and proceeds used to purchase another residence

Under her will, Mary (deceased) grants a life estate in her residence to Bob (her spouse), and on his death, the land is to pass to a discretionary testamentary trust, which is a special trust for land tax purposes. The Will contains a clause that Bob can require the original residence to be sold, with the proceeds applied to the purchase of a new residence in which he will be entitled to a life estate. Bob uses and occupies the new residence as his PPR until his death.

Bob is taken to be the owner of the original residence until it is sold as well as the new residence for land tax purposes and is entitled to the PPR exemption for whichever residence he occupies as his PPR.

The trustee of the discretionary testamentary trust is not taken to be an owner of the land prior to Bob’s death, so the PPR exemption may apply despite the fact that a special trust is entitled to the remainder interest.

Example 4 – Life tenant ceases to use and occupy the residence – PPR exemption does not apply

Under his will, Bob (deceased) grants a life estate in his residence to Mary (his spouse), and on her death, the land is to pass to their child, Jeremy.Mary moves into a retirement village after Bob dies and rents the property to a tenant until her death.

Mary is taken to be the owner of the property for land tax purposes and the property is liable for land tax.

Jeremy is not taken to be an owner of the land and is not liable for land tax prior to Mary’s death.

Example 5 – Life estate granted to a company as trustee - PPR exemption does not apply

Under his will, Paul (deceased) grants a life estate in his residence to ABC Pty Ltd as trustee of a fixed trust established for the benefit of Joan (his sister), who is the sole beneficiary of the fixed trust. On Joan’s death the land is to pass to the family trust, which is a special trust for land tax purposes. Joan occupies the residence as her PPR until her death.

ABC Pty Ltd is taken to be the owner and primary taxpayer for land tax purposes until Joan’s death. During her life Joan is a beneficial owner of the residence as a secondary taxpayer because she is a beneficiary of the fixed trust. If she owns other taxable land, she is assessed for land tax but she is entitled to a deduction to avoid double taxation under s.33 of the LTMA.

The land is not entitled to the PPR exemption because a company and trustee of a special trust is taken to be the owner of the land.

During the life of Joan, the Trustee of the family trust, as owner of the remainder interest, is also liable for land tax as a secondary taxpayer. The Trustee is assessed as a special trust and is not entitled to the threshold, but is entitled to a deduction under s.33 of the LTMA to avoid double taxation.

Life estates created other than by a will

- If a life estate is created other than by a will, the life tenant and the persons entitled to the land in reversion or remainder are all taken to be owners of the land for land tax purposes.

- The life tenant is taken to be the primary taxpayer and the person or persons entitled in reversion or remainder are taken to be the secondary taxpayer. The secondary taxpayer is entitled to a deduction in land tax under s.33 of the LTMA to avoid double taxation (see Revenue Ruling LT 039 - Deductions to prevent double taxation)

- This would be the case if an executor or administrator of a will grants a life estate under a power granted under the will, because the life estate is not created by the will itself.

- If a natural person who is either the owner of the life estate or entitled in reversion or remainder uses and occupies the land as that person’s PPR, the PPR exemption applies unless any of the owners is a company or a trustee of a special trust, other than:

- as trustee of a concessional trust (see s.3B of the LTMA); or

- as a trustee company within the meaning of the Trustee Companies Act 1964; or

- the NSW Trustee and Guardian.

Examples of life estate scenarios created other than by a will

Example 6 – Life estate granted by owner – PPR exemption applies

Bob owns a residence which is used and occupied by his son, Peter. Bob grants a life interest in the land to Peter, by a deed which is executed on 15 December 2019. The deed provides that Peter’s children (Jack & Jill) are entitled to the land when Peter dies.

Peter and his children are taken to be the owners of the land for land tax purposes from 15 December 2019. For the 2020 land tax year and later years during Peter’s life, Peter is the primary taxpayer and his children (as joint owners) are secondary taxpayers.

As Peter uses and occupies the land as his PPR, the land is exempt from land tax. Neither Peter nor his children are liable for land tax while the property is used as the PPR of Peter.

Note: If Peter moves out and either Jack or Jill use and occupy the land as his or her PPR, the PPR exemption will apply.

Example 7 – life estate in rental property granted by owner – PPR exemption does not apply

Bob owns a rental property and grants a life estate in the land to his son, Peter, who is therefore entitled to the rent. The deed also provides that Peter’s children are entitled to the land when Peter dies.

Peter and his children are taken to be owners of the land for land tax purposes. Peter is the primary taxpayer, and his children (in respect of the remainder interest) are secondary taxpayers as joint owners. Each of them may also be separately liable for land tax, depending on whether they each have any other taxable interests in land. Each child may be entitled to a deduction under s.33 of the LTMA to avoid double taxation.

Example 8 – life estate in land owned by a special trust

A Pty Ltd as trustee of the Big Family Trust owns a parcel of land and is subject to land tax as a special trust. A Pty Ltd grants a life interest in the land to B Pty Ltd for the life of Mr Big. On the death of Mr Big, the land reverts to A Pty Ltd as trustee of the Big Family Trust.

A Pty Ltd and B Pty Ltd are both taken to be owners for land tax purposes. B Pty Ltd as holder of the life interest is the primary taxpayer and is entitled to the threshold. A Pty Ltd is the secondary taxpayer and is not entitled to the threshold because it is a special trust, but is entitled to a deduction for the land tax payable by B Pty Ltd in respect of the land under s.33 of the LTMA to avoid double taxation.

Example 9 – life estate granted by a company to a Director

A Pty Ltd is the owner of a parcel of residential land. A Pty Ltd grants a life estate to a Director of the company, John Smith, for his life, and he occupies the land as his PPR. A Pty Ltd is entitled to the land on the death of John Smith.

John Smith and A Pty Ltd are both taken to be owners of the land. John Smith is the primary taxpayer and is liable for land tax because a company also has an interest in the land as an owner.

Example 10 – Life estate granted by a company to natural persons as joint owners

A Pty Ltd is the owner of a parcel of residential land. A Pty Ltd grants a life estate to John and Mary Smith, based on the life of Mary Smith. They use the property as their PPR. A Pty Ltd is entitled to the estate in reversion and is an owner of the land because the life estate was not created by a will.

John and Mary Smith are assessed jointly as the primary taxpayer. Because a company (A Pty Ltd) has an interest in the land, the PPR exemption does not apply. A Pty Ltd is assessed as a secondary taxpayer and is entitled to a deduction for the land tax payable by John and Mary in respect of the land to avoid double taxation.

Example 11 – Life estate granted by a company atf a fixed trust to another company

A Pty Ltd atf of a fixed trust owns a parcel of land. Adam and Andrew are beneficiaries of the fixed trust and each is entitled to 50% of the income and capital of the trust.

A Pty Ltd grants a life estate in the land to B Pty Ltd, based on the life of Adam, the sole director of A Pty Ltd and A Pty Ltd has the estate in remainder on the death of Adam.

B Pty Ltd is the primary taxpayer and is entitled to the threshold. A Pty Ltd is the secondary taxpayer and is entitled to a deduction for the land tax payable by B Pty Ltd in respect to the land under s.33 of the LTMA to avoid double taxation. The deduction would be equivalent to the land tax payable by B Pty Ltd in respect of the land but A Pty Ltd may be liable to land tax if A Pty Ltd has an interest in other NSW taxable land.

Adam and Andrew each hold a 50 per cent equitable interest in the parcel of land as joint owners and as such are a secondary taxpayer. They are entitled to a deduction for the land tax payable by B Pty Ltd in respect of the land under s.33 of the LTMA to avoid double taxation, but may be liable to land tax if have other interests, either jointly or separately, in other taxable land in NSW.

Example 12 – Life estate granted by an executor of a will – PPR exemption does not apply (see paragraph 9 above)

Under her will, Mary (deceased) leaves her estate to her husband Bob, subject to a discretion granted to Bob as the executor of her estate, to determine the disposition of specified assets. Under the discretionary power, Bob determines that a residential property owned by Mary and occupied by their Daughter, Jill, should be transferred to the family trust. The trust is a special trust for land tax purposes. Bob also grants a life estate in the property to his daughter Jill, based on Jill’s life.

As the life estate was not created by the express terms of Mary’s will, the PPR exemption does not apply because a special trust has an interest in the property, as owner of the interest in reversion.

Jill is the primary taxpayer and is entitled to the threshold. The family trust is liable at the special trust tax rate and may be entitled to a deduction to avoid double taxation under s.33 of the LTMA.

Note: If Bob allocated the property to himself or another natural person instead of the family trust, Jill would have been entitled to the PPR exemption as long as she continued her use and occupation of the property.

Life interest under a lease

- Interests in land in NSW may be freehold or leasehold. However, the only recognised freehold estates in NSW are an estate in fee simple and a life estate. S.20(4) of the LTMA makes it clear that a lease for life or an agreement for lease is not a life estate for the purposes of s.20 of the LTMA.

Right of occupancy after death of owner – Cl.10 of Schedule 1A of the LTMA

- Clause 10 of Schedule 1A of the LTMA provides for the PPR exemption to continue following the death of the owner where another person is granted a right of occupancy under the will, and that person occupies the land as his or her principal place of residence. The right of occupancy is not a life estate because it ceases when the occupancy ends.

- This concession is explained in Revenue Ruling LT 082 v5 (The principal place of residence exemption).

Registration of a life estate

- A person who acquires an interest in land as a life tenant or acquires an interest in the remainder or reversion should lodge an initial land tax return or a variation return depending on whether or not the person is already registered for land tax purposes. The due date for initial returns is usually 31 March during the tax year. Variation returns are usually required to be lodged by the first instalment date shown on the notice of assessment. If the notice of assessment shows that no tax is payable, the due date for lodgement of a variation return is usually 40 days after the “Issue Date” shown on the notice.

Evidence of ownership of a life estate must be produced

- An owner must present documented evidence of the existence of a life estate. Such evidence may include a valid deed or the will of a deceased owner. An executed transfer may be presented instead of a deed or will.

- Neither a deed nor a transfer in relation to the granting of a life estate has to be stamped because the creation of a life estate is not liable for duty. However, the transfer of a life estate from the current holder to someone else does require stamping.

- If a deed or transfer is not dated, a declaration from both the transferee and the transferor specifying the date on which the life estate was transferred must be provided.

- In the absence of satisfactory documentary evidence as to the date of creation, a life estate will only be recognised by the Chief Commissioner from the date on which a copy of the relevant deed or transfer is received by the Chief Commissioner.

Assessment and Reassessment

- Part 3 of the TAA specifies when an assessment or reassessment may be made by the Chief Commissioner.

- Where more than five years have elapsed since an initial assessment was made, s.9(3) of the TAA provides that a reassessment can only be made:

- as an outcome of an objection or appeal decision; or

- where a full and true disclosure of the facts and circumstances was not made at the time of the initial assessment and as a result the tax liability assessed was lower than the Chief Commissioner would have assessed; or

- where the reassessment is authorised to be made more than five years after the initial assessment by another taxation law; or

- where the reassessment is made because of an application by a taxpayer (made within five years after the initial assessment) and reassessment would result in a reduction of the tax liability.